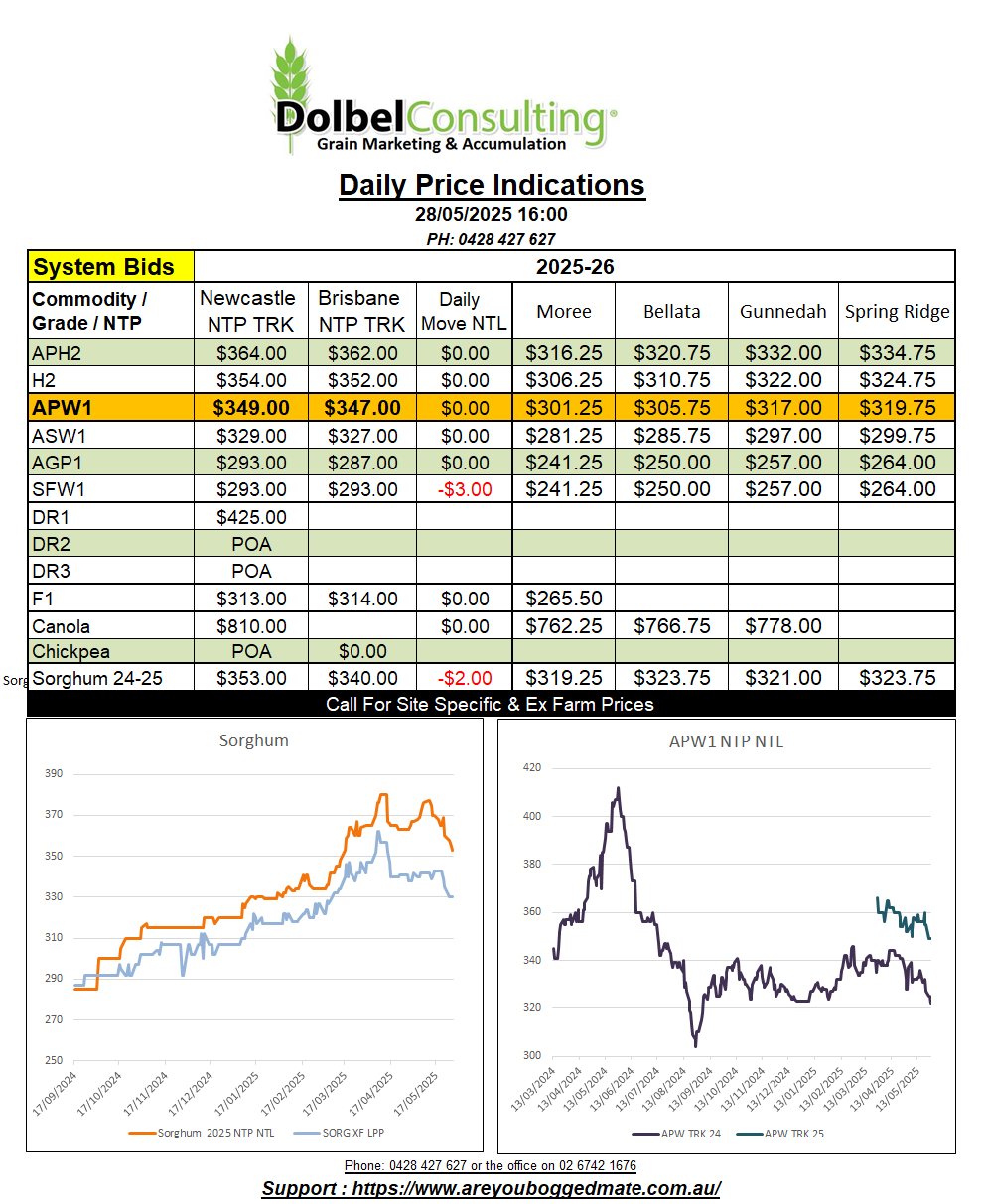

28/5/25 Prices

The USDA weekly crop progress report was out after the close of the day session in the US last night. Corn sowing continues to progress well in spite of some heavy rain in some locations. Corn is now estimated at 87% sown versus 85% for 5 year average.

The big question getting thrown around the corn market is, can the US achieve the average yield estimate the USDA have come up with, 11.36t/ha is one hell of an average yield. The USDA rated the corn crop at 68% Good / Excellent, their first quality rating for the 2025-26 US corn crop, and bang on the 10 year average quality rating.

Soybean sowing was progressing well at 76% sown versus the 5 year average of 68%. Cotton was estimated at 52% sown. Sorghum was estimated at 39% sown, 81% sown in Texas and 21% sown in Kansas.

75% of the US winter wheat is now in head, Kansas 68%. A little ahead of the five year average but behind last years harder finish. The crop condition rating for the US winter wheat crop fell from 44/8 – 52% G/E last week, to 43/7-50% this week. The Kansas crop slipping 1pt to 48% G/E. Spring wheat sowing is nearing completion, progressing to 87% sown, up 5pts on last week. Wet conditions across N.Dakota and Montana delaying the last few acres but the average pace is still above the 5 year average, so all good.

Maybe a little too good. The wheat futures and cash market for all 4 main grades of US wheat fell away overnight. Cash values out of the US Pacific Northwest tracked futures markets lower. The weaker AUD has helped counter some of the downside potential in the conversion but the numbers are still reflecting a plausible loss in the conversion between AUD$3.50 and AUD$6.00 per tonne, HRWW being hit the hardest out of the PNW. HRWW is sustaining the US$11.00 discount to Aussie H2 type wheat into the N.Asian markets. Yes white wheat should extract a premium to red wheat and it will into most markets, but the pressure remains. Aussie H2 is discounted to US white wheat into the Asian markets by roughly AUD$10.00.