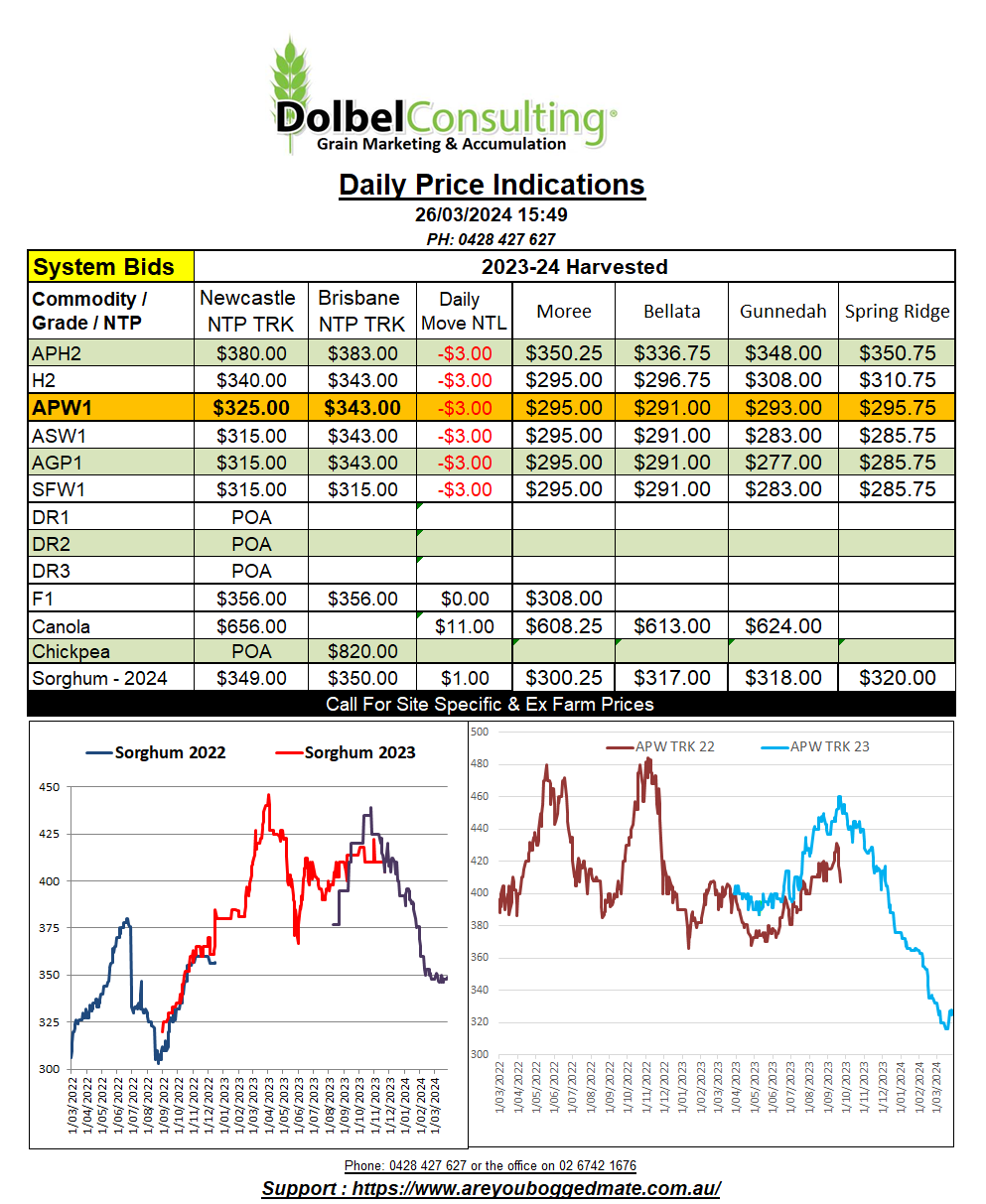

26/3/24 Prices

The clear winner in last nights futures markets was veggie oils. Canola and rapeseed futures took back any weakness shown on Thursday and Friday and some. The Chicago soybean contract was also higher, closing up 16.75c/bu on the nearby.

Canadian canola cash bids ex farm SE Saskatchewan jumped in unison with the futures market there. Bids for both old and new crop canola rallying roughly C$15.00 on the day.

The rally in oilseeds is a little against the fundamental flow but the punters are expecting to see oil seed stocks in the US lower in Thursdays USDA quarterly stocks report. The recent fall in soybean prices has the majority of punters expecting to see fewer soybean acres in the US than the USDA Outlook Forum had assumed in January. Some analyst see the area being closer to 86.7 million, some 800kac less than the USDA estimate, but still 3.1mac above last years area in the USA. Combine this with a 150mt+ Brazilian crop and it’s not as if supply is tight.

Canola crush margins in Canada remain healthy, encouraging crushers to persist at the current pace, which if continued will have no issue making the projected crush of 10.5mt. The current pace being 14% higher than the 3 year avg pace.

The weather in Europe is starting to co-operate. Conditions are still wet in some spots, and looking at the 7 days forecast any spots in France that had managed to dry out a little over the last few weeks may well see the heavier falls in the coming week. So it’s not all said and done just yet. Some analyst see the rain as a problem but as yet it has not had a major impact on yield estimates.

Large parts of central Russia and the Volga Valley are seeing less than average rainfall now. Some 30 day totals in the Volga Valley are less than 5mm.

Conditions in China remain generally favorable for the winter crop, good rainfall has been recorded across much of the main wheat districts over the last 30 days. If anything wet conditions across the SE of China may start to affect summer crop projections there.