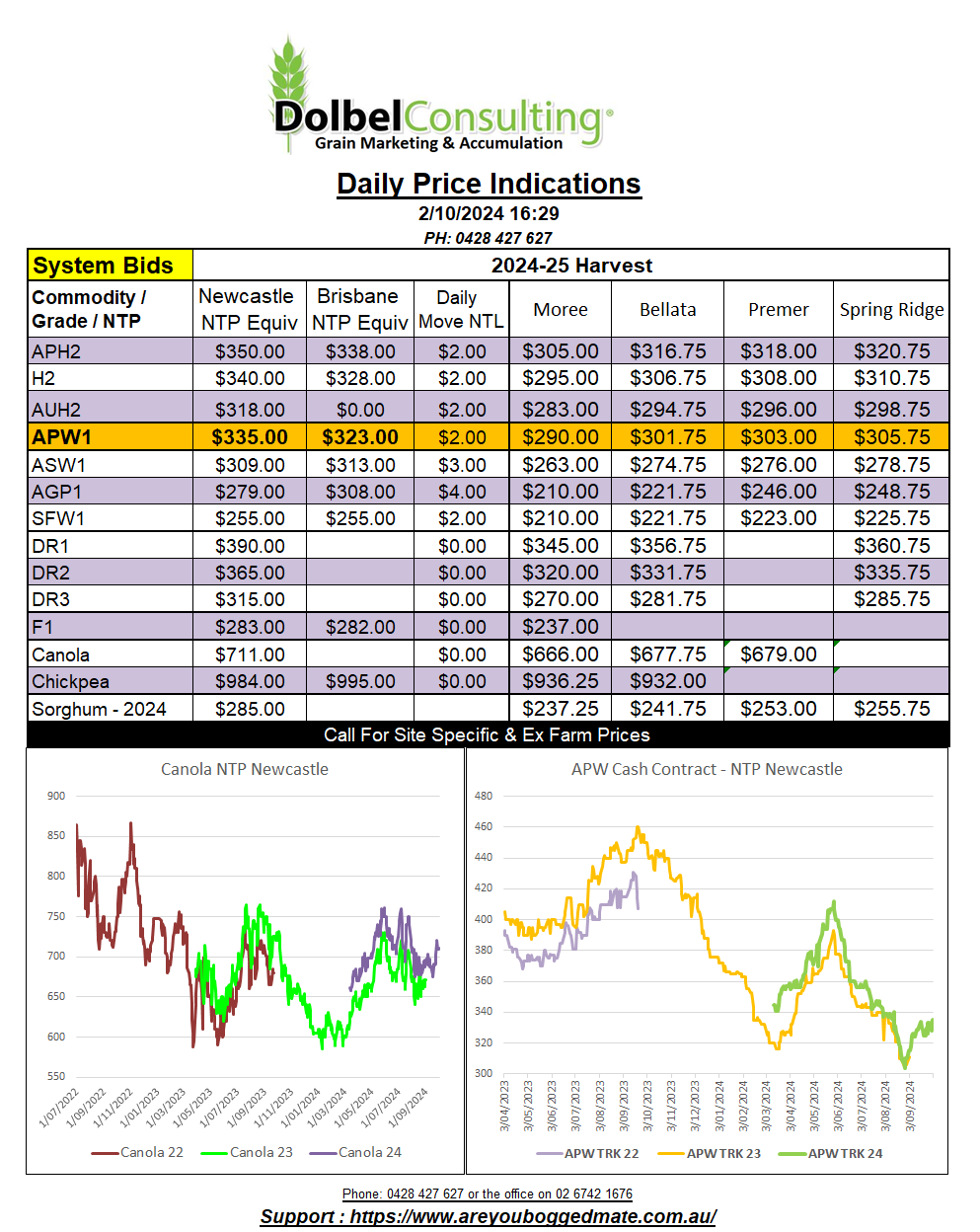

2/10/24 Prices

It appears Iran has entered conflict between Israel and ……… anyone nearby. I’m not about to take sides in this “war”, both sides have done their fair share of escalating things over the years, with neither putting in much of an effort to stabilise. I’m here to simply look at this from a grain market perspective.

Iran is expected to produce around 14mt to 15mt of wheat in 2024, with consumption around 13.5mt. Harvest is during April / May / June and sowing usually commences around late September through to December.

Depending on the season Iran can swap from being self sufficient to relying on a small volume of imports to top up domestic supplies.

This would indicate from either a supply or demand perspective Iran’s involvement in the dispute, and if it attracts further sanctions, will have little to no impact on the global wheat S&D.

As far as international wheat futures market were concerned the move was bullish. An escalation in both the Middle East and Black Sea conflicts was said to create some technical buying in wheat futures at Chicago pushing futures there to close 15c/bu (AUD$8.00) higher in the nearby SRWW contract. Paris milling wheat futures followed the US market higher. The Dec24 contract there closing €5.25 (AUD$8.43) higher for the day. US and EU futures were a wall of green last night, corn, wheat and oilseeds all pushing higher. Good moves in both Winnipeg canola and Paris rapeseed futures should combine with the weaker AUD here today to pressure local bids higher for new crop canola. Canola is starting to be windrowed north of Moree and will be on the ground north of Narrabri over the next 7 -10 days. looking at cereal values, canola may well be first to market again this year. Have you considered the ISCC scheme.

Thailand tendered for 180kt (3x60kt) of feed wheat for Oct / Nov / Dec, no results as yet.