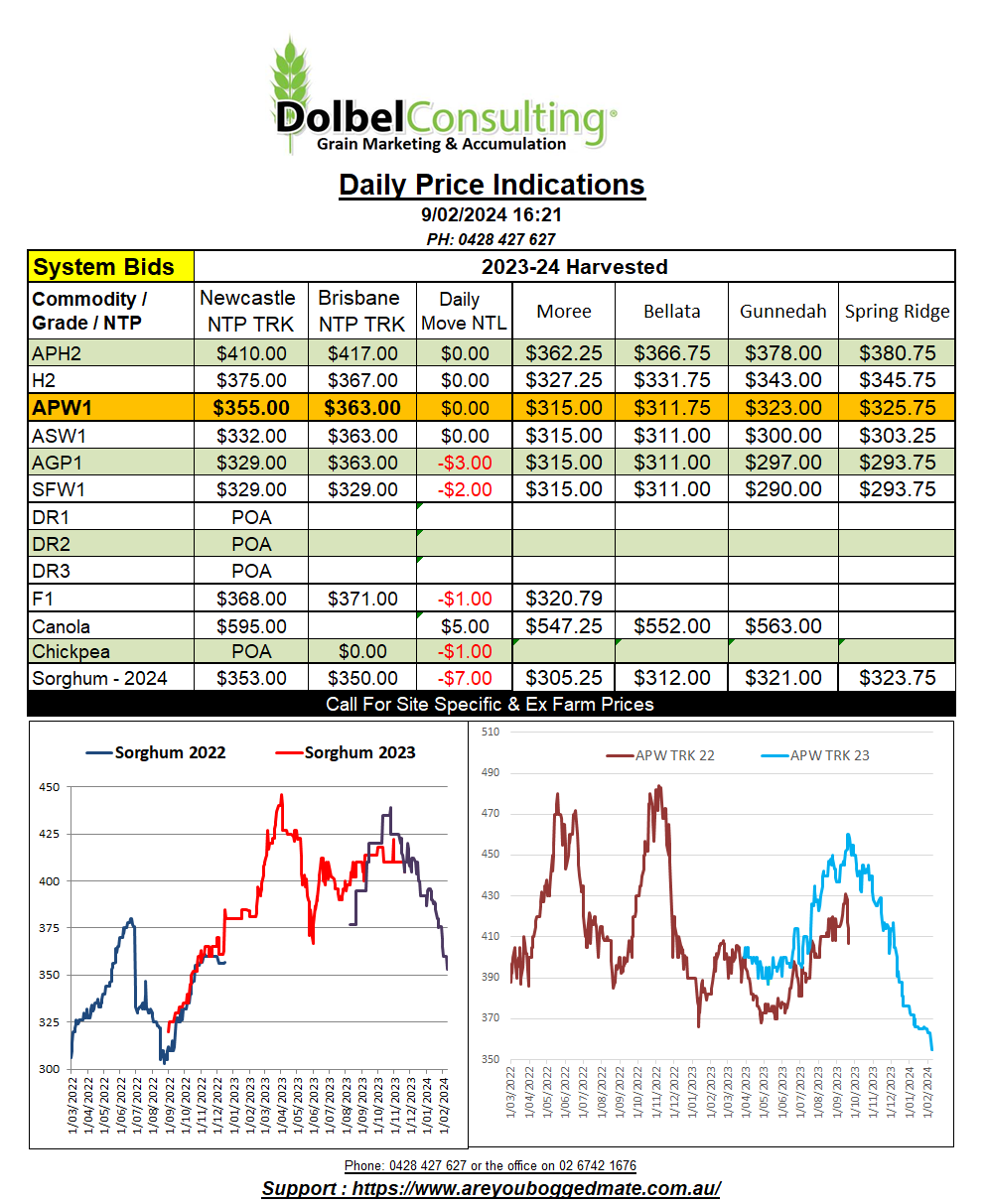

9/2/24 Prices

There’s a lot of adjustments to digest in the February USDA World Ag Supply and Demand Report. As usual I’ll concentrate on wheat. Initially the numbers start well, a slight reduction in world carry in after adjustments to last years data. World production was increased as most of the punters had expected. From 784.91mt last month to 785.74mt, an increase of 830kt. The surprise I guess came to increases in world consumption, basically countering the increase in production and some. The net result, a decrease of 590kt in world ending stocks, from 260.03mt to 259.44mt, but still too much.

Drilling down into the report, as boring as it is, confirms larger US ending stocks after a slight reduction in domestic use, up from 17.62mt in January to 17.9mt.

The bigger picture wasn’t quiet as bearish as a 13c/bu to 17c/bu fall in US futures might indicate though. That probably had a lot to do with the jump in the value of the US dollar too.

Major exporters ending stocks were reduced a smidge, just 180kt to 40.9mt. Major importers ending stocks were reduced 1.15mt to 169.16mt, also not a bad thing. Argentine production was increased half a million tonnes, to 15.5mt, more in line with the latest estimates. This was countered by a 500kt increase in Argie exports, so we see a very small adjustment higher to Argie ending stocks. Australian productions was left unchanged but domestic feed use was lowered 500kt (SFW1 v SOR1 ??), this amount was then put on top of the January exports estimates, increasing exports to 19.5mt. Considering current Aussie export bookings are roughly 9.7mt (8.6mt this time last year), one could assume 19.5mt isn’t out of the question.

The Canadian numbers were pretty much unchanged apart from a minor adjustment to carry in. EU ending stocks were increased 200kt, not much and once you look through adjustments to their imports and usage those adjustments could be questioned. The Black Sea states are the problem at present, Russian production was left unchanged at 91mt, actually everything for Russian was left unchanged from January. Ukraine saw a 600kt adjustment lower to domestic consumption, feed usage back 1mt but other usage up 400kt ?? and a 1mt increase to exports, there we no changes to carry in, production or imports.