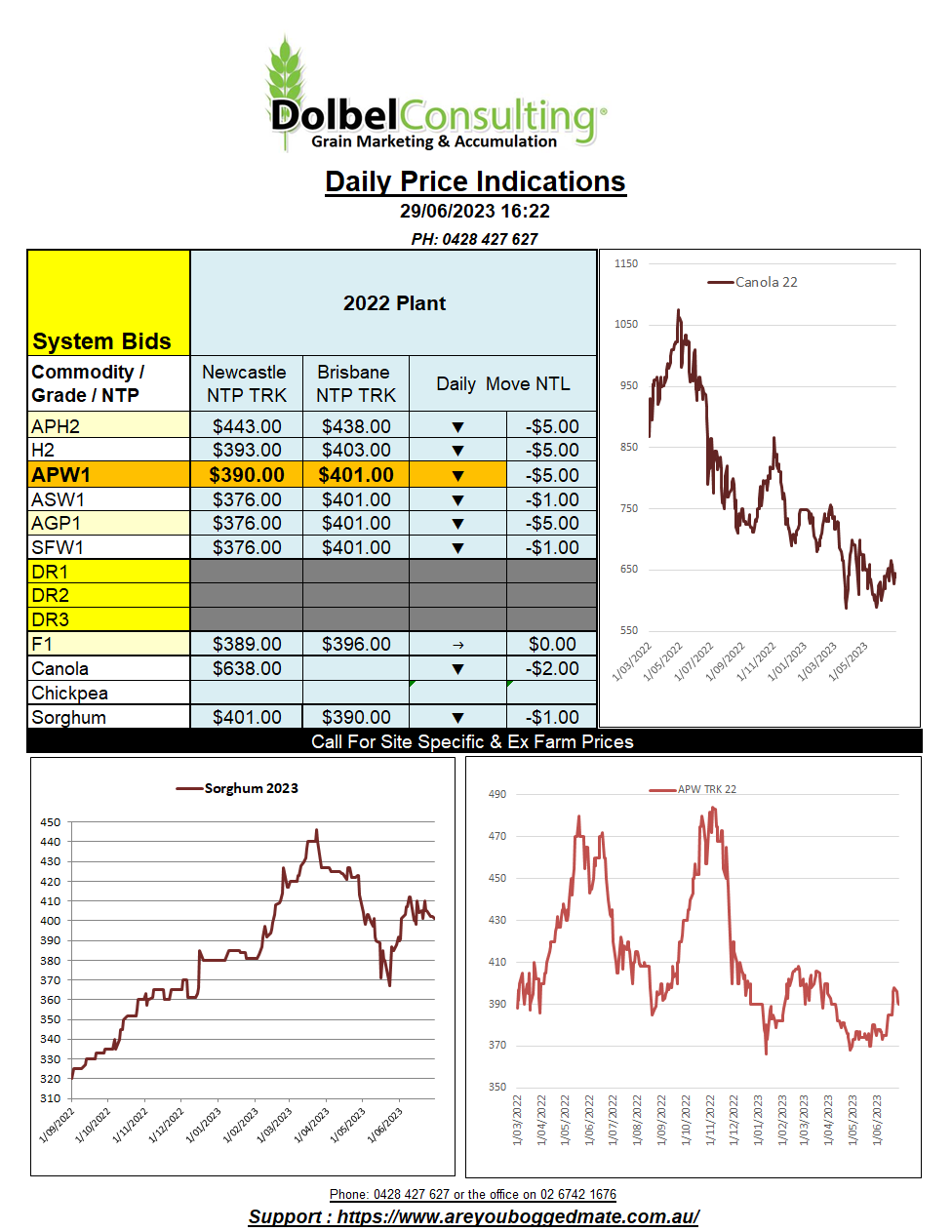

29/6/23 Prices

Another ugly night in the world futures markets. Corn futures at Chicago were hit hard for a second session, soybeans followed, back 30c/bu (AUD$16.70) in the new crop and 44c/bu (AUD$24.50) nearby. Wheat was again caught up in the action, dragged lower. Even the HRWW contracts was lower, shedding AUD$17.95 per tonne in the Dec23 slot.

The weaker AUD may counter a little of the move, roughly AUD$4.80 of the move in nearby soft red winter wheat futures at Chicago, but the move there is roughly AUD$16.29, so given a flat basis there is some downside potential here again today.

Local wheat basis did recover significantly yesterday, going from 5c/bu under to about 25c/bu over FOB. A 30c/bu recovery in basis limited day to day losses for old crop APW to just AUD$5.00, it could have been much worse, and may well be today.

US wheat was again dragged lower by the better weather in the US corn and soybean areas that have been very dry from the time of sowing. US wheat had also been uncompetitive in the world market after being dragged higher by the weather rally in row crops. These adjustments are helping US wheat futures back to a level where it can again compete into the Asian markets, as seen on today’s global wheat price comparison chart. US white wheat out of the Pacific Northwest is now priced at or lower than the Aussie product into the north Asian market.

The Canadian prairies continue to see much less rain in the forecast than their southern neighbours. The GFS model for the next week shows little to no rain across the major durum regions of Saskatchewan. Some average falls are expected towards central and northern Alberta which could be viewed as beneficial to Canadian canola. In general, the outlook isn’t great for durum and spring wheat in Saskatchewan though, so keep an eye on this. Dry weather is also returning to the Russian / Kazakhstan spring wheat region, this area has been dry throughout most of the growing season now.