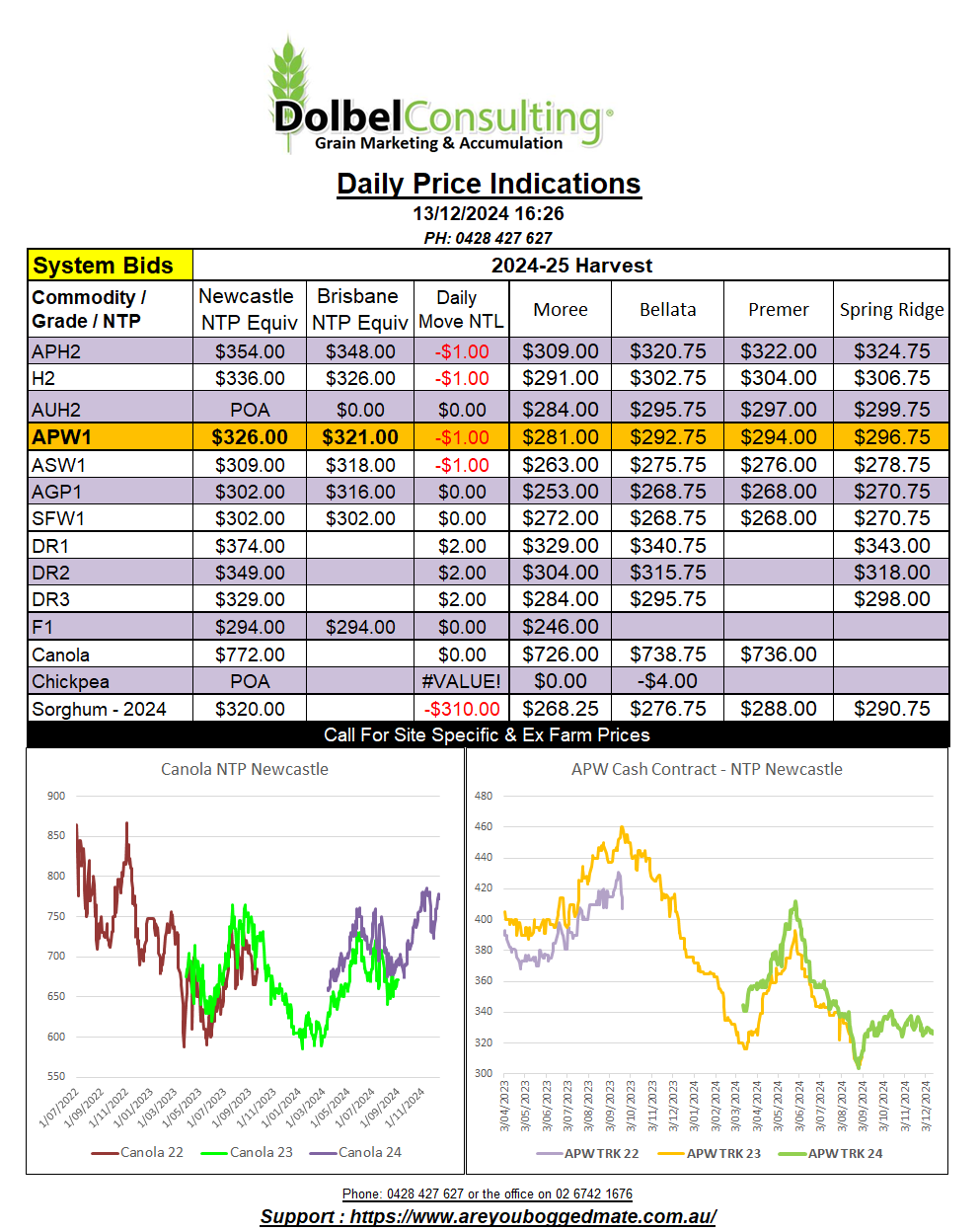

13/12/24 Prices

International Commentary

There’s not a lot of green on the screen this morning. US, Paris and London wheat futures all closing lower. The AUD remains under 65c US, which is helping but lower futures may weigh on local bids today. As mentioned yesterday local basis was hit hard as the US market rally in futures was generally not reflected in local bids. This saw the premium that APW on the track had over Chicago March SRWW futures eroded from +34c/bu on the 2nd of December to just +4c/bu yesterday. At today’s exchange rate the erosion in basis is equivalent to roughly -AUD$17.31 / tonne.

Russian FOB wheat values recovered a little overnight after reports showed a significant collapse in value in the previous session. With Russian exports slowing significantly, and projected exports reduced for the last half of their export program, one can’t help but think that Russian values should be moving higher, not lower in the short to mid term.

Looking more closely at the Asian market we see the US PNW values back in line with the reduction in US futures. The weaker AUD is countering this decline, keeping the fall in check in AUD/t somewhat but still indicating potential losses of AUD$2.00 to AUD$3.00 are possible today unless we see a turnaround in basis.

Saudi Arabia is in for 595kt of feed barley for Feb / April delivery. Russian values C&F S.Arabia do appear to have the edge over Australian feed barley values by up to AUD$30.00 at present. Russia’s geographical advantage into the Saudi market will be hard to compete with, but supply issues and the volatility in government policy may put WA barley in the mix. French values remain higher than Australian values C&F S.Arabia. Once we see the tender values we can convert to an Aussie equivalent and potentially compare to domestic values here on the east coast. Currently one would calculate export parity at close to AUD$285 to AUD$290 XF LPP using China as a consumption point. Implying that local prices are well priced for export and shouldn’t fall lower.

Sorghum values FOB US Gulf were roughly AUD$2.00 lower in overnight trade. US export sales of sorghum have slowed significantly, just 6.3kt last report.

Domestic Commentary

Local markets were generally quiet, the trade appear to have good coverage for domestic and export positions at present. There are still a few slots for ASW into Tangaratta through the trade at $320 for Jan / Feb. SFW1 into the LPP end user market was bid at $290 end user but bids were thin (closer to $305) on the ground as offers to sell dry up. SFW1 into the Newcastle end user market was unchanged at $330 delivered Jan / Feb.

Feed barley was steady at $280 delivered LPP end user with most traders happy to book at $260 ex farm. Overnight world feed barley values were mostly a flat to a little softer. The average move when bundling S.Arabian and Chinese C&F values was roughly $0.50/t. Spot oat demand at $275 / tonne XF LPP.

Chickpeas fell away a little yesterday as shipping delays push arrival dates to India into March. The current season has been very dry in India. Official estimates expect Indian area under chickpeas to increase 7.14%. Higher Indian prices have been eroded during the sowing period which is just starting to wind up. The increase in chickpea area appears to have came at the expense of oilseeds. If the season is good and there is no issue with irrigation, which there shouldn’t be, the potential for chickpea prices to fall further, to MSP values, is high.

New crop sorghum values were unchanged, track bid at $315 less GTA, $288 delivered G’corp Werris Creek, or $350 for direct delivery to the port by road, roughly equivalent to $310 ex farm C-LPP. Compared to SFW1 at $290 XF C-LPP sorghum is probably the better sell at present.