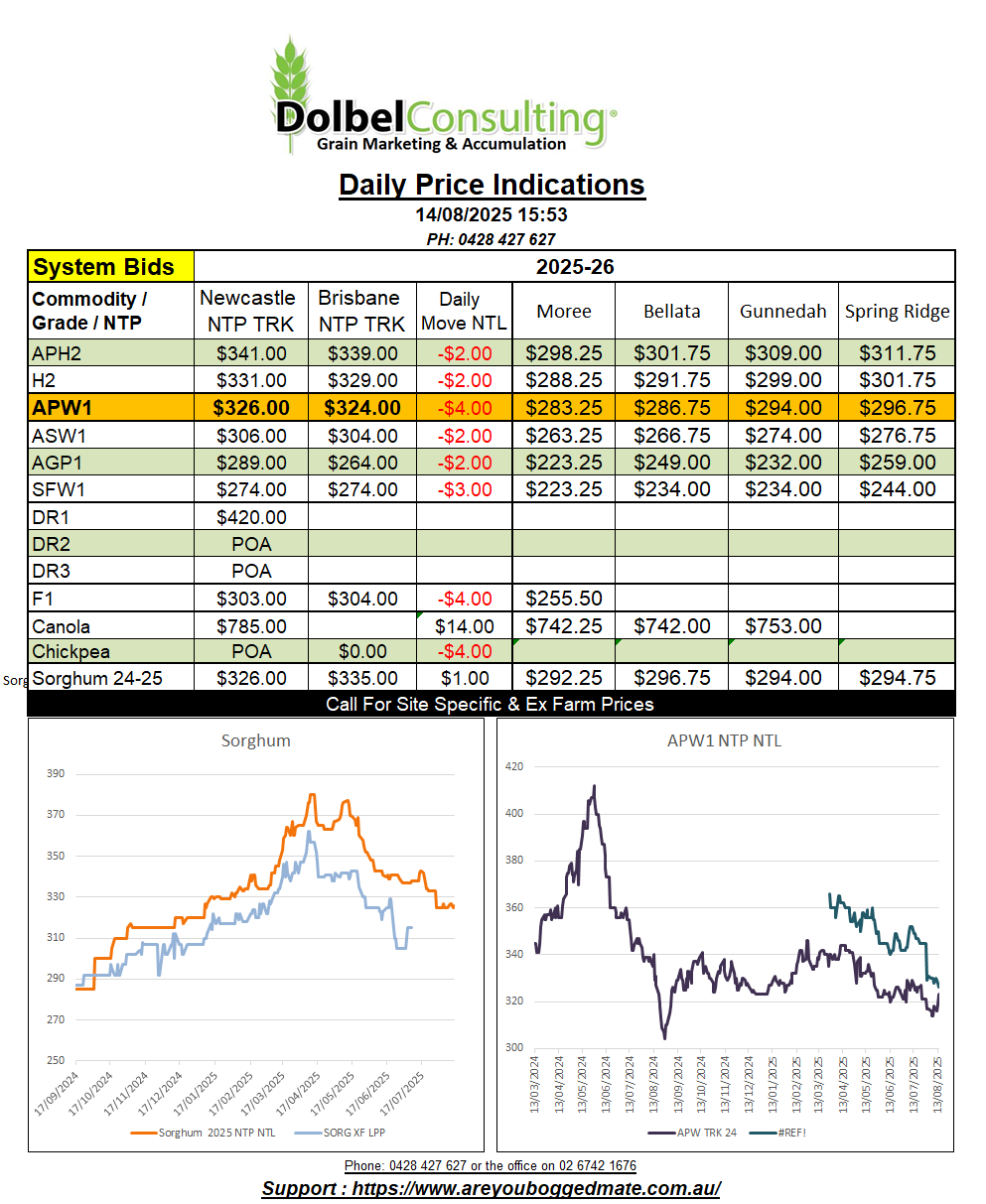

14/8/25 Prices

The international market, mainly the US market, is still digesting the vast meal that was the August USDA WASDE report. Some may have suffered indigestion from this report others may still be in the loo, given size of the meal. A market mover it was, but are these moves both unexpected and more importantly justified, that’s what the next couple of session / weeks will determine. Already we’ve seen some adjustments to corn and SRWW futures at Chicago.

Canola futures at Winnipeg were crushed on Tuesday night, failing to take any notice of the sharply higher Chicago soybean market. Last night saw Winnipeg canola take back some of the big losses and close higher, as did Paris rapeseed futures.

The news that China was smacking a 75.8% import duty on Canadian canola was the main focus at Winnipeg. Canada’s relationship with China is low, probably not as low as the US relationship at present, but to expect that China was going to do anything but limit Canadian canola imports shouldn’t have came as a huge surprise to anyone. The knee jerk reaction in the futures market does tend to highlight the impact certain types of traders have on futures markets these days. From a fundamental perspective, if Australia can meet import demand into China that may have otherwise been filled by Canadian canola than this is simply going to result in a reshuffling on the S&D sheet, not a whole new set of numbers. It may, to the skeptical among us, bring into the spot light why we need to have the ISCC “premium” in place when it’s only applicable to the EU market.

Last night Winnipeg canola bounced, time will tell if this is a dead cat bounce or if the market will make a recovery and close at or above similar values as it was prior to the announcement of the Chinese duties. Or if indeed Canadian canola “needs” to be even cheaper to buy demand over Aussie canola into the EU or others. Prior to the fall Canadian canola was already cheaper, hence more skepticism. The million dollar question every farmer asks, “should I forward contract some tonnage”. Current values are good, better than what Canadian values are, the big question is “what is China willing to pay” for seed, oil or meal ?

Contract execution and clean up of both sorghum and any remaining winter crops seems to be the program at the moment. There’s not a lot of incentive to lock in new crop grains at current values, remember the marketing year is 6 months either side of harvest, not 6 days either side of harvest. It may be one of those years that you need to be a little patient.

It appears the trade is happy to reflect the lower values currently being set by the US leading up to our harvest. This isn’t a guarantee that prices will rally as buyers become more active in Oct / Nov. Given current basis levels you could even be excused for thinking the opposite may happen (wouldn’t be the first time). Basis to US futures has been stronger than one might expect given the current production outlook in the north. This is allowing the trade to currently sell high basis, I’m not sure how good a hedge US futures are these days, but a hedge is a hedge.

This does need a degree of confirmation though, playing the devils advocate we need to ask two things. Is winter crop area in the north at a level where domestic consumers and exporters should be comfortable, and what is the potential yields of these fields.

Driving around the plains it’s getting easier to tell the amount of canola that has been sown. To be honest it looks to be a slightly higher than average area but not huge. BUT the amount of green fields, wheat or barley, doesn’t look to be at all near average but much lower than average.

It’s important that I get your sown area and commodity split data this year. The reason is two fold, firstly to confirm that area estimates are what I think they are. Secondly that I keep market reports relevant. If no one has sown durum than I’m wasting your time and my time reporting on it.