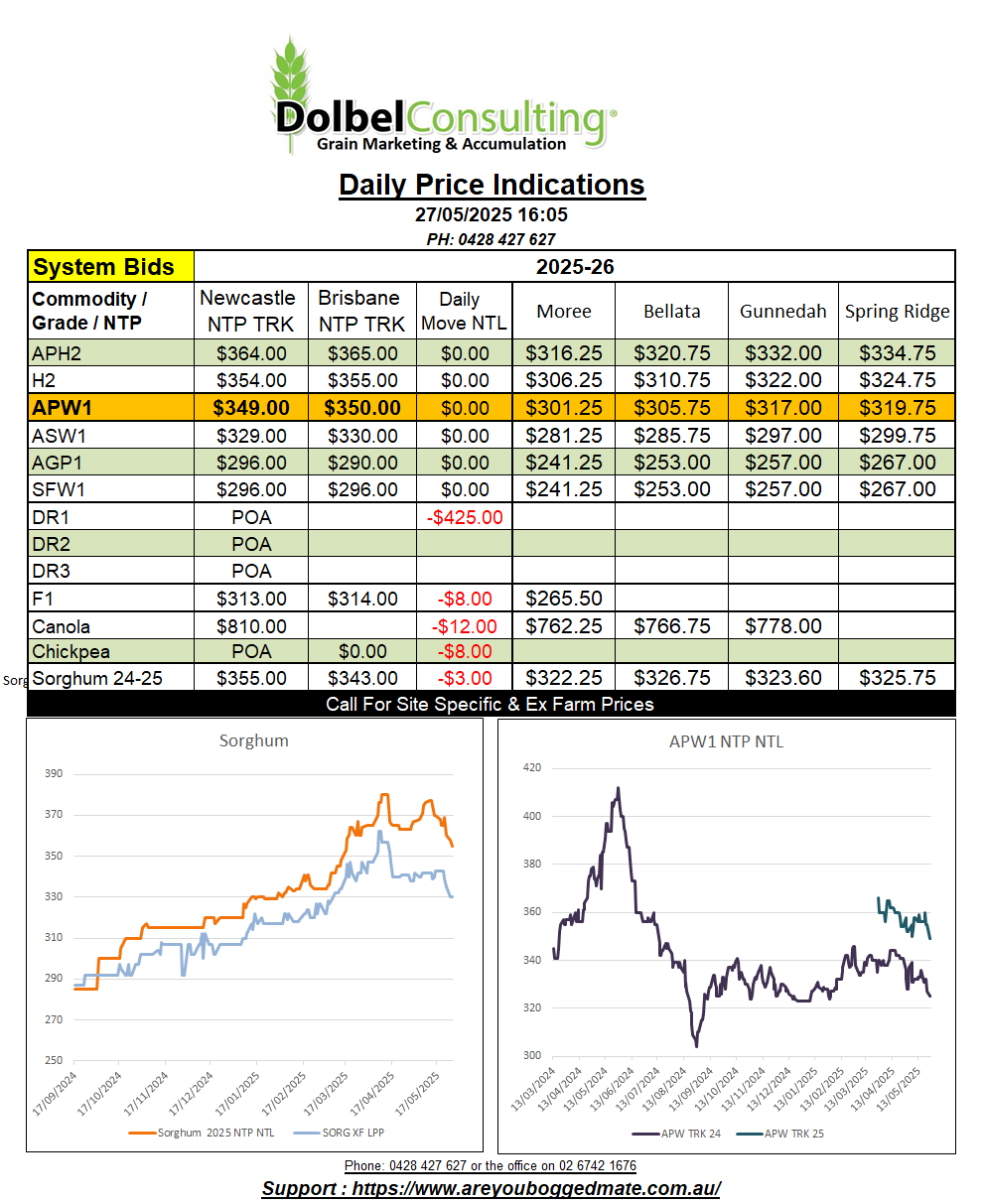

27/5/25 Prices

The international markets remains focused on dry conditions across the north of France, hot dry conditions in the major winter wheat producing region of China, recent flooding and water logged fields in Argentina, and drought conditions across SE Australia.

France has seen little rain across the northern half of the country over the last 7 days. Temperatures there remain mild, hardly breaking into the 20’s yet. The seven day forecast for much of France remains dry. This has most analyst expecting to see a decline in the Good / Excellent rating of the French crop from 71%, in both this weeks and next weeks crop condition report. Germany is expected to see some good falls over the next 7 days after a mixed spring.

The forecast for the winter wheat region of China remains dry after a few light showers moved across the region last week, with 5-10mm falling across Henan. Rainfall across the southern half of China remains high and is expected to become very wet this week with 75-100mm forecast for the central and southern districts. Temperatures across the winter wheat region of north central and northern China have cooled a little and are expected to remain average for the week ahead. We should start to get some harvest results out of China soon, late May / June is their peak harvest period for winter wheat. Wheat imports to China have slowed this year, something to watch as we move through Q3 – 4 2025.

Flooding across Argentina has resulted in the BA exchange reducing soybean production estimates. Some punters believe that wheat sown area may also be reduced in coming months but as is the case here in S.Australia, it is also early days in sowing for Argentina. The winter sowing window is open for at least another 4 – 6 weeks for many producers in the flooded regions of BA. Argentina has produced winter wheat on very little subsoil moisture over the last few years. This rainfall event may be just what they needed to recharge some of the drier fields.

International cash and futures markets showed little change overnight. Paris milling wheat futures were +/- €0.25 / tonne in the August > Jun 2026 contracts. Paris rapeseed futures were also flat to €0.25 / tonne lower. The AUD is steady to lower, shedding just 0.12% overnight and remaining in the high 64s.