17/2/25Prices

It appeared to be all about US wheat futures last night. Lately the futures market seems to be responding more like a “past” market than a “futures” market. The USDA will release some slightly bullish data, say good export numbers, on the day the market will fall, only to rally the following day. The US will show a poor weather outlook, the market falls on the day the data hits the floor, only to rally the next day. Maybe a generational change ?

So what triggered last nights move in US wheat futures ? The wires are calling the rally on the back of cold, dry conditions in Russia, nothing new there. The initial buying triggered further technical buying and away the fund merry go round went, where it stops, or breaks down, no body knows.

France confirmed that their winter wheat crop is all sown as of Feb 10th, as one would hope, and that it is currently rated at 73% good / excellent, which basically means nothing in Feb. Last year we saw the French crop rated at 68% this time of year and look what happened.

Jordan cancelled there wheat and barley tender….again….that’s the fourth time. They might be regretting that looking at the markets this morning. See how they go next week when the print another tender to cancel.

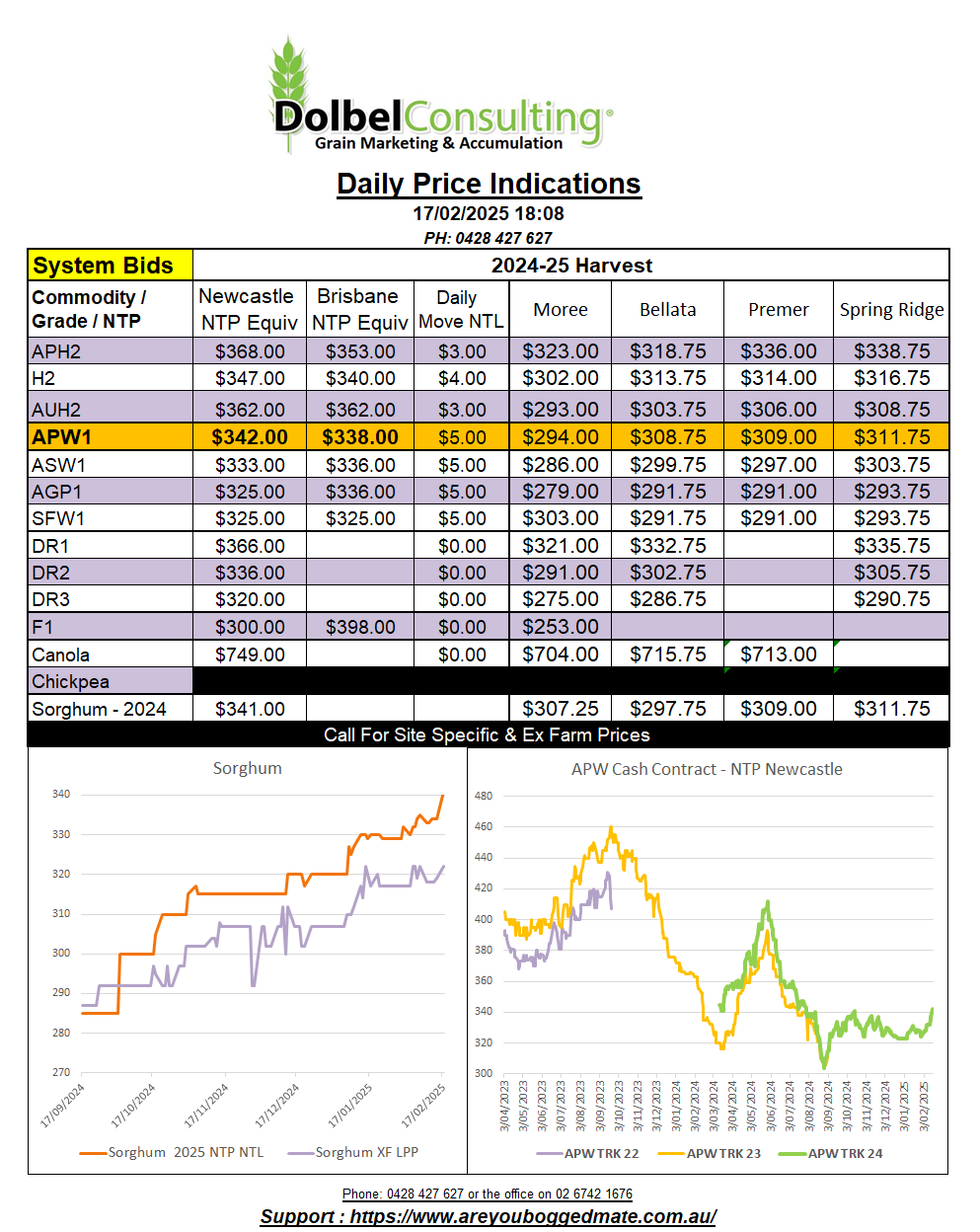

Corn and soybean futures found limited support from a lower week on week rating of the Argentine crop. Just 15% of soybeans and 16% of the Argie corn crop is rated in good conditions. Corn shows a massive 33% below normal, a 7pt increase week on week. Worldagweather.com shows 7 days rainfall across much of the major summer crop region of Argentina at roughly 10-30mm, there are still plenty of dry spots though, obviously given the crop rating. This may also go some way to explain the recent rally higher in Argie sorghum values, up more than AUD$4.00 / tonne compared to yesterdays conversion this morning, and that’s taking the stronger AUD into account. Aussie sorghum is still cheaper though.