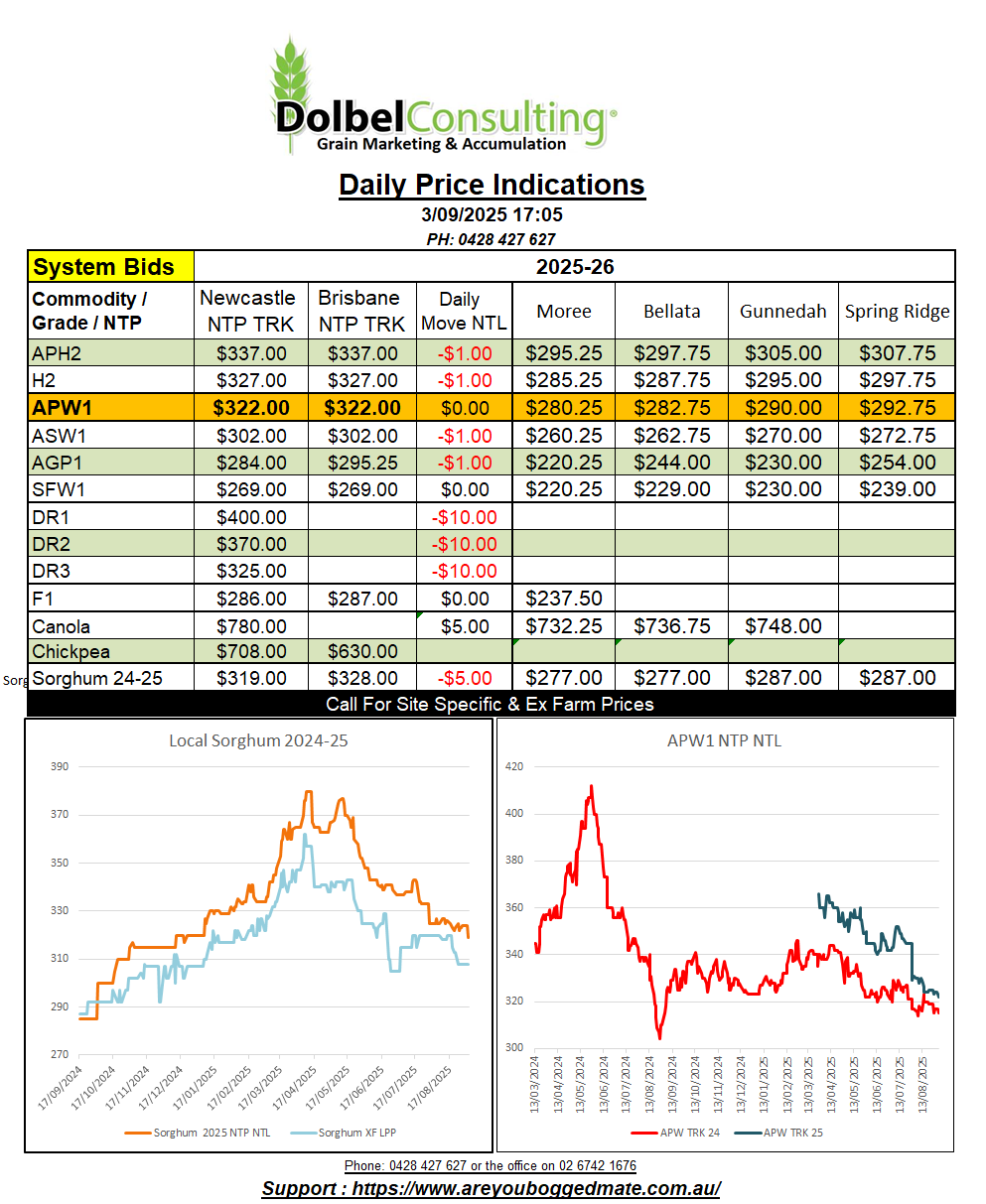

3/9/25 Prices

The USDA weekly crop progress report was out after the US futures market closed last night. Just skimming through it we see corn there is now 58% dented, 15% mature and has a G/E condition rating of 50/19=69%, compared to last weeks G/E rating of 51/21=72%. This may help to continued to close the gap between corn and wheat futures. About 94% of the US soybean crop is now setting pods, 11% is dropping leaves and the bean crop is rated at 51/14=65% G/E, a decline of 4pts week on week. 58% of the US sorghum crop is colouring, 28% is mature. 67% of the Texas crop is now in the bin and around 12% of the Kansas crop is mature. The G/E rating for US sorghum improved 1pt this week to 48/16=64%.

Spring wheat is 72% harvested. N.Dakota is catching up to the other states, but is still behind at 62% harvested. There’s nothing in this report to drive wheat higher. We may see some spillover support from corn but that’s not something that we’ve seen materialise often during this US wheat harvest.

Looking at the weather from around the rest of the world we see flooding in Pakistan Punjab. This is having an impact on their summer crop program in low lying areas and in some cases stored winter crops.

Argentina continues to see significant winter rainfall, much of the wheat districts seeing 150-600% of average rainfall over the last 30 days. 30 days totals across the central wheat regions of Cordoba, Santa Fe and Buenos Aires are above 100-150mm. A serious storm produced 150mm to 300mm of rain within 2 hours across southern Santa Fe and neighbouring states, leaving many local roads and power delivery infrastructure destroyed. Damage may have been much worse if it wasn’t for recently improved flood mitigation work on channels and rivers. The flooding follows reports of frost damage to crops across SE Cordoba and Santa Fe. Argentina had already had a wet winter, this storm potentially sealing the fate of some low lying winter crops. Rosario Board of Trade state that damage assessment will be days away as access is now poor. Corn sowing may be delayed as fields are re-worked in preparation for planting.

Looking at basis. After sending out that email about Rabo Bank and the way they were comparing international FOB wheat values yesterday I got into a conversation or two in regards to basis.

Simply put, a swap is an over the counter product where the bank plays an intermediary roll between you the buyer or seller of the swap, and the futures market on which the underlying futures contract is traded.

At some time in the long distant past, the bank had a set fee for this service, you knew that the swap value, buy or sell side, was going to reflect the futures market on the day converted to AUD / tonne, less a small fee.

These days it’s a little different, swap providers are now theoretically basis traders too. Basis traders in a market they can’t loose in. The gap between the banks bid to buy the swap, and the offer to sell the swap, can change. This spread, lets call it their basis, changes, sometimes daily, sometimes not so often. Just be aware that it’s not as simple as converting a futures contract to AUD per tonne when dealing with swaps.

This is not exactly the same as a physical grain traders basis position where they buy physical, sell futures and then buy futures back when the sell the physical, not necessarily in that order but that’s the process. The basis being the difference between the cash price and the converted futures price to the relative point of delivery or execution. In theory it is possible to make not only physical profit, buying grain lower than where it’s sold, but also basis profit. The same process can be done with freight as another leg of the “hedging” program.

This brings me to the attached chart outlining basis movement between August and December last year. A year of good supply.