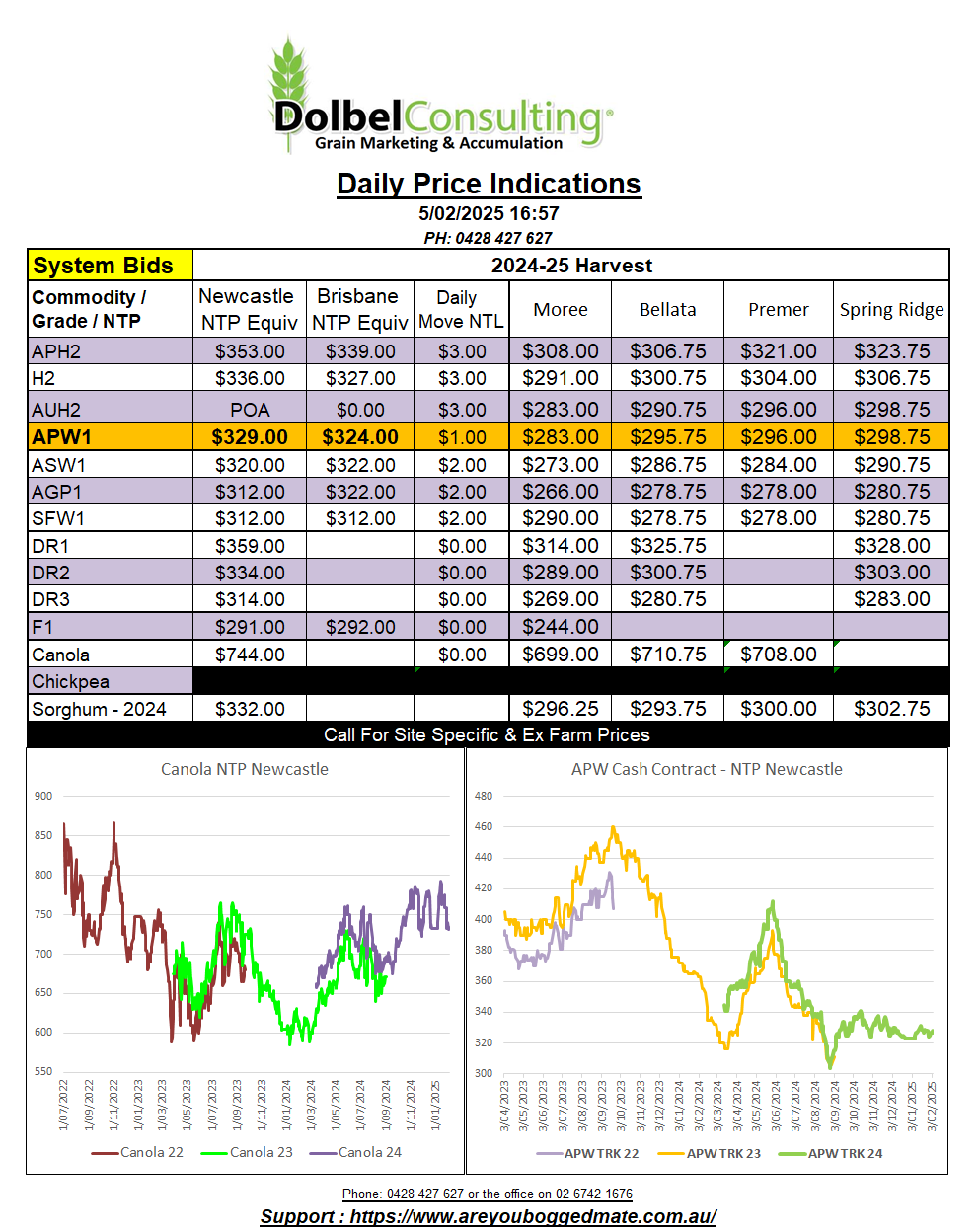

5/2/25 Prices

Trump held off on the implementation of tariffs against Mexico and Canada but implemented tariffs against China. China then confirmed their introduction of tariffs against a raft of US products. This includes a 15% levy on LNG and coal, 10% on oil, farm gear and possibly electric trucks from Tesla. China also confirmed the restriction of exports of rare earth minerals to the US, minerals crucial to the US tech industry.

Back in the “real” world US wheat, corn and soybean futures all continued to push higher. The stronger AUD will counter some of this strength. Wheat for example, the move in the AUD is equivalent to about -AUD$4.11 per tonne when converting nearby SRWW futures. The rally in futures was equivalent to roughly AUD$6.02, so still a net gain in AUD per tonne. Wheat ignored the lower weekly sales and export data out of the US, instead focusing on the bigger picture, year on year improvements and continued good numbers for corn and soybean exports. Although corn was back 18% week on week, net sales of 1.36mt is still very good.

EU wheat exports remain poor, down roughly 37% year on year. The EU is not alone, Russian wheat exports too are failing to meet 2023-24 or 2022-23 volume with some analyst expecting to see as little as 42.8mt exported this year and as little as 38.3mt projected for export in 2025-26. The January WASDE had Russian wheat exports down for 2024-25 at 46mt. Although back 1mt on their December estimate still much higher than the estimates of SovEcon.

The main Russian winter wheat regions remain very dry. Much of the Volga valley has seen less than 40% of normal precipitation over the last couple of weeks. The 30 day anomaly is also showing conditions are drier than average across much of the black soil country. With the forecast remaining dry across Russia for the week ahead, Russia will need to see ample spring rains to recover to build subsoil moisture or crops will deteriorate quickly. The EU is mixed, rainfall has generally been good across western France and Germany, England and Spain while conditions are dry to the east. The US is drier than average.

New crop sorghum was bid at $360 delivered Newcastle port for April / May delivery by road yesterday. Ex farm bids were a little harder to secure, some buyers more prone to let the producer organise road freight this year.

Overnight international sorghum values were stronger in native currency but the firmer AUD has eroded much of the chance of upside for sorghum here today if using these international values as a guide. US values once converted to AUD port comparative using China as a consumer are back between AUD$2.00 to AUD$4.00 this morning. Possibly weighing on local bids. US weekly export sales were again zero. The US shipped just 600t to China between the 17th and 23rd of January.

The AUD climbed for much of the session, closing near its high. The US has delayed implementing tariffs on both Mexico and Canada but a 10% tariff was realised on Chinese imports. This saw the international money market breath a little easier but should result in longer term strength in the USD over the Yuan.

There was limited demand for prompt barley XF LPP. This market has stagnated in recent weeks with limited interest from the trade / consumer. Yesterday saw a little trade short coverage at $262 ex farm. There was carry available for outer months but the carrot wasn’t especially tasty. Some buyers are still showing bids as low as $257 ex farm C-LPP for BAR1 for April / May delivery. BAR1 bids into the border feedlots were a little firmer at $302 delivered March / April, roughly equivalent to $262 ex farm LPP. Downs consumer bids were closer to $317 delivered, equivalent to a sub $260 XF LPP.