27/8/25 Prices

The USDA weekly US crop progress report was out yesterday. Corn is now 83% dough stage and 7% mature on average. The G/E condition rating was stable at 51/20 = 71% versus last week at 50/21=71%. 4% of the US soybean crop is dropping leaves and the rating was up 1pt in the G/E to 54/15 = 69% G/E. Cotton was rated at 54% G/E and 20% boll open.

Sorghum was 44% coloured and 23% mature, the condition rating was 47/16 – 63% G/E, the same as last week.

The USDA pegged 53% of the spring wheat crop in the bin, just 1pt behind the 5 year average harvest pace. The spring wheat condition rating was estimated at 43/6=49% G/E versus last week at 45/5=50% G/E. Montana continues to see lower than average condition ratings with just 1% of their crop rated as good and a massive 49% of their spring wheat rated as poor to very poor.

This rating is reflected north of the Montana / Canadian border where much of the SW Saskatchewan and SE Alberta spring sown wheat and barley not only suffered from a dry start and mid season, but then ran into late season rain encouraging sprouting and poor test weight in what crop survived the early season set back.

Ironically both Canadian and French durum values have fallen away this week as harvest picks up across the Prairies. Yields have been a little better than expected in some fields. The mid to late season rain filling grain better than expected but then sprouting many fields. Yields across SE Alberta and SW Sask are starting to come in at 20-30bu/ac, 1.7t/ha, not great but better than the 10bu crops many were expecting.

In last nights ND Wheat update N.Dakota durum harvest was pegged at 30% complete, Montana at 66% complete. N.Dakota durum was rated at 83% G/E, an extreme contrast to the Montana durum crop, now rated at 0% G/E and 57% Poor to Very Poor. Markets are cruel, durum sometimes one of the cruelest (let’s not mention pulses) the average XF price out of SE Sask for 1CWAD13 slipped CAD$7.43/t for Dec lift yesterday, harvest pressure the key.

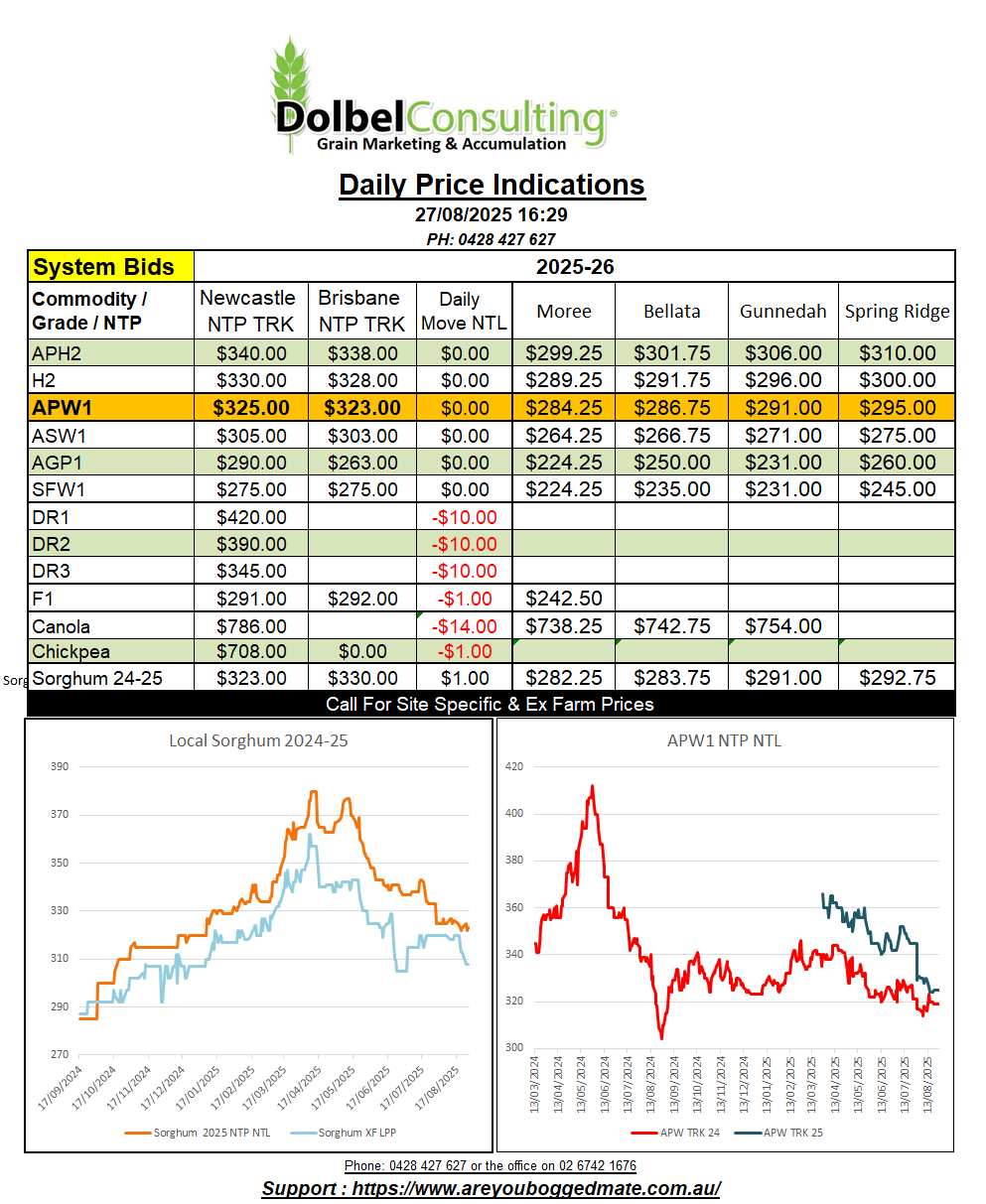

Local new crop sorghum values fell away a little yesterday. Producer selling on the Downs and seller interest across the LPP spooking the buyer a little. Generally grower offers to sell remain above $300 – $305 delivered Werris Creek silo, a number very close to trading on Monday.

Weakness in new crop sorghum correlates with the higher AUD and not so much with international values. Overnight international sorghum and cash corn was generally flat to lower. The bundle of corn and sorghum FOB / CiF values I’m using as a price index slipped roughly AUD$1.45/t, possibly indicating that we may be in for some softer new crop bids for sorghum again today.

Longer term it will depend on the way China buys. Demand into China is expected to be roughly the same as last year. The main difference this year being that the Chinese are starting their buying with the US / China tariffs already in place. This may influence early business more our way. As with last year I think the Chinese market will be more about volume than price locally but we should expect to see a good premium above US values.

Currently US sorghum is valued at roughly US$239 CiF China. Working that values back to an Aussie port equivalent, after adding the current import tariff to the US value, we come up with a price something close to AUD$330 +/- at the port, or $300ish XF LPP. Yesterday we saw Brisbane port bid at $345 for new crop sorghum. Given the US conversion one could assume this is fair value and may attract further grower selling up there. The Shenzhen index is roughly US$30.00 above this number. Potentially this is giving us a cap and floor to work off for local values, $300 to $347.

Over the last ten years the average range that the local track sorghum contract has traded is roughly AUD$80 over the life of the contract, using the monthly average throughout Sept > August. If we take a mid way point between $300 & $347, say $324, a traditional cap / floor may be closer to $364 – $284 XFLPP.