5/9/25 Prices

European grain futures were generally lower, London feed wheat shed £1.00/tin the Jan 26 slot, Paris milling wheat was flat nearby but slipped €0.50 / tonne in the December slot, Paris corn futures were lower and Paris rapeseed also closed in the red, shedding €2.25 / tonne in the Feb 26 slot.

US futures were mixed, corn and soybeans at Chicago were up a smidge while wheat continued to shed values. HRWW has been hit particularly hard this year and continues trading at a discount to SRWW, hard to believe. Locally we generally only see wheat of lower grade priced at the same value of a higher grade when there’s a supply squeeze and wheat is simply wheat as it consumed by the feed market. In the case of the USA we have HRWW in good supply and SRWW in good supply but HRWW trading at a 13c/bu (AUD$7.30/t) discount to the lower grade wheat.

It reminds me of the joke that done the rounds when the US invaded Iraq, “You know the world is messed up when the best golfer in the world is black, the best rapper in the world is white, and you can’t talk Germany into a war”. It appears thing never really improved.

Cash wheat values out of the US Pacific Northwest were generally flat to lower compared to yesterdays conversions. White wheat was adjusted lower by AUD$2.42 / tonne while US DNS wheat and Canadian spring wheat conversions were less than 50c/t firmer.

Wheat values out of the Black Sea were AUD$1.00 to AUD$2.00 / tonne lower compared to yesterdays conversions. Russian wheat exports have been poor so far this marketing year. By market design or political design one could ask. With Russian wheat export taxes set to zero, one may tend to think it’s more to do with price than supply, is this right. Take Egypt as a consumption price point for the sake of a hypothetical exercise. Russian wheat is roughly equivalent to US$254 CnF, Ukraine wheat roughly US$274 CnF and French wheat of a similar grade roughly US$261 CnF. US HRWW FOB NOLA is valued at roughly US$241 Dec, on a boat to Egypt and it would cost the buyer roughly US$284 CnF.

So Russian wheat is cheap enough to buy demand into their traditional markets. It will be interesting to see where the USDA estimates demand.

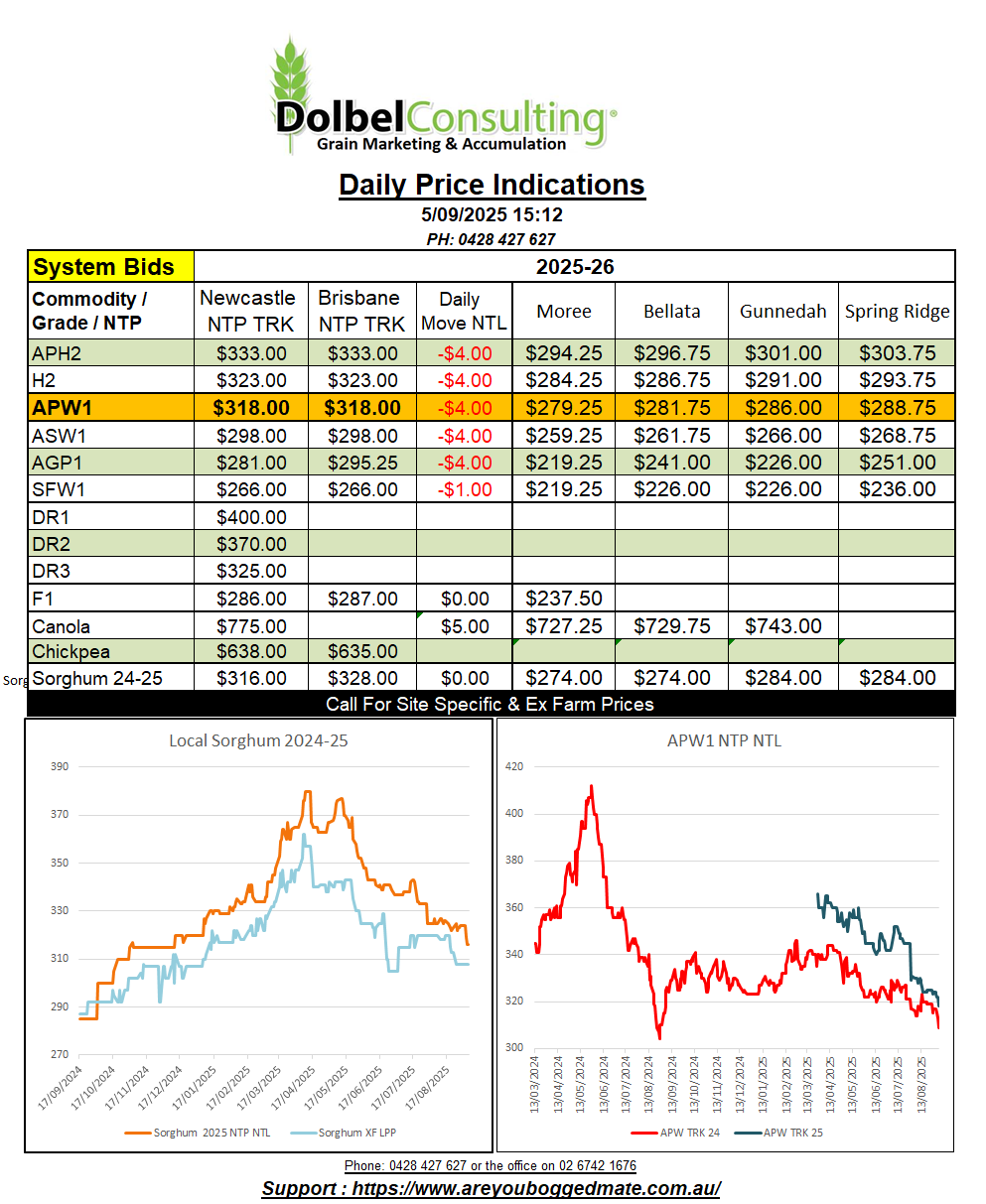

Yesterday unfolded much like the last few, some SFW1 moving to market. Growers continue to clean up old season wheat that was held as either stock feed if required, or a hedge against seasonal changes. The trade was happy to book SFW1 for September delivery at $300 XF SW LPP, roughly equivalent to a delivered Tamworth market price of $325 +/-, a little above where the public bid sheets were pricing it.

Old crop sorghum on the track fell apart, bid at $316 NTP Newcastle now, $289 delivered Werris Creek silo. This sorghum could be executed Free On Truck Werris Creek at $315 / tonne. Freight to Crawfords packing at Werris Creek would be negligible, maybe $10.00 or $15.00 / tonne, equation to a delivered packer price there of $330 at most. This is where the last business I saw was priced at into the Werris Creek packer.

New crop sorghum found a bid of $330 delivered Newcastle port / end user, Brisbane was bid at $334 delivered port. The Newcastle port price gives the grower a sub $300 ex farm LPP equivalent price, so is not attracting a lot of attention. With sorghum not even in the ground yet, and 12 months left of the marketing year, many growers do not see the reward for the risk involved with forward contracting. The last couple of years also saw prices higher at harvest.

The trade tell me there is active grower participation in the new crop sorghum market on the Downs, but south of the border grower selling has been limited.

With new crop ASW bid at $300 delivered Tangaratta it is unlikely that sorghum will be priced into any feed ration in a significant way again in 2025-26, long way to go but. Overnight sorghum values out of Argentina were lower, but much higher CnF China, US values were a smidge firmer in AUD.