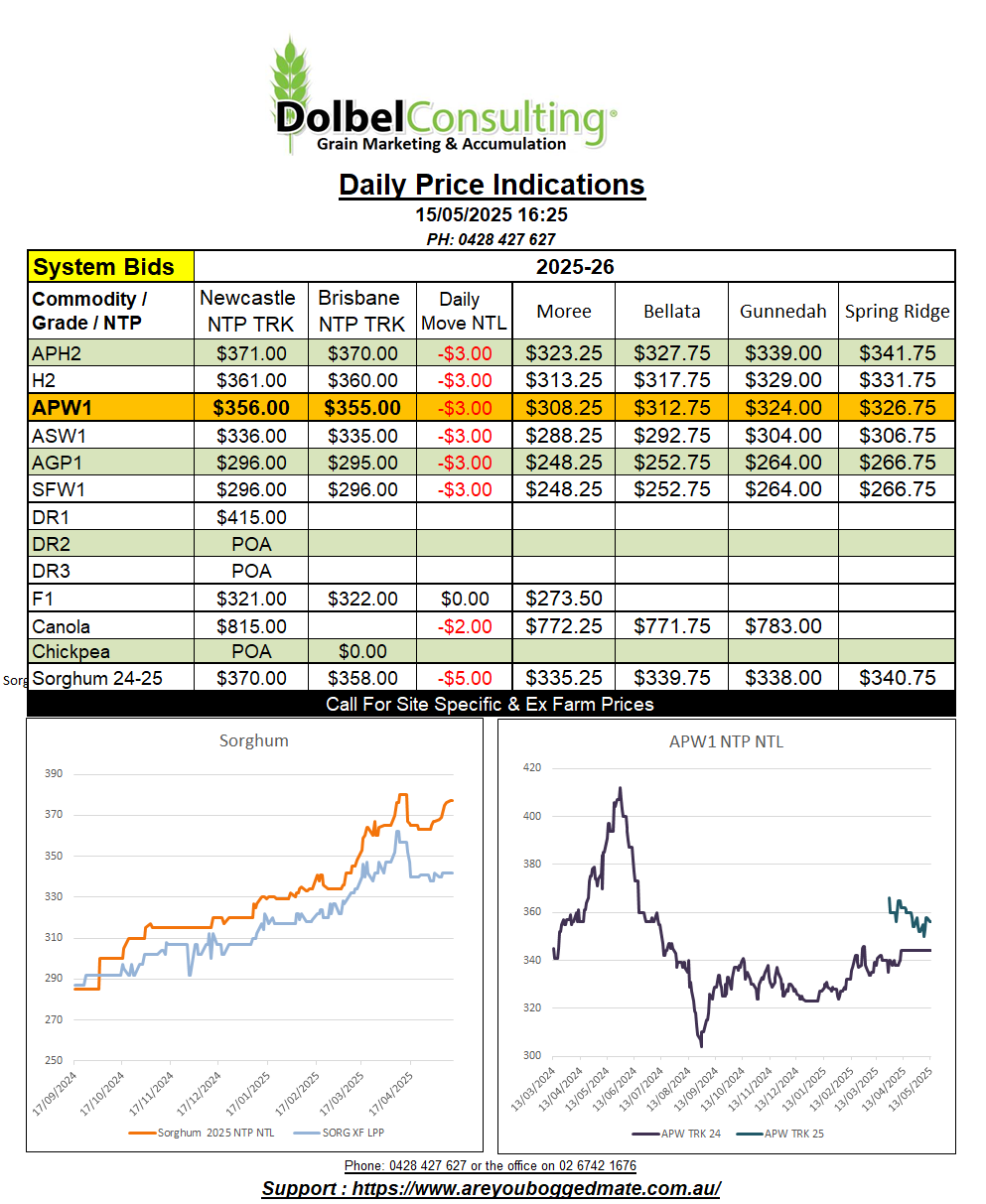

15/5/25 Prices

With US internal wheat values as low as they are we are starting to see a few more punters backing higher demand for wheat in feed rations unless corn values in the US fall further.

The major importers are also taking up US wheat. US export sales and loadings are beating, or constantly coming in towards the higher end of the trade estimates prior to the weekly report release.

So there are two things at play. Cheap wheat, and plenty of it, and a narrow corn / wheat spread. The July futures contract at Chicago this morning shows a spread of 79c/bu to SRWW and 78C/bu to HRWW. Yes that’s a premium for SRWW over HRWW. That’s like being bid less for H2 than APW, not common but can happen. This would tell most feed consumers that throwing some higher protein wheat in the mix is not a bad option.

The second thing is export projections, and will the constant beating of estimated sales eventually mean the USDA have to increase international and domestic demand for HRWW, thus reducing 2024-25 ending stocks, potentially pushing HRWW premiums back to a more traditional level. Some are of this view, while others think this unlikely. Suggesting a further reduction in corn values (feed grains) is more likely.

The outlook for the Russian wheat crop is improving, the 7 day forecast shows some good falls are possible across the central and western region and also along the Volga Valley. Recent cold weather saw some frosts towards the far SW but generally the area impacted was small. Some drier weather is also expected across the Russian spring wheat region, this isn’t a bad thing as conditions have been wetter than average there for a month or two.

Europe can only look east in envy, the 7 day forecast for northern France, Germany and west Poland remains very dry. France has reduced their April soft wheat area estimate to 4.6mha, still +9.1% higher than 2024. French rapeseed area is projected at 1.3mha, -2.3% on last year.