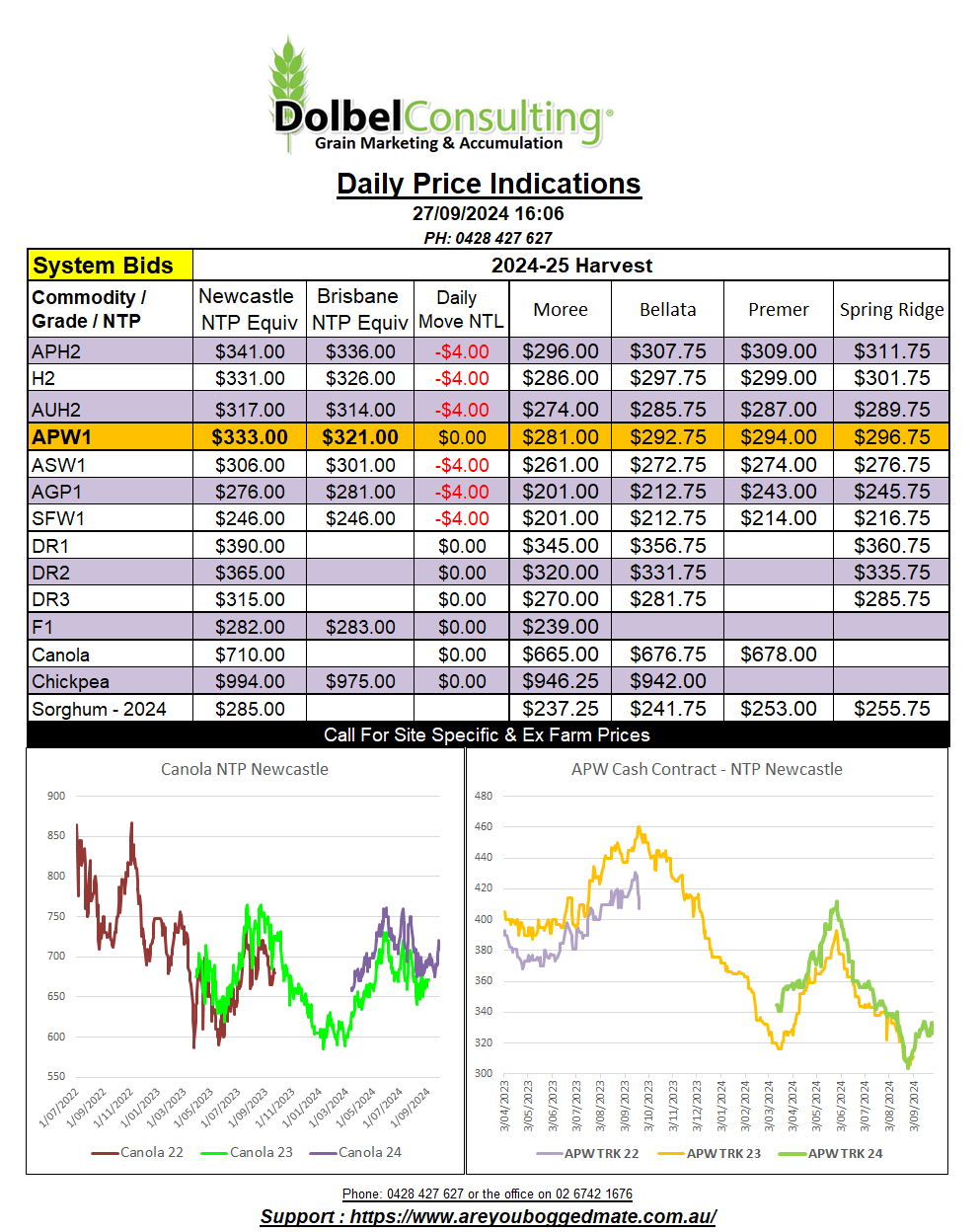

27/9/24 Prices

The Aussie dollar will take back what it gave us yesterday, up over 1% against the US dollar overnight. The bad news this morning is that we see the rally in the AUD coinciding with weakness in most US grain futures markets. Wheat, corn and soybean futures in the US all trended lower. The turnaround was put down to profit taking after the recent rally.

Fundamentally there has been little change to the production prospects of new or old crop grains in either the northern or southern hemisphere. Russia and Ukraine remain dry, disrupting winter wheat sowing. Australian conditions remain good apart from the recent frost event, Argentina remains dry and SE Brazil remains too wet. Meanwhile the US is seeing some delays to summer crop harvest and winter wheat sowing due to rain, but the rain is largely seen as beneficial with very little of the US now in drought.

Weekly US grain export loadings were mixed, generally considered good for soybeans, very good for wheat but poor for corn. The corn number coming in below even the lowest trade estimate prior to the release of the data. US wheat prices out of the Pacific Northwest were lower, not by much, keeping US wheat competitive into most Asian markets. Paris milling wheat futures were a little firmer in the Dec24 slot, gaining €0.75/t. This compares to FOB values out of France moving higher in Euros by roughly the same. The AUD is the party killer today, once these moves are converted to AUD per tonne we are looking at losses of between AUD$4.00 and AUD$7.00 per tonne, the AUD even negating the higher close in Paris milling wheat.

The AUD will hurt wheat, canola and chickpea conversions here today. For example Delhi chickpeas closed Rs21/q higher day to day, but when considering the AUD the day to day conversion equates to a day to day loss of roughly AUD$10.29 / tonne, not ideal. Canola is in the unfortunate position of not only being hurt by the stronger AUD but also being influenced by weaker Paris rapeseed and Winnipeg canola closes. Winnipeg shed C$10.50 / tonne in the January slot while Paris rapeseed in the Feb slot was back €3.50 / tonne by the close.