15/8/25 Prices

The weaker AUD is countering most of the negativity in world cash and futures markets for grains last night. The AUD is weaker against the US dollar. The odds appear to be back on for a rate hike in the USA as tariffs increase the cost of goods, thus the US continues to see, and is expected to see further inflation. I’m starting to think Trump was the only one that didn’t see this coming, well that’s what he’s telling everyone anyway. The best way to erode government debt is to increase inflation, decreasing the value of the debt relative to the dollars true worth.

The reality is, in theory at least, reducing rates here and increasing rates in the US should continue to weaken the AUD. Looking at how the US continues to reduce values of export grains we really need to see the AUD continue to weaken. Not good for those looking to buy / sell a new tractor or header, but at least it helps the export value in the short term. We do have the whole AUD trade as a Yuan proxy to deal with though.

The lower dollar saw most conversions for international grains that would have been slightly weaker convert to slightly firmer today. For instance white wheat out of the US Pacific Northwest is up AUD$4.43/t compared to yesterdays conversion. US HRWW fell away in US dollars per tonne, but compared to yesterdays conversion into an AUD port equivalent price, this mornings conversion is up AUD$1.43 / tonne. The weaker AUD buffered EU, Canadian, Russian, Ukraine and Argentine wheat price conversions.

The combination of the weaker AUD and a rally in the cash price for chickpeas at the Delhi mandi helped claw back some of the losses seen there during the week. Delhi chickpeas moved 57Rs/Q higher. Converting the closing price of 6307Rs/Q to AUD/t this morning indicates an improvement of AUD$15.14 / tonne over yesterdays conversion. This market remains volatile at present, but with poor production in Pakistan, and good demand from other importers, chickpeas look unlikely to collapse in the short term. Canadian production is up year on year, but is still expected to be below 320kt.

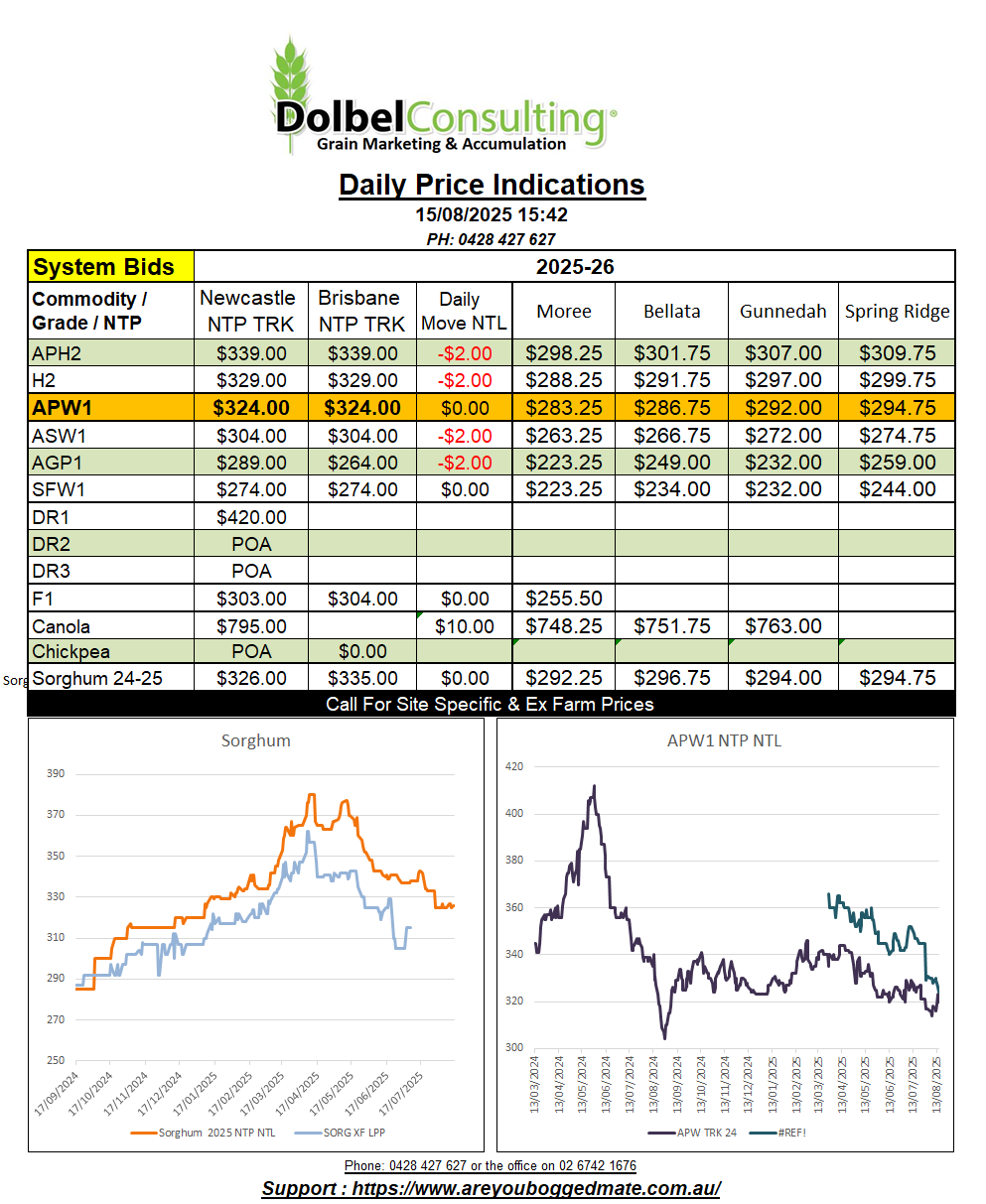

New crop wheat and barley numbers slipped away a little yesterday. Canola broke the trend, recovering some of the previous sessions losses. Canola was bid $830 delivered Newcastle crush for Q1 2026 delivery, so roughly $790 XF LPP +/- oil P&Ds. The ISCC non compliance discount, or sign up premium as the trade like to call it, will apply again in 2025-26. It’s a bit like a new tax, once you get it you will never get rid of it.

The world oilseeds market is complex, different levels of substitution exists between different oil seeds, some more elastic than other. Oil and meals come from the likes of sunflower, olive, fish, peanut, cottonseed, soybean, canola, palm or copra, this all inter-relates to the oil and meal markets.

For instance Brazil supply about 80% of Indonesia’s soy meal demand but only 3% of their soybean demand. The US sell more actual soybeans to Indonesia than Brazil do, but Brazil has the lions share of meal market there over both Argentina and the USA. This could be due to quality, US beans are usually better quality than Brazilian beans. Whole soybeans are generally used in the production of human foods like tempeh and tofu. Meal is stock feed.

The S&D tables for the each oil seed alone tells one story but something like a 175mt soybean crop in Brazil, can also weigh on something like EU rapeseed values.

Global rapeseed / canola production in 2025-26 is estimated at 89.58mt (85.65mt LY) this is very close to the 2022-23-24 production levels. Total oil seed production is closer to 690.11mt, 8.35mt higher than last year. World ending stocks for rapeseed is expected to be 9.87mt (9.75mt LY). Crush rate is expected to be high, around 85.11mt, the highest crush number in 5 years, resulting in the highest oil and meal production in 5 years.