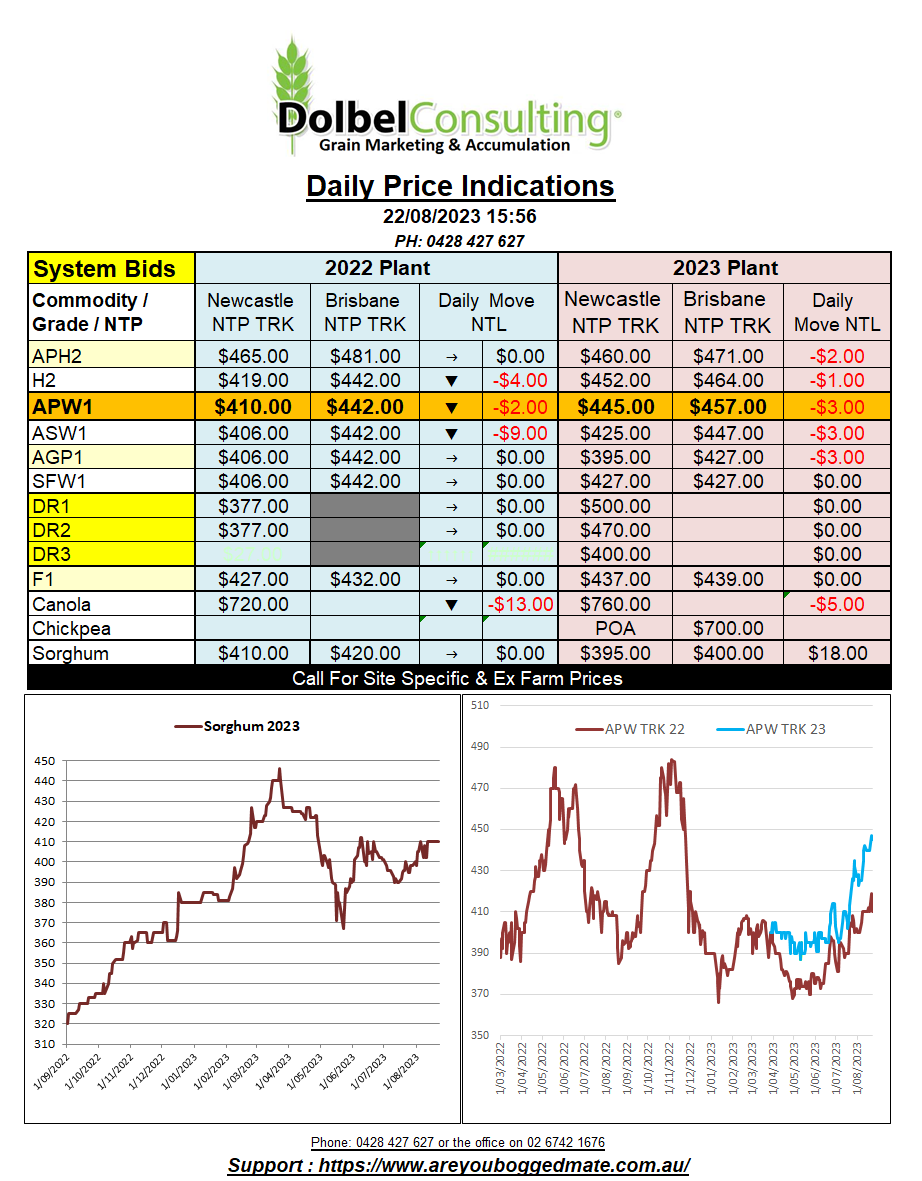

22/8/23 Prices

The Turkish pasta millers are now putting pressure on the government there to limit the durum wheat exports. There’s been talk that Turkey had sold as much as 1mt of grain durum to Italy. Export paper work currently backs up at least 300kt has been booked.

Turkey has had a good season, durum production is better than average, but to export 1mt of grain durum was always going to be a big call and could have potentially left the industry needing to import durum from Russia or Kazakhstan later in the season. Most likely at a time when international prices were reflecting the tightness of supply given the drought in Canada and now the potential downgrading of the US crop.

Overnight Canadian 1CWAD13 prices were flat. The average price ex farm SE Saskatchewan for a Dec23 lift was C$506.23 (AUD$582.81). Durum values on the Canadian Prairies did not follow the milling wheat market lower.

Still in Canada we also see the canola price higher, ex farm SE Sask climbed C$8.85 for a Dec23 lift, to C$768.42 per tonne. The move in Canadian values was against the trend in Paris rapeseed futures, which closed down E5.25 in the Feb24 slot. Local prices here may be torn between the two, the move in Paris rapeseed basically equating to potential downside of AUD$8.36 for the new crop.

Issues in China continue to weigh on the AUD. The official five year prime rate was cut by 10 points, not the 25pts the market had expected to see, so that could be conceived as better than expected if you want to grasp to something almost bullish. This doesn’t really give you the confidence it should though considering the collapse of Evergrande Group over the last couple of years, finally putting up the white flag a week or two back. What does real-estate in China have to do with my grain price I hear you ask. Well not a lot, but it does have a bit to do with the AUD, so keep half on eye on this “crisis”.