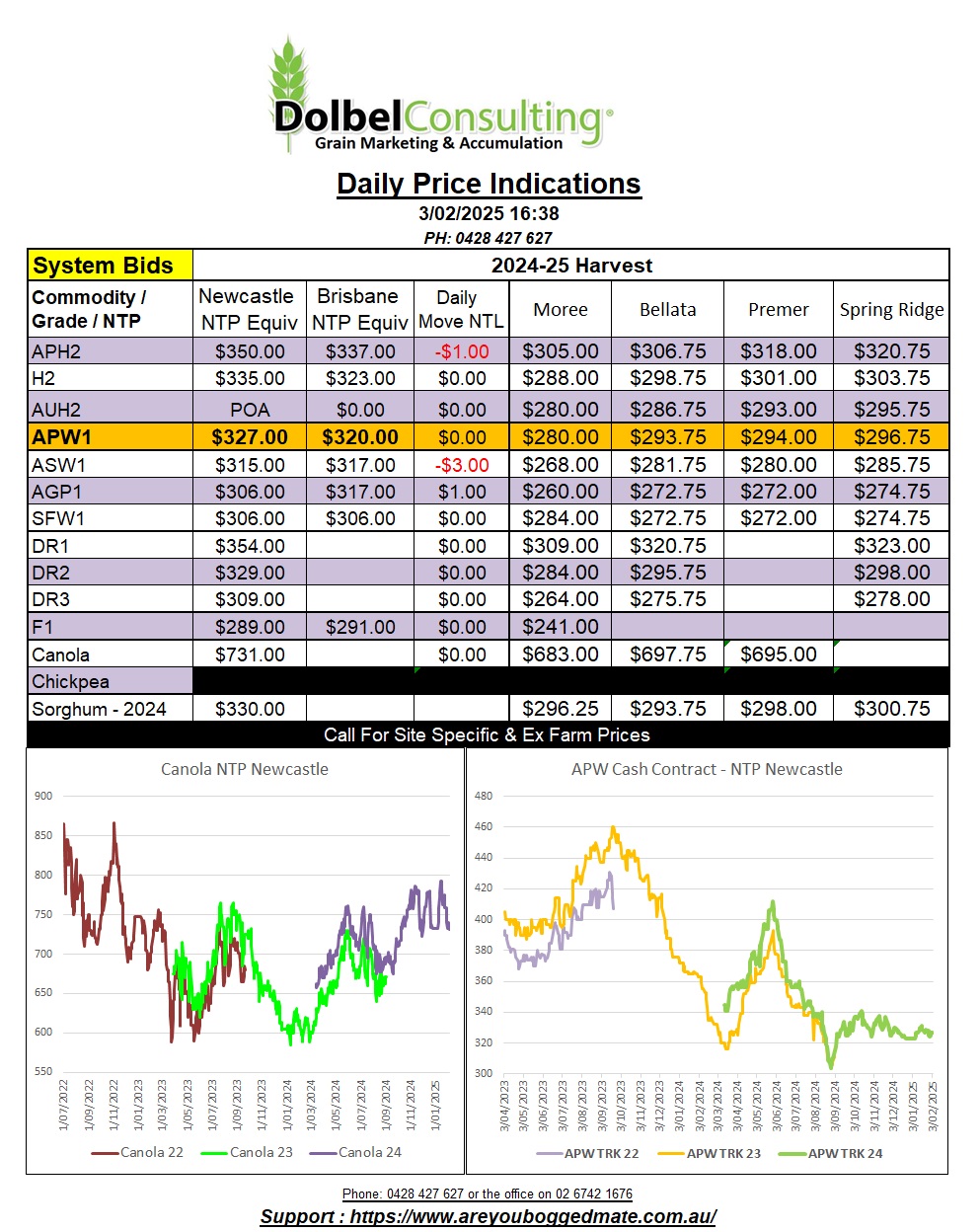

3/2/25 Prices

World grain futures values closed lower overnight. Trump tariff concerns and pressure from lower closes for the US stock market and crude oil all weighed on the grain markets. After a couple of higher closes in wheat there was a degree of profit to be had. All three US wheat grades gave back value, Paris milling wheat futures followed the US market lower.

Soybeans at Chicago fared OK, lower but only by 2c/bu nearby. Winnipeg canola futures were lower. Paris rapeseed was mixed. Someone was obviously caught short nearby, the Feb contract closed €22.25 / tonne high. I bet someone had a sleepless night. The outer months for Paris rapeseed were not as volatile, May down €1.25 and August up €1.75 / tonne.

The weaker AUD will help counter the move lower in US, EU and Canadian wheat values. HRWW out of the PNW compared to yesterdays conversion into an Asian market fell just AUD$3.54 / tonne. White wheat out of the PNW was flat in USD, thus due to the weaker AUD we actually see a slight improvement for white wheat this morning.

I was trying to find some decent speculative reading on Trumps vs the world with tariffs and the best line I read all day was “this last season of USA is heaps better than season 8 of Game Of Thrones”, I concur. Granted the US wields a heavy sword in the fight for dominance in many markets but buyers, and sellers, have a long term memory. A like to use the barley / wheat feed ration demise as a good example of what happens when the price of something becomes unpalatable or there is simply not enough available at the right price to make it viable. During the last drought we saw so many feed wheat over barley, and they learnt how to do it properly. Now we see much less barley in feed rations than prior to the drought. If the US and a tariff war send other nations into “drought mode” it may simply be the USA who ends up paying. I’ve said all along that Australia and it’s non reliance on the US as a major trade partner may well serve up well in the long run if our government isn’t drawn into a Trump like standoff with our own trade partners.

There was almost a pulse in the local wheat market yesterday, almost. Bids for H2 and APH2 on the track were firmer. The trade wasn’t chasing the market higher but was willing to give back some of what can only be considered deplorable basis to Chicago, in order to get some tonnes booked.

The offers side was tougher than the buy side though, resulting in a lot of bids and offers for not a great deal of wheat changing hands. For those that were trying to sell and failed to yesterday, Monday may not brings as high a price as Friday. Currency is working with us but world cash and futures markets moved lower on Friday. Yes, there is a tonne of basis buffer factored into local bids but the trade will not miss an opportunity to talk values lower.

Longer term may find support, world fundamentals are improving and the trade is establishing further short positions into the local consumer market.

Yesterday there was talk of trade sales into the LPP market. ASW was bid at $327 delivered Tamworth to the producer, roughly equivalent to $305 XF C-LPP. This isn’t hugely different to where this market has been trading for a while now but should continue to offer liquidity to those with wheat on farm looking to move it somewhere other than the port during the March / April period.

ASW was bid at $293 delivered Graincorp Werris Creek yesterday. The buyer leading the pack suggested this wheat was destined for export. Looking at it from a local perspective, executing it by road to Tamworth would offer the buyer a delivered Tamworth price of about $330 +/-. This does tend to indicate that the $327 delivered Tamworth bid may still have a little fat in it.

H2 at Werris Creek silo changed hands at $310 and APH2 was bid at $335, both grades destined for export.