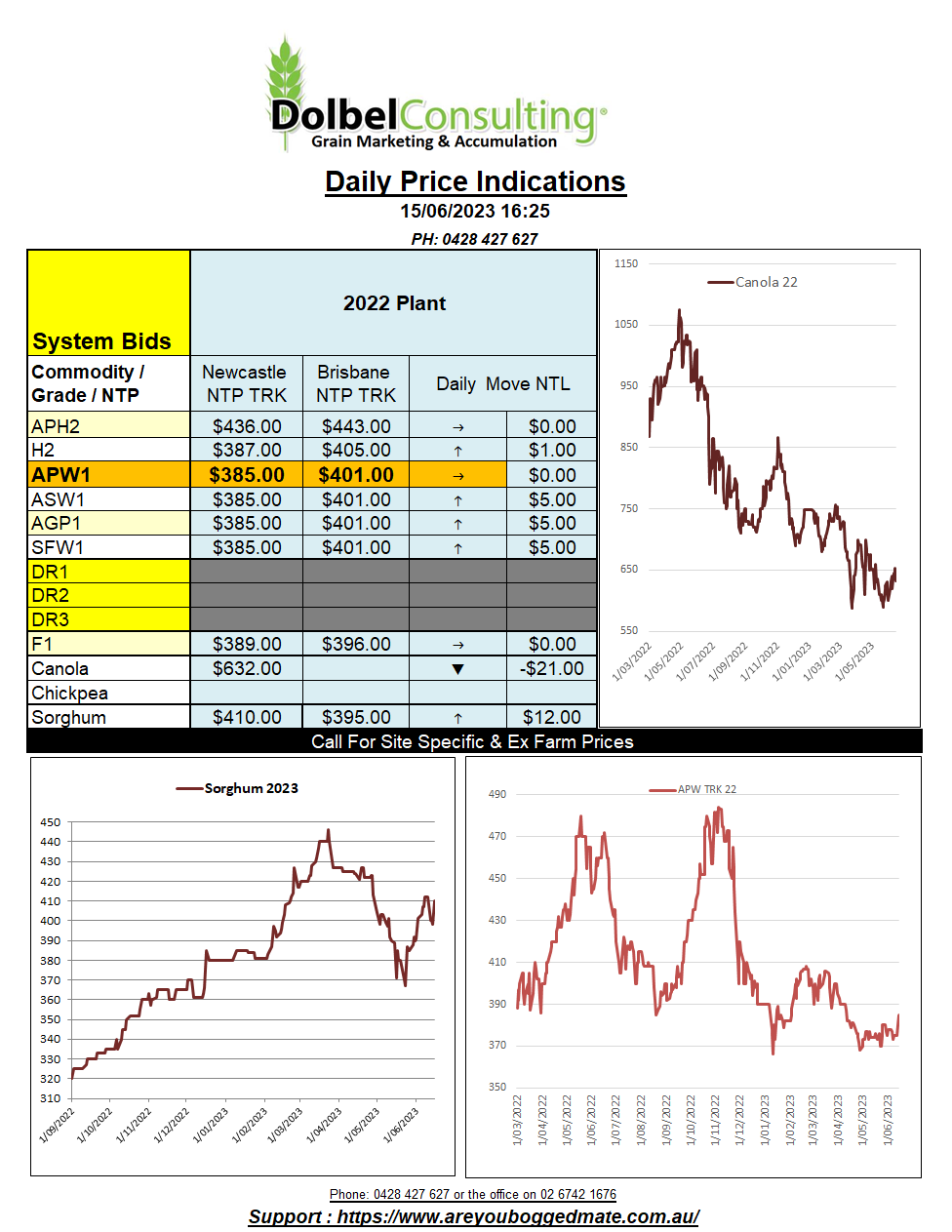

15/6/23 Prices

There’s not a lot of green on the futures board this morning. US wheat and corn were lower, soybeans were mixed.

Both Paris rapeseed and Winnipeg canola were lower, Paris sharply so. The move in Paris when taking the move in the AUD / Euro into account is worth about AUD$18.16 downside in old crop values, and about AUD$16.58 off the top of new crop values. Winnipeg was not as low, shedding around C$3.30 in the new crop. Drier weather in Canada helping to support the market there.

Drier weather across the Canadian Prairies also helped support spring wheat futures at MGEX and cash FOB wheat offers out of the PNW. Although PNW values did slip a little day to day, the move lower was not as sharp as the decline in either SRWW or HRWW cash or futures.

The seven-day forecast for the US and Canada shows that the dry regions across the central US corn belt are likely to stay dry but the central Saskatchewan Prairies may see a shower or two. Canola regions in Alberta are also likely to see some good falls in the week ahead.

Conditions are looking to dry down a bit in the wheat regions of China after heavy rain was said to have damaged much of the winter wheat in late May. No doubt we’ll see another “record” crop out of China, as they slowly increase imports.

Taiwan picked up 56kt of US milling wheat for a first half August delivery. DNS with a minimum 14.5% protein wheat as booked. The price was said to have been around US$368 C&F Taiwan. On the back of an envelope that converts to an XF LPP price equivalent to something close to AUD$450, not that there is any old crop APH left to price. There was some HRWW done at about a US$25 discount to the DNS, this converts to a better number than we’ve been seeing for port based H2 here, AUD$425, and converts to roughly AUD$410 ex farm LPP, without trade margin and insurance deductions.