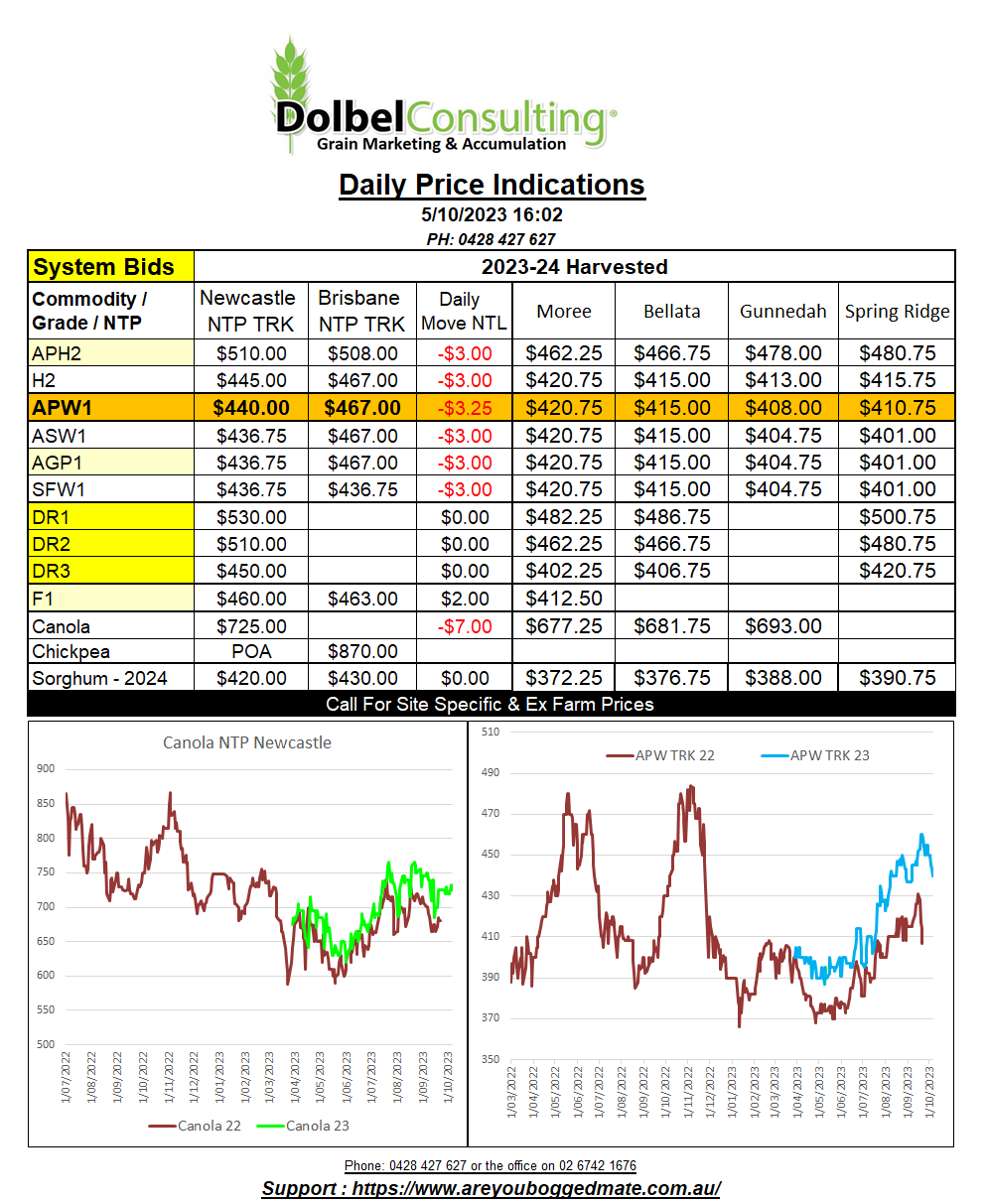

5/10/23 Prices

International wheat futures closed lower, Chicago SRWW and HRWW both falling. Minneapolis spring wheat joined the HRW contract and settled with double digit losses as the funds jumped back on the sell side, which they’ve actively participated in all year. London feed wheat futures slipped lower, shedding £1.15 in the Jan24 slot. Paris milling wheat was also weaker, shedding €2.50 in the December slot through to the May 24 slot.

Taking the move higher in the AUD into account doesn’t help when comparing cash values today to yesterdays cash values. Out of the US Pacific Northwest FOB values followed the futures markets lower. White wheat was back about AUD$2.00 but the big losers, as with futures, was HRWW and spring wheat, back between AUD$10 and AUD$12 per tonne FOB.

Canadian values out of the Pacific Northwest were also lower, not as much as the US product, but still falling by roughly AUD$9.00. Across SE Saskatchewan PDQ also indicate that cash prices for 1CWRS13.5 spring wheat fell on average C$5.54 to C$314.21 per tonne for a Dec 24 lift. Durum values out of SE Sask were flat to firmer. When taking the AUD move into consideration the Canadian values converts to a day to day decline of roughly AUD$4.00, while French durum values are relatively flat day to day in AUD terms.

Talks around the establishment of, or the re-introduction of, the Black Sea Grain Corridor deal appear to be stalled. Russia obviously don’t want it. Ukraine would like to have it, ship owners would love it and insurance underwriters might be able to sleep at night if there is one. Presently the flow of Ukraine grain isn’t being decimated by not having it, export volume is still good enough to meet expectations. Ukraine values are low and one could argue if a deal was struck prices could simply remain low, even if execution cost were reduced, thus forcing world, or at least Black Sea values, lower in the mid term.