9/5/25 Prices

A stronger US dollar, and better crop ratings for the US winter wheat crop continued to hurt their futures market. The weaker AUD went some way to buffering the decline in futures, but may not cover it all. Further technical selling leading into next weeks USDA WASDE report was also evident.

The competitive value of US wheat was confirmed again by another good weekly export sales number. At 563kt it beat the highest estimate from the trade made prior to the release of the report. This also takes US cumulative sales to 19.059mt for the 24/25 crop. C.America and Asia continue to be the major importers of US wheat.

International cash values were generally a little lower from the majors, maybe mixed would be a better term. Black Sea values varied from AUD$2.00 higher than yesterdays conversions to a dollar lower.

Australian wheat remains very competitive into Asian market, more than capable of buying demand against US HRWW.

China released a crop risk warning for Henan province, hot dry weather potentially limiting yields for the winter wheat crop now filling heads. Henan province produces about 30% of the Chinese winter wheat crop. According to last months USDA WASDE report total Chinese production for 2024-25 was estimated at 140.10mt (30% = 42mt). So a maybe a 10% reduction is worth mentioning. The USDA also estimate Chinese carry over stocks are 127.1mt, that is 48.75% of the entire world wheat carry over stock estimate. A 4mt reduction in world carry out isn’t huge, but consider we may see further reductions to Australian production due to severe drought across western Victoria and S.Aust. Include a possible reduction in Russia and Ukraine, yield losses in northern Europe from dry weather. If we were to peel say 10mt of world carry out and make it closer to 250mt it’d be nice, but it would still see the world stocks to use ratio at +30%. Don’t get me wrong, it’s a good start, and should stop any further decline in price due to supply if not kick the market some.

The AUD continued to weaken as the US FED poured cold water on a rate reduction. We’ll likely we’ll see an RBA reduce rates on May 20th according to NAB.

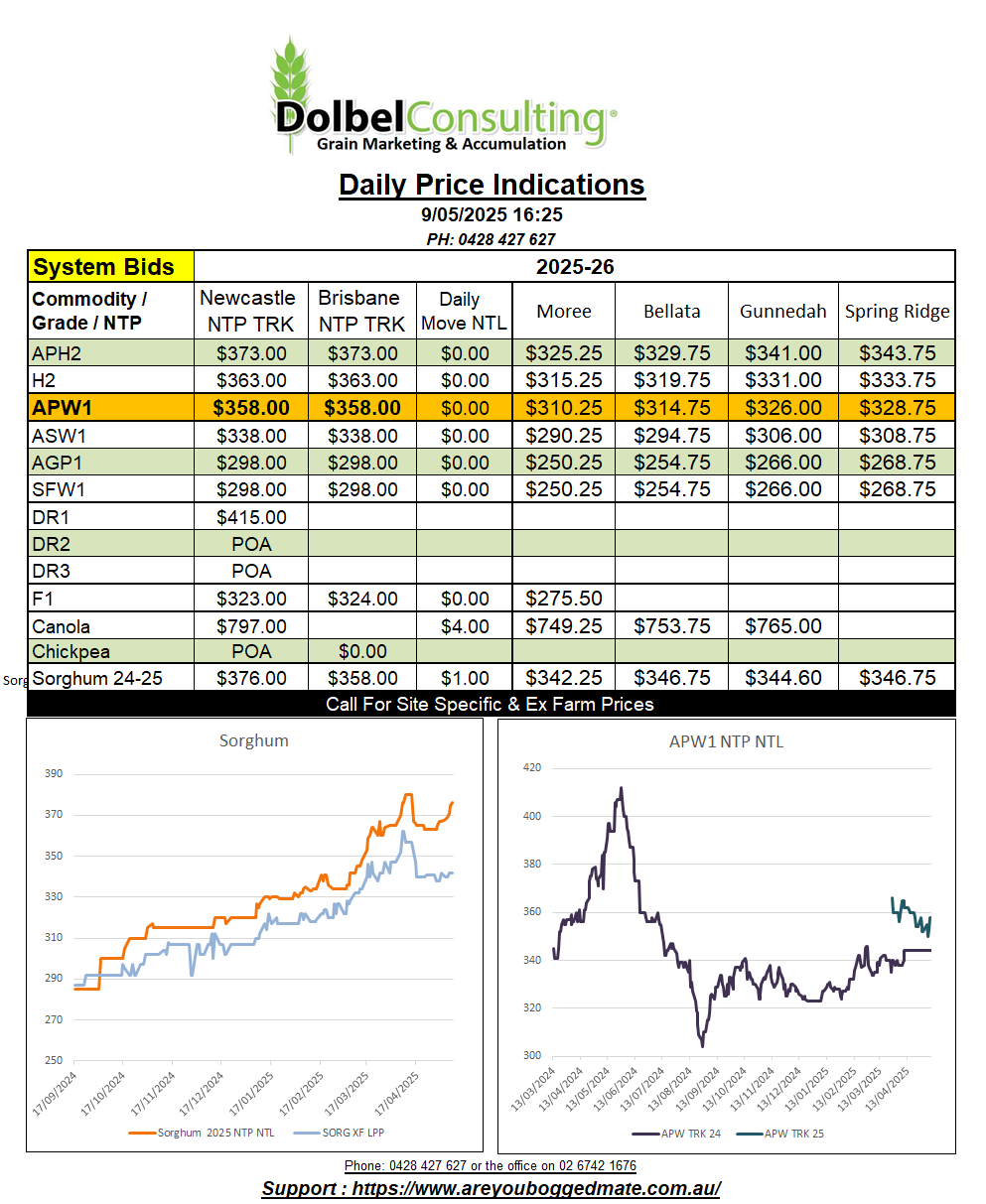

Sorghum values enjoyed the weaker AUD/USD conversion yesterday. The trade more ready to meet the offer in the afternoon. It’s not all plain sailing though. I’m seeing a big difference between the smaller trader bids and the major traders that have bulk export sales already on.

The smaller traders continue to tell me they can not do business into the export market using current major trader bids as an accumulation price. This continues to confirm that the major exporters are continuing to accumulate for export sales made months ago, not anytime in the last month of so. The only smaller traders left in the current market are those short to the majors from sales they made some months ago.

Sorghum was bid at $387 delivered Newcastle port by road. There was not significant volume on the offer side to test the resilience of the bid, but one gets the feeling offers around $388 – $400 may have played. Business on the track was conducted at $377 NTP NTL equivalent. This would give a producer delivering to Graincorp Premer a site price bid of $345. Grower offers on the track vary from $377 NTP NTL, to $392 NTP Newcastle equivalent. One gets the feeling that without some major help from currency the later offers may struggle, especially if sellers miss the current export accumulation program.

Which brings us to the stem report for Graincorp and NAT, and guess what, we now see 95kt on the Carrington stem and 119kt on the NAT stem. Unconfirmed estimates for both ports now stand closer to 180kt. This would take Newcastle port bulk export shipments towards 394kt if realised, a little above previous estimates. If the later estimates are correct and we don’t see port switching take place. Brisbane is bid $15 – $20 under Newcastle now. We should see continued support at these price levels, if the trade continue to price accumulation as it has been. That’s a big if.