12/5/25 Prices

The Canadian spring program is progressing nicely, as of May 5th data confirming the state off to a good start . Across SW Saskatchewan, prime durum country, sowing is ahead of schedule with around 44% of the projected acres now sown. Saskatchewan durum is estimated at 33% sown across the province. Spring wheat is 13% sown across Saskatchewan and canola is estimated to be 10% sown.

Spring wheat values across the Canadian Prairies continue to closely track US spring wheat values. Overnight the average price for 1CRWS13.5% milling wheat ex farm SE Sask fell by C$2.65 nearby, and C$3.11 / tonne for an August pickup. Durum values across SE Saskatchewan have been fairly stable this week, bid on average C$344.07 / tonne for prompt pick up ex farm, or $312.79 / tonne for a September pickup. The new crop value would equate to something close to US$405 CiF Europe. This is probably a little more expensive that Italian durum at present, not a lot though. On the back of an envelope it would also suggest that current bids here are well below where they should be. Potentially closer to AUD$400 – AUD$450 XF LPP (with a trade margin deducted), than the current bid of AUD$415 NTP Newcastle we are seeing for new crop.

The forecast for much of Alberta and Saskatchewan over the next 7 days looks good for those seeking a 15-30mm of rain to get the crop up and away. Something to note is the very dry conditions across S.Australia this year. Although Australian domestic durum demand is minimal, we may see consumers from the south trying to accumulate NNSW durum at a premium to the export market in 2025-26, unless conditions in the south turn around in the next 4-6 weeks.

It may be a toss up between what makes the best headlines early next week. A USDA WASDE report, or trade negotiations between China and the USA. The two a set for negotiations this weekend, the US already confirming they are willing to halve current tariff values if China will negotiate favorably.

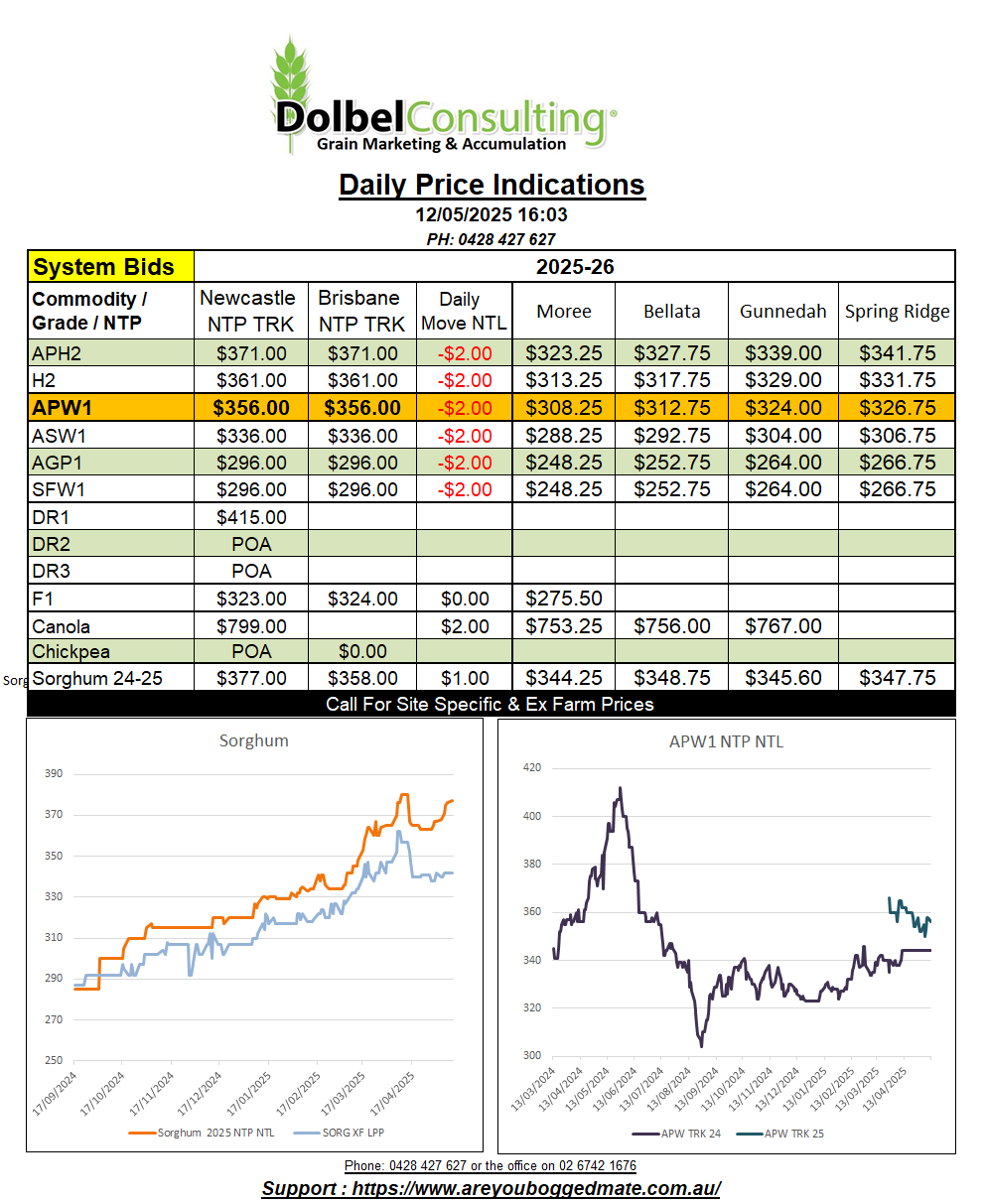

Very quiet yesterday, more of the same. The markets are starting to look a little like the weather, one day like the last. There was a little track sorghum on offer to the trade at $382 NTP Newcastle. The trade didn’t quiet get there in the end, closing the day bid at $377 NTP NTL. There was a couple of dollars carry for a June transfer and a July first transfer actually saw the $382 bid.

The smaller traders continue to struggle against the majors who are accumulating boats for June / July / August. The values being paid to the producer for bulk accumulation currently, do not support a margin on current sales values. This may stifle box trade considerably as we move into Q3 but once the boats are full and the major traders start to concentrate on new crop winter grains in September, it may free up the sorghum market for the box trade, if there’s any left. Prices may fall away to mop up tonnage from those that missed the bulk program the trade sold earlier in the year.

There was demand for old crop SFW1 at $340 delivered LPP end user and $347 delivered Downs. Volume on the offer side is minimal, some producers electing to feed wheat through their own stock, others watching the tightening S&D at the local level and poor conditions in the south, hoping for better prices in the new financial year.

Conditions in southern NSW, western Victoria and S.Australia remain very poor. South Australia is in very bad shape with some locations of the Northern Wheat Belt seeing just 5mm of rain for 2025. Parts of the WA wheat fields are also starting to feel the pinch after a pretty good start, sown acres reducing.