4/9/25 Prices

The September USDA World Ag Supply and Demand report is due out on the 12th US time, Friday week, so data here on Saturday morning of the 13th. The chance of increases in world wheat production is potentially high.

Yields across Canada have been a little better than expected. Private estimates out of Russia are generally all higher than the current USDA estimate, some by more than 3mt. I’m not convinced Russia is a done deal though. Weather across the spring wheat regions has been good all season, and continues to be wet, even now that the headers are coming out of the sheds. This may reduce test weight in some fields, time will tell, but the general market is factoring in a larger Russian crop than the current USDA estimate. Response could be sell the rumour / buy the fact, but lately it’s been more a “sell everything” market.

The flooding and heavy rain across Argentina as a few punters expecting to see reductions there. Like the Russian spring wheat region, the season in Argentina had been very good prior to the storms at the end of August. Some analyst are predicting that the flooding across Santa Fe and Cordoba will have more of an impact on summer crops, like corn, creating sowing delays. The winter crop window is very similar to the Australian window, thus the rain is probably creating a similar environment for wheat as what we are seeing here on the LPP at present. You be the judge of what you think that will do to yields and quality.

International cash wheat values were mixed overnight, generally lower, following US futures lower and also finding pressure from a stronger Aussie dollar. Looking at US and Canadian values out of the Pacific Northwest we see spring wheat, both US and Canadian, was hardest hit, more so than what the futures market may have suggested. In AUD per tonne the day to day conversion is down roughly AUD$6.47/t for DNS wheat out of the US and -AUD$2.05/t for Canadian 1CWRS13.5 milling wheat. Canadian durum values were also lower, back CAD$2.54/t XF SE Saskatchewan. Harvest pressure in Canada is seeing durum values there move against the trend higher in French values this week. The stronger AUD taking the cream out of both conversions today.

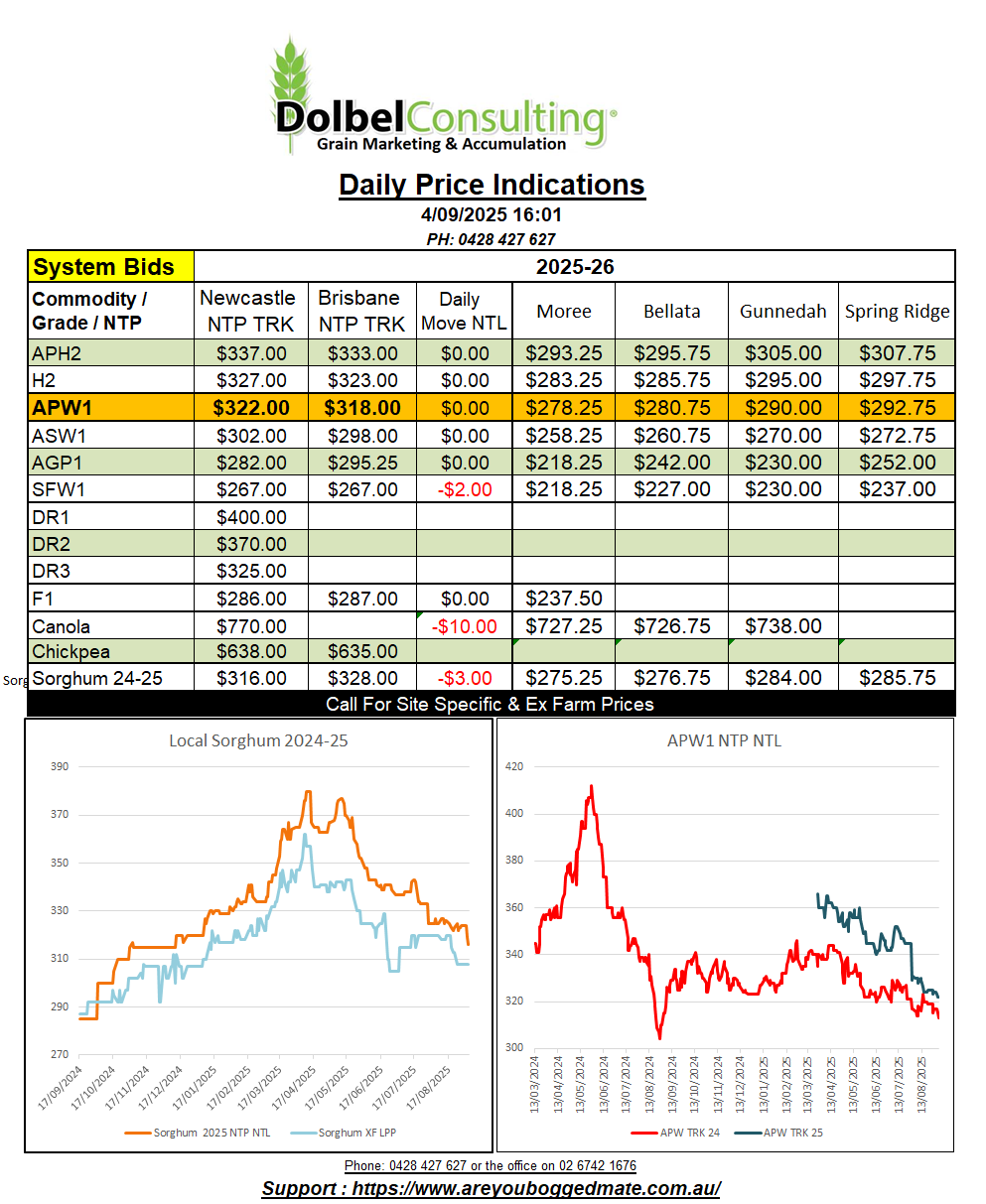

There’s a little old crop SFW1 changing hands at values equivalent to about $325 delivered LPP end user for September. The volume on the offer side isn’t huge, a few hundred tonnes here and there, but the trade are absorbing the volume easily and appeared happy to meet the offer. There is also trade demand for BAR1 either on the track or ex farm but values remain poor and volume on the sell side is non existent off the plains at current values.

The latest ABARES crop report increased Australian winter crop production, now significantly higher than the June estimates. NSW is expected to produce around 10.7mt of wheat this year, that’s a year on year decrease of 17.1% off a 5.1% smaller area. This is using a yield estimate of 2.89t/ha, which may turn out to be a little low in some places. NSW barley production is estimated at 3.15mt and NSW canola is estimated at 1.6mt.

Looking at a national wheat crop of roughly 33.7mt, does tend to indicate that ending stocks will probably increase significantly unless exports increase from the current 22.8mt estimate to at least 24mt to 25mt. Domestic demand should remain relatively static, possibly a slight increase in human consumption but not enough to counter the potential 2.2mt increase in carry out, unless exports improve. Current USDA Aussie wheat export estimate is 23mt.

Competition into the Asian market will mainly come from the USA. Recent trade negotiations have seen the US reducing import tariffs for those countries that will increase import demand from the US. At the moment that isn’t hurting milling wheat out of Australia a lot due to our wheat type, and geographical and timing advantages, but it could become an issue if we have a downgraded crop. Does this hint towards potentially hedging some wheat on the cash market. At $300 delivered Tamworth for ASW, that’s right ASW not SFW1, it doesn’t do much more than open you up for a washout if we do have a feed year.