16/5/25 Prices

Canola and rapeseed got caught up in the sell off in Chicago soybeans last night.

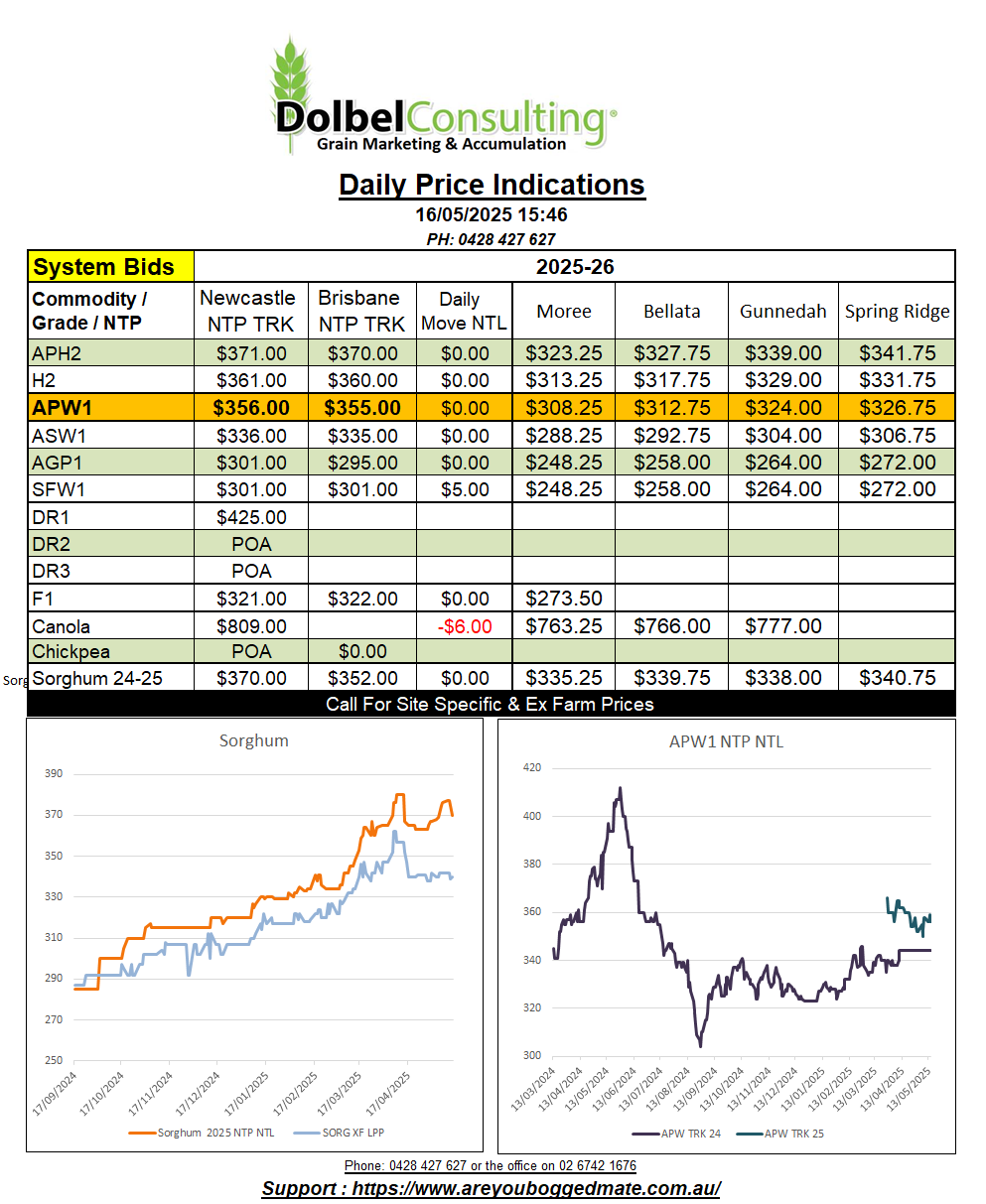

Winnipeg canola was hit the hardest, shedding C$27.04 for nearby pickup ex farm SE Saskatchewan according to price reporting platform PDQ. Canadian new crop canola was also hit, a Sept lift shedding C$23.60 / tonne. There’s still a spread between old and new crop across SE Sask, prompt pickup bid on average C$657.12 and the Sept lift bid C$605.08, a spread of C$52.04 / tonne. This is interesting as locally we see the old crop bid at AUD$805, and the new crop bid at AUD$832 delivered Newcastle crusher.

Across the Atlantic Paris rapeseed futures were back €5.25 in the nearby August slot. Feb 26 was back €4.75, closing at €484.50 / tonne. World cash values for rapeseed and canola were also volatile, some locations much more so than others. FOB Rouen is valued at roughly US$550. Taking the AUD move into account that is actually a slight day to day improvement from yesterdays conversion. The June palm oil contract was back 17MYR/t, roughly AUD$6.20 / tonne, the least bearish of the vege oils. Chicago soybeans were back 26.5c/bu (AUD$15.20/t) nearby.

According to one reporting agency the sell off was attributed to concerns to changes in the US biofuels policy. The fact that the funds had pushed beans to a 10 month high against a huge S.American crop and failing trade talks with China should probably be considered too, but to counter that we do see US bean exports above last years pace. Argentina raised it’s soybean production estimate now harvest is winding up, and the prospect of some half decent rain across the Canadian canola regions also weighed on the market.

US weekly wheat export sales at 430kt came in towards the higher end of expectations. I’m surprised it wasn’t more considering how cheap the US product is at present. S.Arabia issued a tender for 650kt of milling wheat, nice to see. To counter that Argentina expects to sow their biggest wheat crop in 15 years.