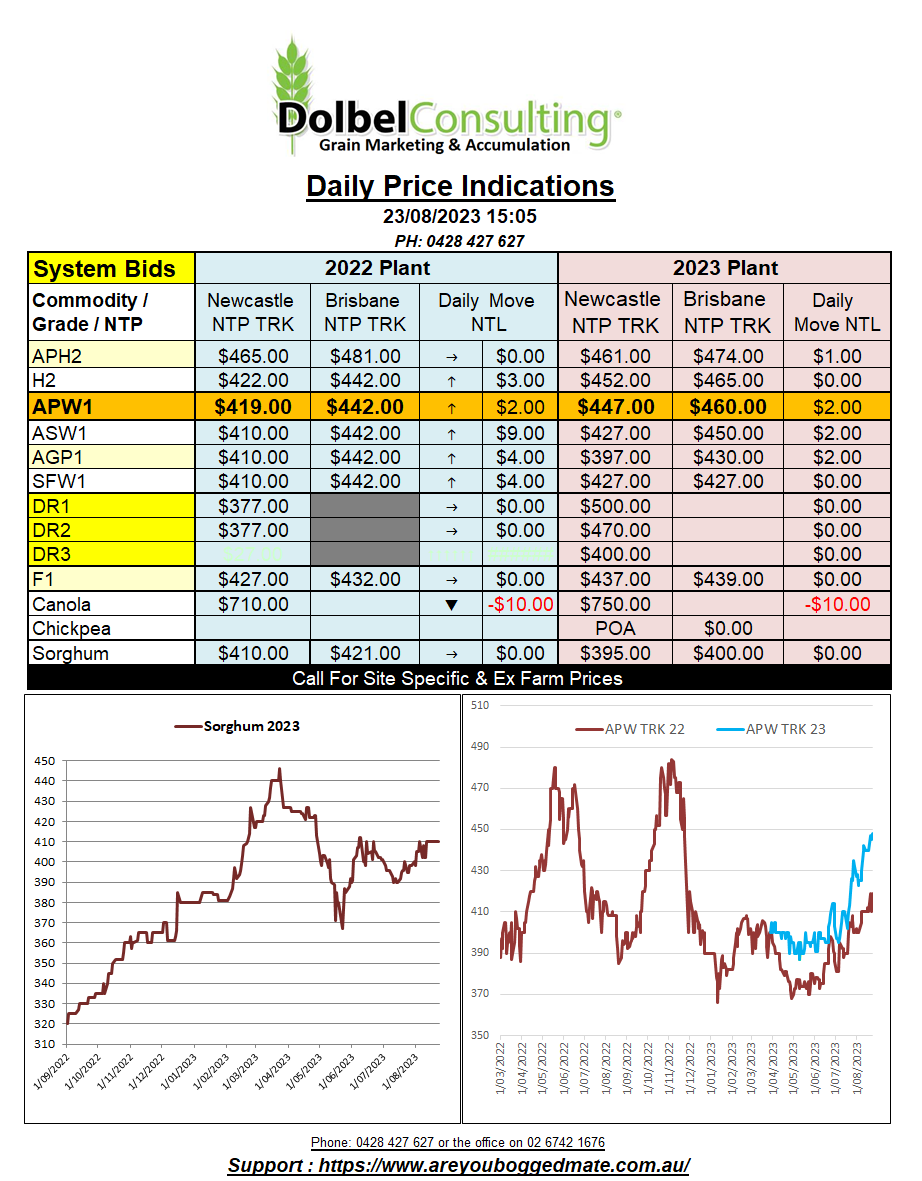

23/8/23 Prices

The level playing field of international grain marketing. Remember that, it was the reason we disbanded the single desk marketing system. You remember that system, that thing we had to help sell wheat. Apparently it gave Australian growers an unfair advantage because it shared arbitrage, blending, freight and storage costs across the entire Aussie crop. Reducing risk and enhancing marketing efficiencies that prevented undercutting on the offer side and helped to gain market share by educating international processors on the best ways to mill Aussie wheat, remember that. It was viewed as a subsidy, we were told “subsidies bad”.

So I enjoyed reading that the Ukraine Minister for Agrarian Policy has asked the European Commission to compensate Ukrainian farmers (cough, cough, yeah farmers), to the tune of thirty Euros per tonne to help them export wheat and grain through alternative European ports because they cant export enough out of the Black Sea river ports. The EU response, thankfully, appears to be that they don’t have any money put aside to do this.

With the amount of money the US has thrown at Ukraine over the last 12 – 18 months I’m surprised they can’t afford to fly grain out.

US markets were mixed, with spring wheat harvest half way through there was a little more downward pressure on higher grade milling wheat prices. The move kind of flew against the fundamentals though. Especially considering the USDA reduced the G/E rating of the spring wheat crop 4 points in the weekly crop progress report. The Canadian 1CWRS13.5 wheat price also slipped, shedding C$2.84 for a December lift. Durum prices across SE Saskatchewan were generally flat. Not so for canola though. Winnipeg canola, Paris rapeseed and Chicago soybean all saw some downside. SE Sask cash bids shed C$12.47, Winnipeg C$12.60 and Paris E2.75 for the Feb24 slot. Every good rally has to find resistance sooner or later.