29/8/25 Prices

Chicago soft red winter wheat futures took back all of the previous sessions losses last night. Week on week we see the Chicago SRWW contract down just 0.75c/bu (less than AUD50c/t at the spot rate) compared to last Thursday.

Our biggest problem here is the AUD is 1 US cent firmer, that’s roughly equivalent to -AUD$4.60 / tonne. So combined, the conversion is AUD$5.00 lower week on week. So to see AUD$2.00 off the new crop bid probably isn’t as bad as it looks, the fall I mean, the actual price is still rubbish and offers very little incentive to grow wheat from a gross margin perspective.

Looking around the world at some of the major exporters, converting their FOB price to a CnF Asian customer and then converting that price back to a local equivalent we see most conversions for export values for milling wheat have fallen. French and US wheat has lead the march lower, back between AUD$7.00 and AUD$12.00 per tonne since last Thursday. Black Sea conversions have fallen closer to AUD$1.50 to AUD$3.50/t.

The competition for Aussie wheat is coming from the US Pacific Northwest, unless you work it into China who has applied a 15% tariff on US wheat imports. Indonesian tariffs on US wheat are set at “near zero” after Indonesia negotiated with the US to reduce US import tariffs from 32% to 19%. Australian feed and milling wheat are tariff free into Indonesia, China, Vietnam, Bangladesh and Japan, some importers do have a quota system though.

Year on year imports of wheat into China, Indonesia, Vietnam, Bangladesh and Japan are expected to increase by roughly 3.4mt year on year. Volume is still not expected to reach the highs of 2023-24, around 41.63mt, but at 35.75mt for these 5 importers, they do make up 17% of total world imports. The Middle East and N.Africa remain the largest wheat import regions, combined accounting for 25% of world wheat imports, a good thing Russia and Europe are on their doorstep. Russian milling wheat works into Egypt at roughly US$12.00 lower than French wheat would. This tends to indicate that there may be some further downside in French values yet. US wheat remains cheaper than Aussie wheat into the Indonesian market, so less risk of downside there / here.

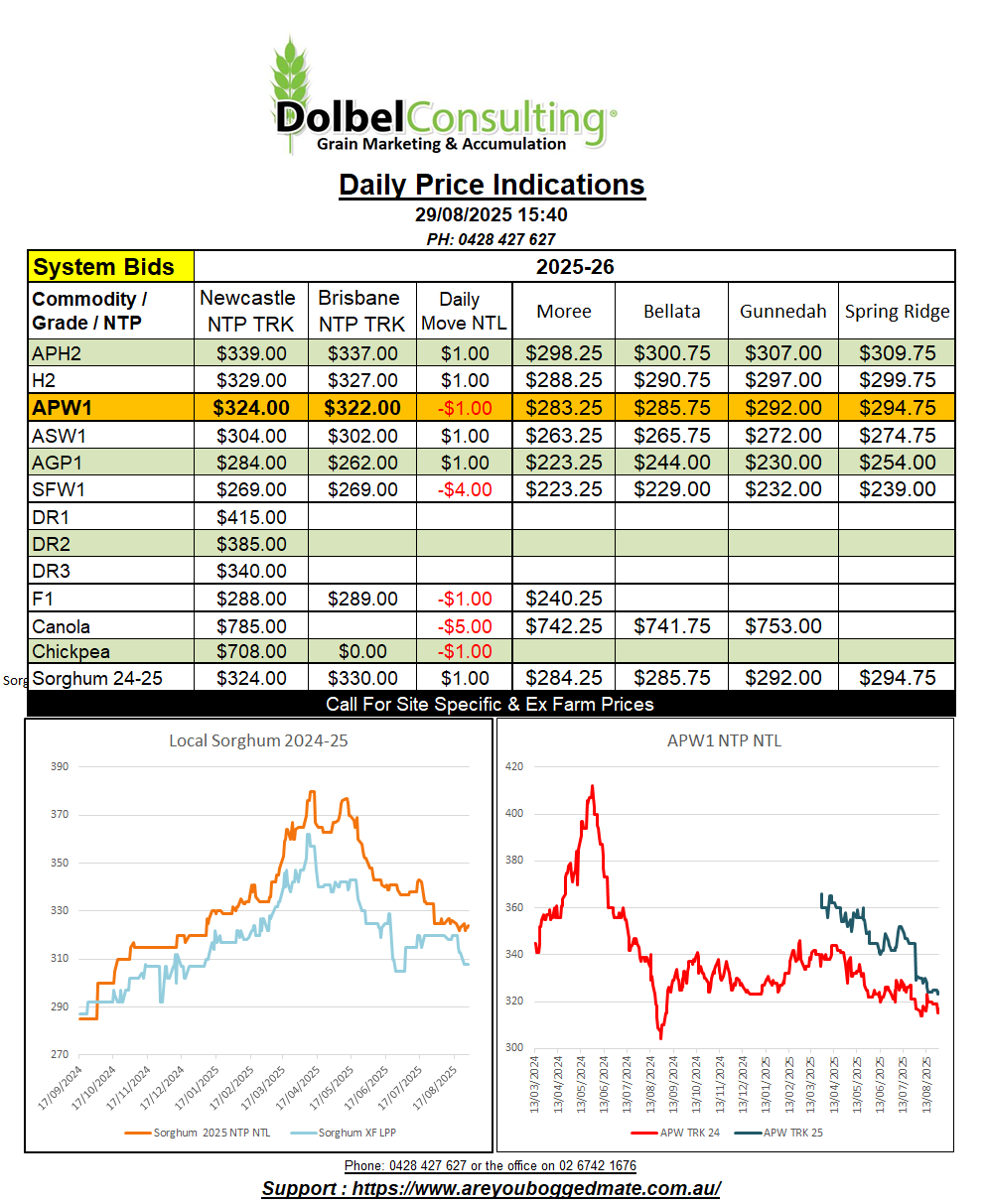

New crop sorghum bids on the track remained unchanged after slipping $5.00 on Wednesday. Some buyers did continue to reduce their bids though, both on the track and delivered port Brisbane or Downs packer. New crop Downs is bid $323 delivered, old crop is bid at $351 delivered Downs.

Overnight international sorghum values were generally a little softer, following the previous session for Chicago corn futures lower. The weaker USD helped corn futures in the US recover a little last night, but also hurt the conversion of international values to AUD this morning. On average the international price of sorghum was back around AUD$2.00 to AUD$3.00 when compared to yesterdays conversion. When including various international corn values into the international feed grain market to determine a general average market move, the lift in corn values overnight decreases that change in the average conversion from yesterday’s market to roughly -AUD$0.87/t.

Last year when new crop sorghum values were introduced mid September at $285 NTP Newcastle we had 65.71c currency and Chicago corn futures at 412.5c/bu. Currently we have currency at 65.07c, Chicago corn at 385.5c/bu and new crop cash bid at $325 NTP Newcastle, a $40 premium to mid September last year. I need to mention that last year the Newcastle track price continued to rally right through to the peak in mid May. Not a year to forward contract a bundle of sorghum.

Currently we still have the Chinese / US sorghum tariff at 10%. We have May 2026 Chicago corn futures at 437.75c/bu, lets just assume 65c May26 currency. To grab the same basis to Chicago corn as what we have currently cash bid should be closer to $340 NTP Newcastle, mind you current basis is ok. US sorghum is valued at US$236 CnF China, plus tariff, say US$260. That rolls back to a NTP Newcastle bid of something close to AUD$327, bang on current bids.