13/5/25 Prices

The USDA weekly crop progress report was out after the close. This weeks report has corn pegged at 62% sown, 6pts above the average. Soybeans 48% sown, 5pts above the average. Sorghum at 26% sown, bang on the average, and spring wheat at 66% sown, well above the average pace of 49% sown. Around 27% of the spring wheat has emerged.

The US winter wheat crop condition rating improved again, up 3pts in the Good to Excellent rating to 54%. The Kansas HRWW crop is now rated at 48% G/E, up 1pt from last week. The Kansas HRWW crop is now estimated to be 71% in head, up from 45% last week. The last 7 days has been relatively dry across Kansas, and the forecast is showing scattered showers in the central and eastern districts, with lighter falls to the west. The amount of rain in their forecast isn’t likely to result in a vast improvement in the rating week on week, but one would not expect to see a decline next week either. Thus we could probably view the weekly report as more bearish than bullish wheat in the short term.

Cash values for HRWW out of the US Pacific Northwest were generally down a dollar or two compared to Fridays conversions. White wheat values were also a little lower, less than a dollar. The weaker AUD has gone some ways to buffer a potentially sharper decline.

French values were lower at the FOB level at some ports, while Paris milling wheat futures were up €2.00 / tonne in the December slot. The later move higher does tend to reflect their weather map a little more closely. According to WorldAgWeather.com conditions in N.France, Germany and Poland continue to deteriorate. The forecast has no usable rain predicted for these regions and the last 7 days. remaining mostly very dry. We should expect to see a decline in winter crop quality rating from Europe in the next report.

Last night also saw the May USDA WASDE. The first of the 2025-26 estimates for wheat. Production is a little large at 808.52mt, but ending stocks are not too bad at 265.73mt, comparable to the current ending stocks of 265.21mt. Australia is in at 31mt, a tall order that one. China also pushing it at 142mt.+

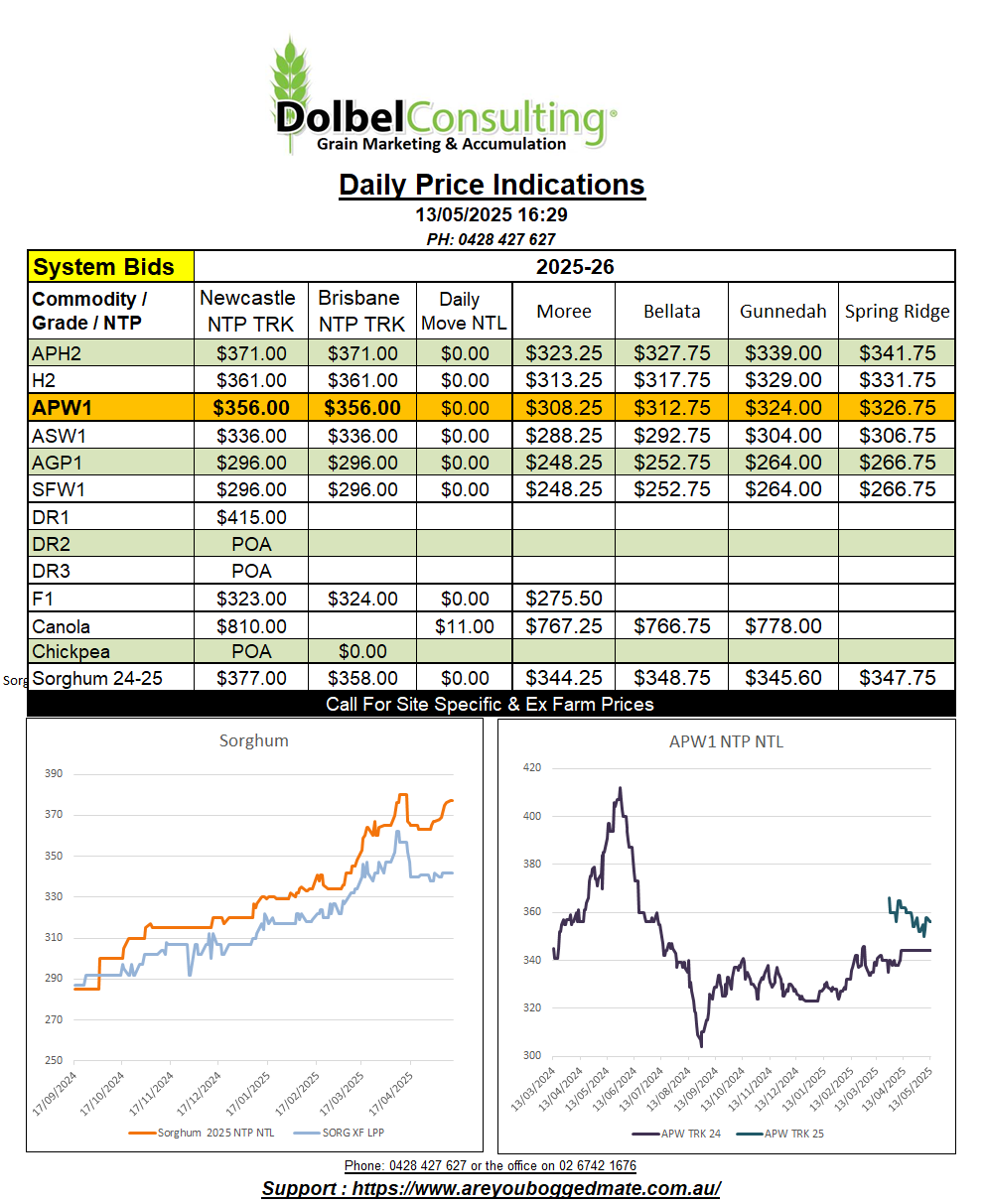

Local markets were very quiet. Sorghum continues to trade both on a delivered port by road basis and on the track. The bulk export traders continue to accumulate at what appears to be values well above where current sales would be capable of being made. Not a problem for the producer, selling sorghum at Prime Hard values is never a chore. Nothing new for the Newcastle port on the shipping stems.

If the current projection for sorghum out of Newcastle is correct, roughly 394kt, it means we need to see another 180kt appear on the stem over the next 3 months, That’s not a lot at 30kt-50kt per vessel. The biggest question on this tonnage is where will accumulation come from. Logically the Liverpool Plains is the primary choice. The balance coming from the Narrabri / Moree area. Production on the LPP is currently estimated at roughly 275kt, a little lower than an average crop which is typically closer to 320kt-330kt. With zero carry over (or carry in) considered, this would leave a balance of 120kt to come from the north of the state. Not a big call given production north of Narrabri is estimated at 255kt (NNSW 529kt). One would expect less than half to run north to Brisbane port or the Downs packers considering both SE QLD production, and the price differential for Brissy ($385) / Newcastle ($387) this year.

From a basic S&D perspective we can’t factor in domestic demand, at these levels it will be minimal, maybe 5kt, if at all. That would give us bulk demand of 394kt for Newcastle zone, plus boxes. The price for boxes hasn’t been great lets factor in 5kt, I’ll try and proof this estimate today. This still gives us a carry out of something close to 124kt for NNSW, approximately the same volume one may expect to see move to the QLD port / packer market. This basic S&D does tend to tell us why the trade is sustaining a strong basis to current international values I guess. There is plenty left to buy in QLD though.