30/11/23 Prices

Hard red wheat futures broke away last night, closing 27c/bu (AUD$15) higher in the nearby slot. Caught and short prior to first notice or some increase in demand ? I’d assume more of the former than the later.

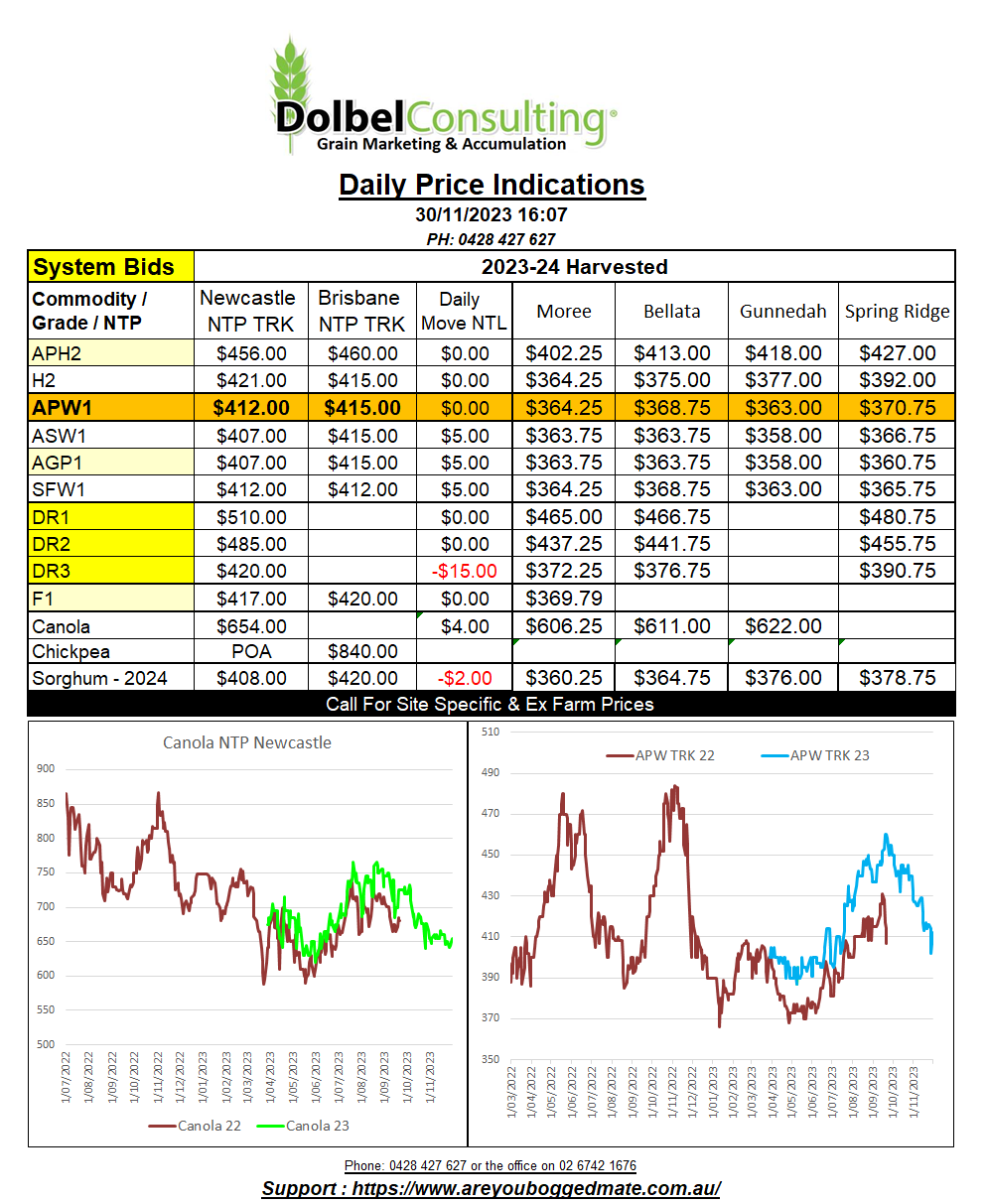

The heavy rain across eastern Australia found some attention in international wires. Some punters calling for 1mt of milling wheat now to be classified at feed wheat. By this time next week we may just see that figure quantified, and I’m assuming it will only go one direction, the demise of test weight will also be a big issue. The potential downgrading of a significant portion of the crop across Australia’s SE may create some stronger domestic demand for the better wheat in NNSW, as little as there is, chart attached (Riverina Aust data). We may also see prompt SFW1 homes fill quickly.

There was speculation that Morocco will increase soft wheat imports by as much as 2.5mt to cover reductions in local production due to drought. This maybe just the increase in demand the EU needs to see.

Russia has confirmed their intention to ban durum wheat exports for the first half of next year. As bad as this sounds it’s a bit like shutting the gate after the horse has bolted, jumped a fence, walked into the neighbors horse float and raced in the Melbourne cup.

Canadian durum values were flat yesterday after shedding a couple of bucks on Tuesday. Milling wheat out of the PNW followed HRW futures higher.

There was also some chatter that Russia may also limit wheat exports, this sentiment was somewhat contradicted by a reduction in their wheat export tax though.