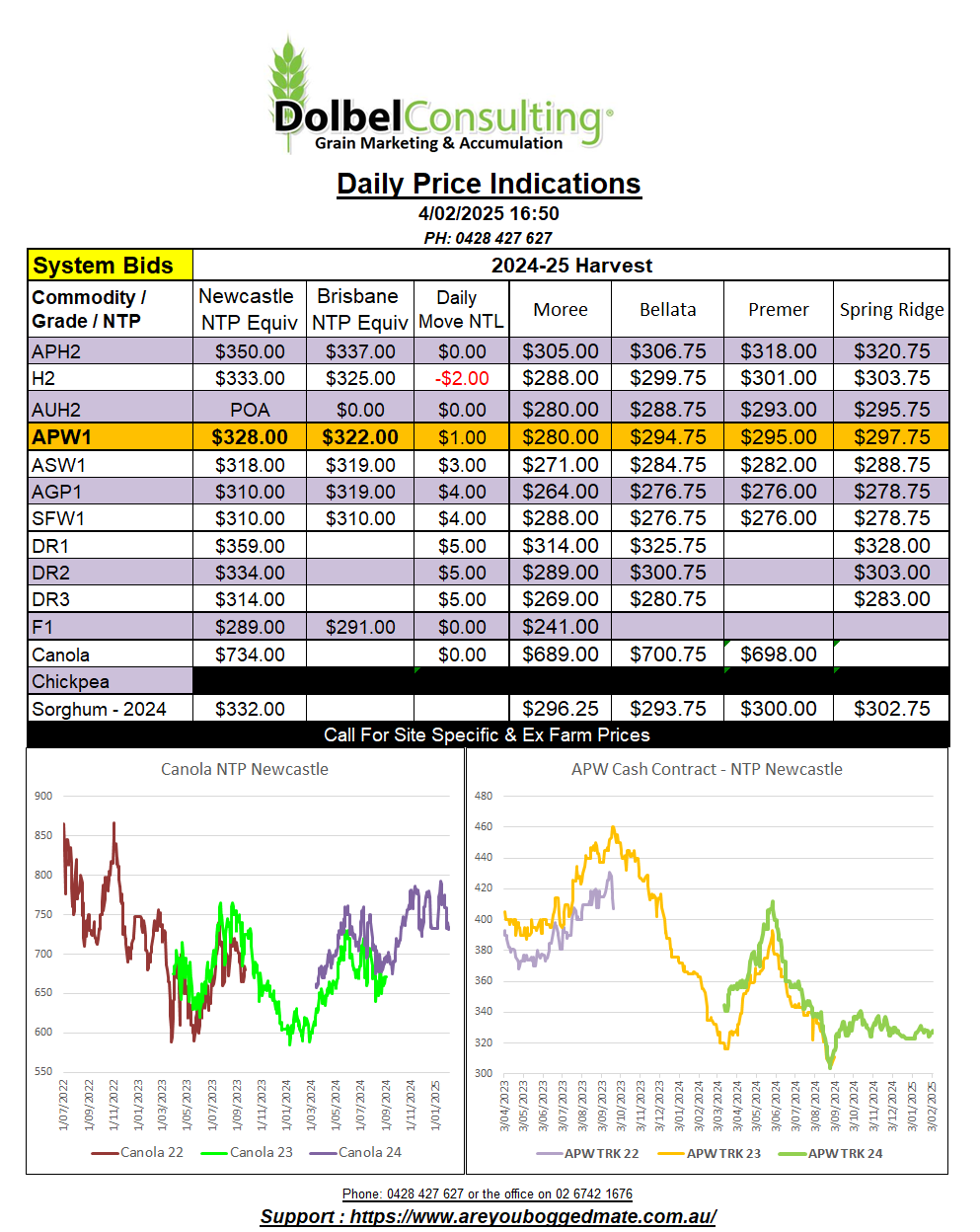

4/2/25 Prices

US and EU grain futures staged a slight recovery overnight. Improvement in US soybean values dragged both Paris rapeseed and Winnipeg canola futures higher. Better closing corn futures saw some improvement in FOB values for sorghum out of the Gulf but Chinese values continue to show little desire to track the move higher in US values (see chart). We may get some better direction from the Chinese market this week now that people are returning from New Year holidays.

US wheat futures closed higher, as did both Paris milling wheat futures and London feed wheat futures. Paris milling wheat gained €2.50 in the March slot and €4.25 in the Dec 25 slot.

Delhi market values for chickpeas traded a wide range of 6045Rs/Q to 6355Rs/Q, closing at 6200Rs/Q an increase of roughly AUD$18.86 / tonne when taking the fall in the AUD into account.

The AUD pushed to a low of 61.38 overnight before recovering throughout most of the session to close at 61.84. The day to day fall in the value of the AUD is worth roughly AUD$1.41/t against nearby US SRWW wheat futures.

Talks between Trump and Mexican President Sheinbaum has seen tariffs put on hold for 30 days. Mexico has agreed to send 10k troops to the US border to help stop illegal passage. What could possibly go wrong, I’m sure this will slow both fentanyl and illegals, let’s check the procedure, stop, search, confiscate, consolidate, sell. As for US ag exports this isn’t bad news for the corn market. The Canadians may find themselves less capable of bargaining unless that take a whole new approach to their own border security, not just the Canadian US border. In the meantime both US and Canadian wheat values out of the PNW are higher, due to better values in native currency and the decrease in the value of the AUD.

Local markets, like international markets, are showing mid to longer term nervousness as Trump starts to announce US tariffs against many of their major suppliers and consumers. This is placing additional volatility into a historically already volatile time for the wheat market, the start of the northern hemisphere spring. It’s hard to say what impact the US tariffs will have on our domestic grain value. I might hazard to guess very little negative influence, but it does muddy the water when trying to use traditional pricing benchmarks or indicators.

At the moment we see the fund managers piling into US grain futures. This is possibly a hedge against US inflation. It’s a standard strategy that has worked for the funds in the past and should work again. This time around is a little different though, the inflation is likely to be driven by tariffs, not debasing currency, (although that is probably still on the table), or a short fall in wheat supply, (although that is still possible). This may see US domestic grain prices increase, following higher futures. International values may increase a little, but the cost of the increase in the US will be born by the US domestic consumer. Thus we have tariff driven inflation. Without proper support for businesses and households this type of inflation could see significant corporate consolidation in their domestic businesses. Longer term hungry people do get angry though.

Here in Australia we will need to track export parity, or more importantly C&F values of major consumers, much more closely than things like futures values. The disparity between futures and cash has been an increasing concern for years now, it may get worse. There is a chance futures markets will become even less indicative of international cash prices as time goes on. It’s not above international traders to take advantage of this lack of clarity.