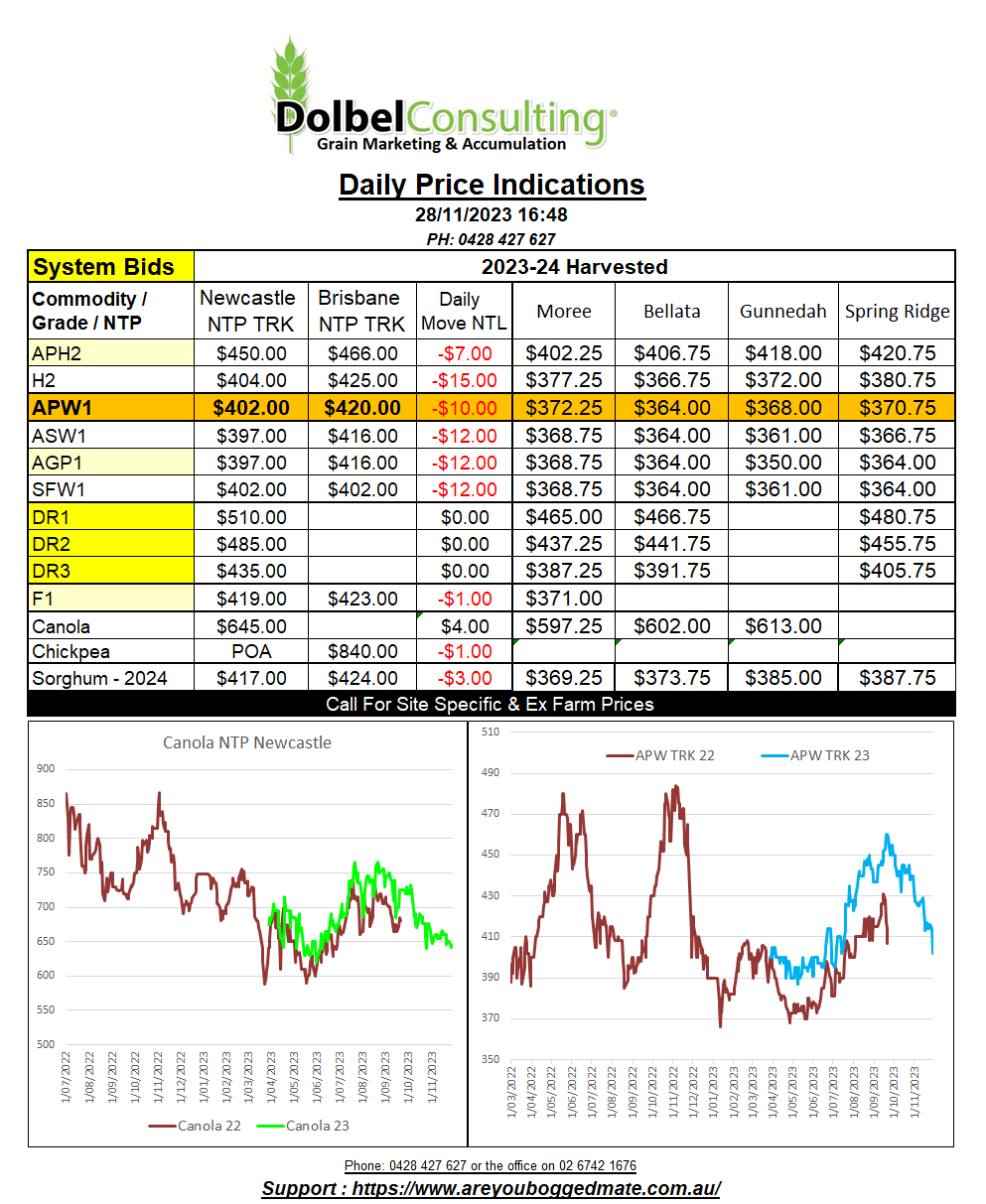

28/11/23 Prices

International markets remain hard to pick. China continues to have a major influence on everything from soybeans and corn to wheat and sorghum. There was talk that China was looking to roll the delivery of 2 – 2.5mt of French wheat purchases by 2 months. This had the punters talking about a possible slowing of demand from China. It had me thinking that it might just coincide with lower Aussie wheat prices. At today’s numbers French wheat is more expensive than Aussie wheat C&F China. If you were to throw some good FX trading into that scenario Aussie wheat could even be cheaper and Australian quality has been exceptional up until now. Even Newcastle port zone is almost competitive with French wheat C&F China.

The latest values C&F China show WA milling wheat estimated at US$276.05, US wheat at US$316, French around US$320.

Wheat futures at Chicago also saw technical liquidation prior to first notice day on the December contract. During the calendar year the December 23 soft red winter wheat futures contract at Chicago has shed 272c/bu, at today’s money that’s about AUD$151. Bidding for new crop APW started here in March at AUD$400 port, yesterday it closed at AUD$415 port for track deliveries. The punters have sold US wheat futures hard all year. Since March this year US white wheat out of the Pacific Northwest has shed about AUD$60.

Paris milling wheat futures closed lower, the March contract shedding E3.75 / tonne. The only grain with a few green closes was rapeseed and canola. Paris up a day to day equivalent of AUD$4.65 and Winnipeg canola futures closed +C$7.00 on the nearby slot, against the trend in Chicago beans.

Tender business is limited this week, Pakistan in for 100kt of milling wheat and Bangladesh in for 50kt of milling wheat.