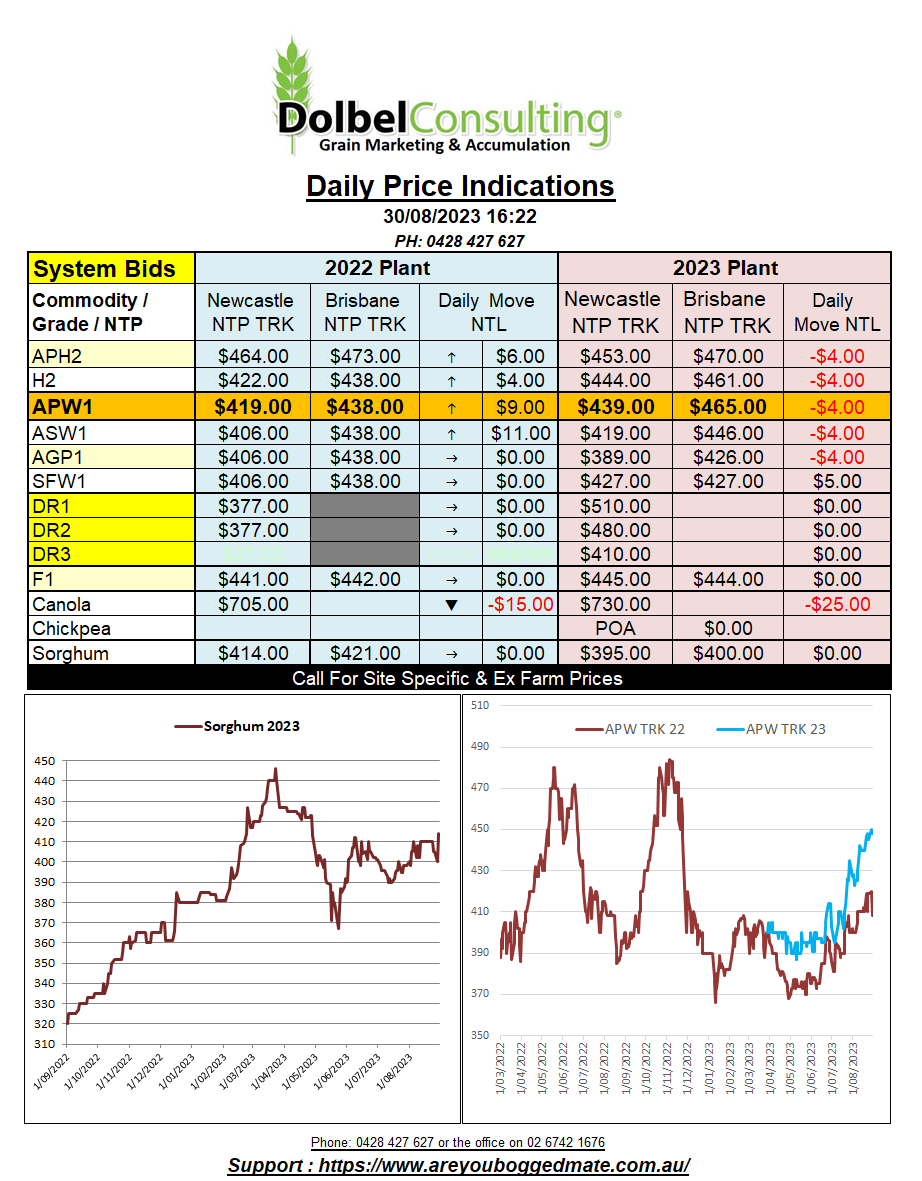

30/8/23 Prices

International canola values were mixed in overnight trade. There were some sharp losses on the Paris exchange. Rapeseed futures for the Feb24 slot slipped E7.75 / tonne. The combination of a stronger AUD and the fall in Paris rapeseed futures equates to a day to day conversion difference of roughly AUD$15.49 lower. At Winnipeg the canola futures contract closed a little higher but once the stronger AUD is taken into account there is again feasible downside here of around AUD$1.26. That’s not much, but with both of the major indicators lower the trade here in Australia use to help determine prices, it may weigh on local bids today.

Chicago soybean futures were also lower, shedding 11.5c/bu (AUD$6.50) in the Jan24 slot. The punters were placing bets that the latest hot dry weather would have seen the crop rating for US beans slide much further on Tuesday. The sell down today does tend to make beans look a little oversold now, but soybeans in particular have a lot of weight on them as the world chews through a huge S.American crop and the US crop about to hit the market.

US wheat futures tended to ignore the improved fundamentals of better US export sales and declining crop condition, to concentrate on harvest pressure and technical trade / profit taking. The main headwind for US export sales continues to be competition from other major exporters. This may become less of an issues going forward as crop size in Australia, Canada and Argentina are all expected to fall over the next few months. That will leave Black Sea and EU grain as the major competition and to be honest, the quality of the EU crop, particularly in the north, isn’t great, so EU wheat may not create a huge hurdle. That just leaves the Russian crop, which appears to be getting bigger and bigger if you believe the latest estimates. Interesting to note that Kazakhstan has extended their ban on wheat imports. This was initially implemented to prevent stolen Ukraine wheat from depressing local prices.