20/12/24 Prices

A mixed night on the world futures markets for grain and oilseeds. Wheat trended lower with losses at both Chicago and Paris. Milling wheat futures at Paris saw €3.75 / t (AUD$6.23) shaved off the nearby contract and €3.00 (AUD$4.98) off the May slot. London feed wheat was back £1.70 (AUD3.41/t) nearby and Chicago HRWW futures fell 5.5c/bu (AUD$3.24/t) nearby March. Chicago soybeans gained 11.25c/bu nearby (AUD$6.62/t), dragging both Paris rapeseed and Winnipeg canola higher. Palm oil futures were down 63MYR/t (AUD$22.39/t), rapeseed, canola and soybeans all turning the other way.

The AUD is trading at 62.48 this morning, just 10pts above the session low of 62.38. The US FED cut rates by 25pts, a job preservation move or are they predicting some interesting times ahead. The AUD remains under pressure from not only a stronger US dollar but also from the fact we have now completed seven consecutive quarters of recession, the longest on record. If local retail is any indication of the impact this is having on the economy I can confirm, it ain’t great. The failure of the Aussie economy, should continue to pressure the AUD lower. We just need to see the trade reflect this weakness in domestic bids. Something that has been hard to do considering the AUD sliding at a similar pace to the value of many international grain prices sliding at present.

World cash grain values were mixed, in line with mixed futures markets. The weaker AUD did help buffer the decline in some grains but could not counter 100% of the decline in wheat, barley and sorghum values. Sorghum FOB US Gulf slipped just under AUD$1.50 lower. Weekly US next export sales were bad for sorghum, total sales reduced by 59.2kt, a marketing year low. Further sales of sorghum were reported, 7.8kt to China but the 67kt total reduction in the unknown buyer slot for export sales was the clincher.

Net US weekly wheat sales were OK at 457.9kt, up 58% from the previous week. The larger sales generally into the Asian market.

Locally a mixed day with various commodities moving off the plains. Feed faba beans found buying interest at $415 ex farm C-LPP. The trade were more reluctant to bid on the No1 fabas after recent declines in export values.

Chickpeas were also mixed, with more subdued buying interest. A rally in Delhi market values earlier in the week is slowly being eroded, even when values in India are converted using the weaker AUD. Overnight the Delhi market was back around 27Rs/q. Compared to yesterdays conversion and considering Rs/AUD conversion, this is equivalent to a decline of roughly AUD$9.47 / tonne today. Although Delhi market chickpeas are still showing a week on week improvement, the trend does appear to be lower in the short to mid term.

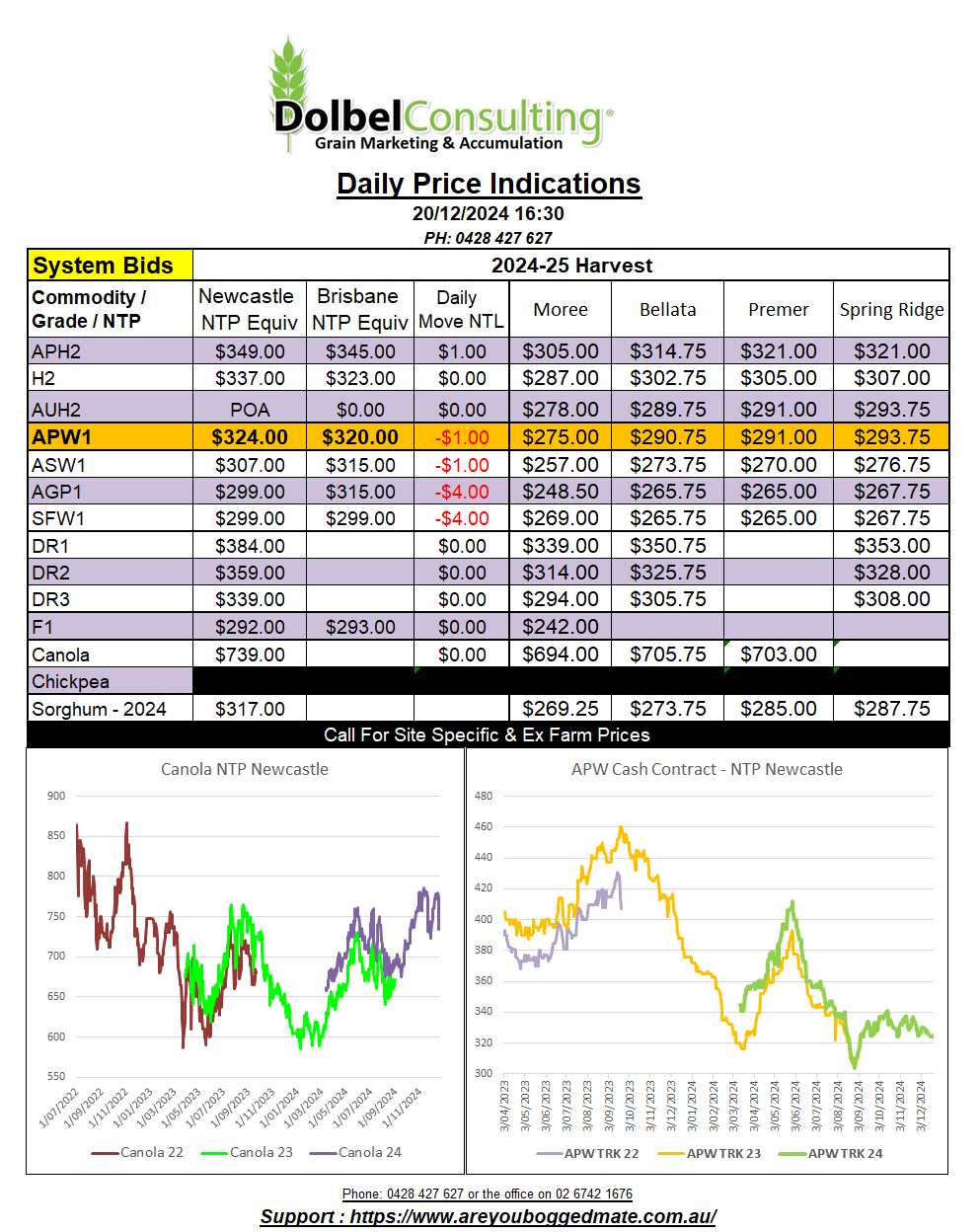

SFW1 wheat changed hands at $295 delivered LPP end user for the January slot. There were bids up to $288 ex farm but these positions were not into the local market. Delivery slots for SFW1 are more easily accessed for the later months, Feb / March, and for some buyers, April. If you have silos that need to be cleared prior to sorghum harvest you would be wise to consider getting this grain sold sooner rather than later.

Volatility in the wheat market should remain minimal. There is plenty of wheat in NNSW to cover the domestic market and export orders on the stem are not as high as one would need to see to create some track shorts in the new year. This may change, and should change, but at present the trade is not making this type of booking or sales data available in any way, shape or form. The stem report for Carrington shows just 50kt of wheat booked to leave against 61kt of chickpeas in December. The January slot 55kt of wheat and the Fed / March / April nominations for Carrington are yet to be made public.