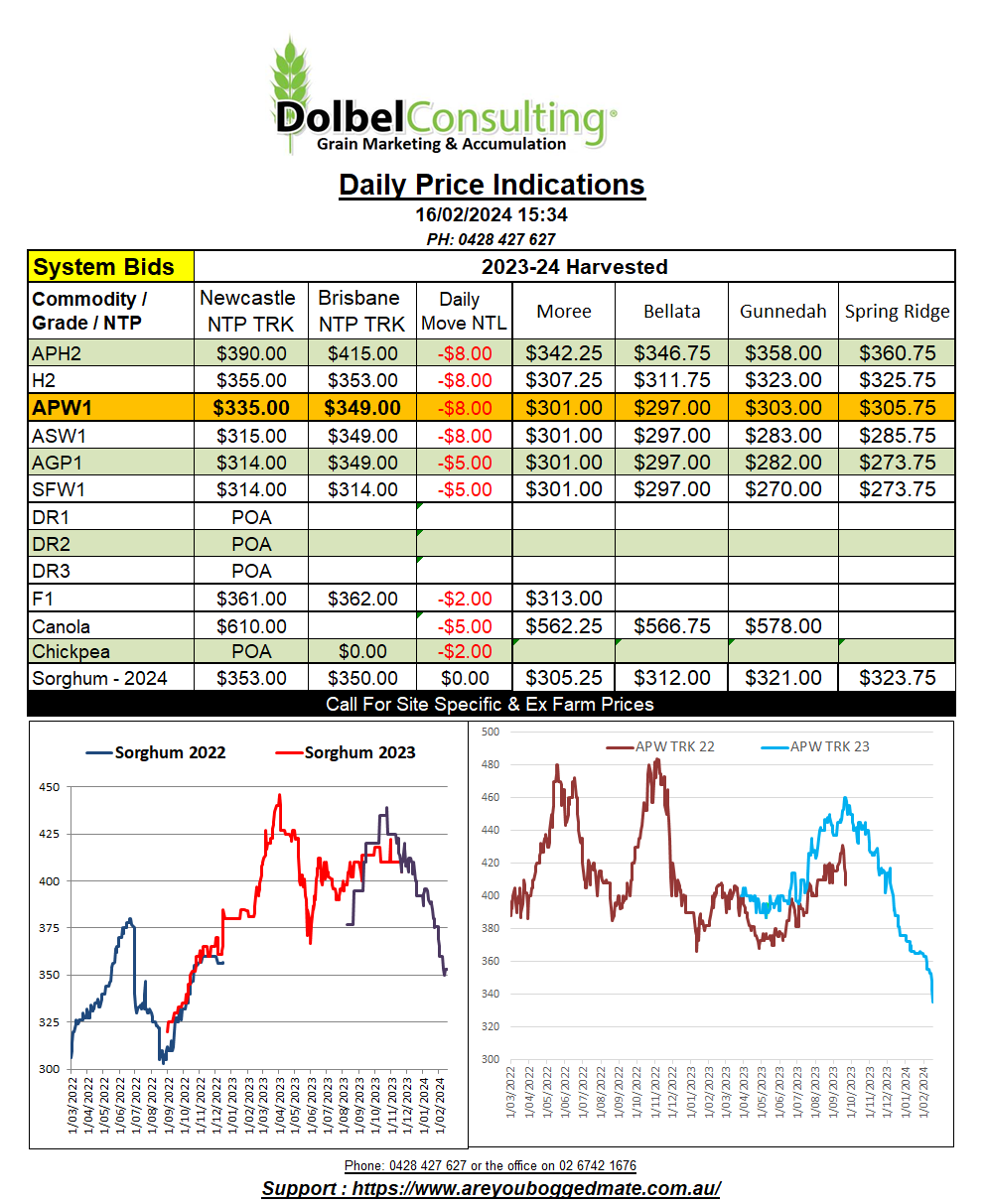

16/2/24 Prices

Egypt picked up 180kt of wheat. The lowest offer was from Ukraine at US$218.10 FOB Chornomorsk / Odessa. The offers were significantly lower at the FOB level then other offers. While the price was low FOB, the freight rates out of Ukraine remain higher, US$36.90 compared to just US$17.60 from Constanta, Romania, which was offered at US$237.40 FOB. All three parcels equated to a C&F price of US$255 Egypt.

On the back of an envelope this equates to something close to AUD$280 XF LPP, around 10% under current cash bids for east coast APW1 wheat. This is if Australian wheat was to be competitive into the Egyptian market. This also tells us that Black Sea wheat is still going to struggle to move into Pacific Asian markets at these values and indicates that recent port values here in Australia are still very competitive.

In world futures markets the slaughter of wheat continued. Nearby Chicago SRWW futures were back 18.5c/bu, in today’s money that’s about AUD$10.42 lower. Unfortunately this has coincided with another higher night for the AUD against the USD, and when taking that into account the day to day variation is closer to AUD$12.00 lower.

Using the latest wheat sales values into Egypt as a guide, one could argue for an improvement in local basis to Chicago, given we are already competitive in the Asian market. Yesterday basis to nearby Chicago SRWW was just +16c/bu, a far cry from the +57c/bu seen at the beginning of February.

The International Grains Council had a stab at world grain S&Ds last night. Global wheat production was left unchanged at 788mt, trade was increased 2mt to 200mt and carry over stocks were reduced 1mt to 265mt. This compares to the latest USDA stab at ending stocks of 259.44mt and production of 785.74mt. The IGC ending stocks number for wheat represents a year on year decline of 15mt from 280mt in 22/23. The ending stocks number is an 8 year low.