4/12/23 Prices

Cash wheat offers FOB US Pacific Northwest were generally a touch firmer, following the Chicago futures market higher. Last weeks US wheat sales volume took the market by surprise, 622,800t, it was even larger than the largest trade estimate leading into the report. Support in wheat was both spillover business from the better than expected export news and technical trade from short covering.

Ukraine appears to be having little trouble getting grains to export. Monthly volume for November was 6.1mt. Of that total 1.2mt was wheat and 2.3mt was corn, the balance consisting of oilseeds and barley. Ukraine 11.5% milling wheat is valued at US$231.50 FOB Black Sea. The cost of execution remains high if not through their B/Sea ports, rates variable due to the threat of a Russian nature, but the price is competitive enough to keep exports ticking over.

A private analyst has predicted that the Brazilian soybeans crop will not exceed last years record of 154.1mt but could still give 150mt a nudge. A 150mt Brazilian soybeans crop, the second in a row, is likely to continue to weigh on global oilseed values for a long time to come. Although the current estimate is some 10mt or more less than the initial forecast a couple of months ago, a crop of 150mt is still an impressively large crop.

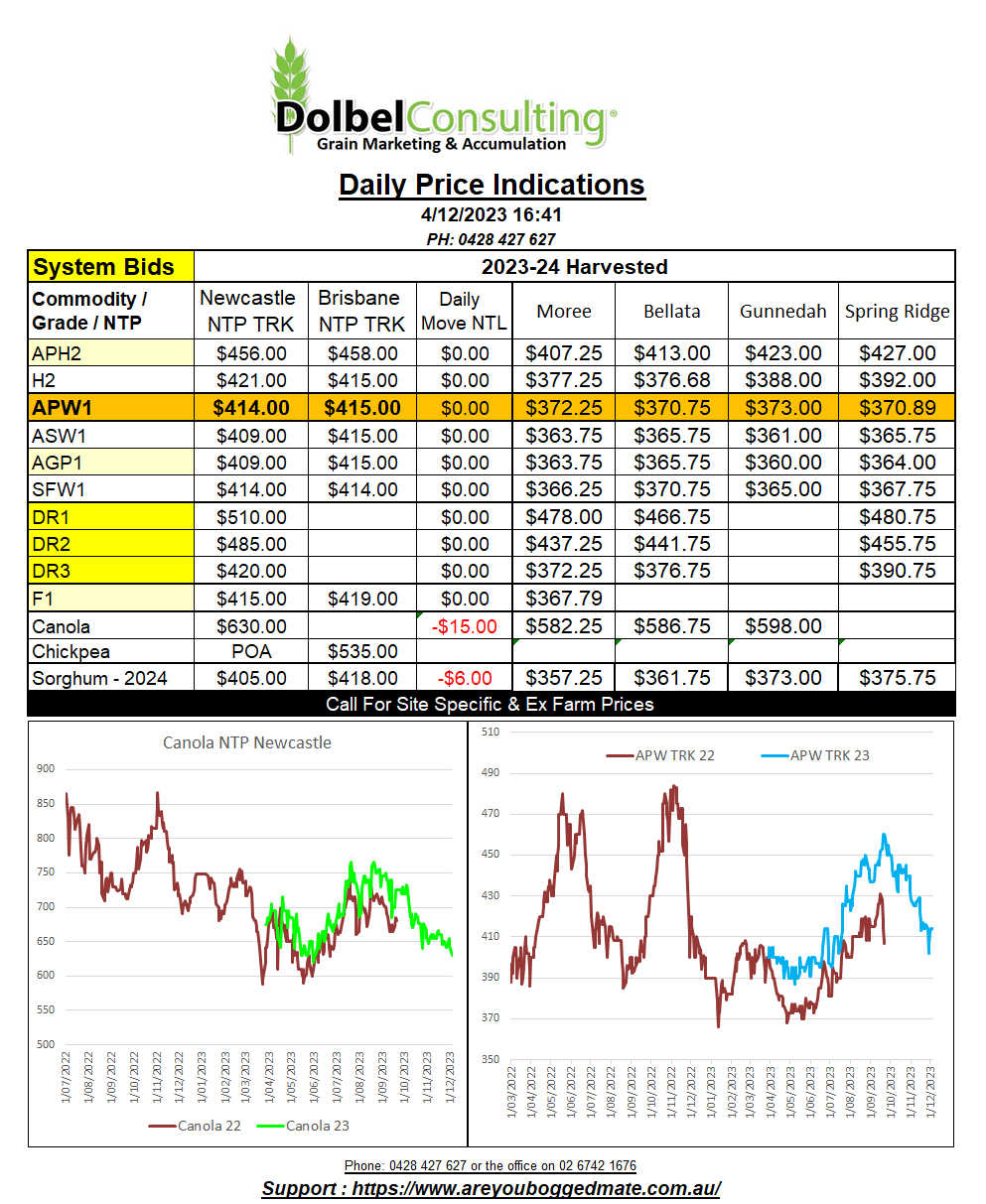

Overnight both Paris rapeseed futures and Winnipeg canola futures fell sharply. Led partly by another decline in Chicago soybeans but also, in the case of Winnipeg, slow export sales. In AUD terms, we see the conversion also hurt by an improvement in the AUD against both the Euro and the CAD. In the case of Paris the fall of E9.50 on the nearby converts to roughly AUD$22.78 potential downside here when taking FX variations into account. With Winnipeg slipping AUD$24.70 when considering CAD/AUD moves, both markets could weigh heavily on canola bids here come Monday.