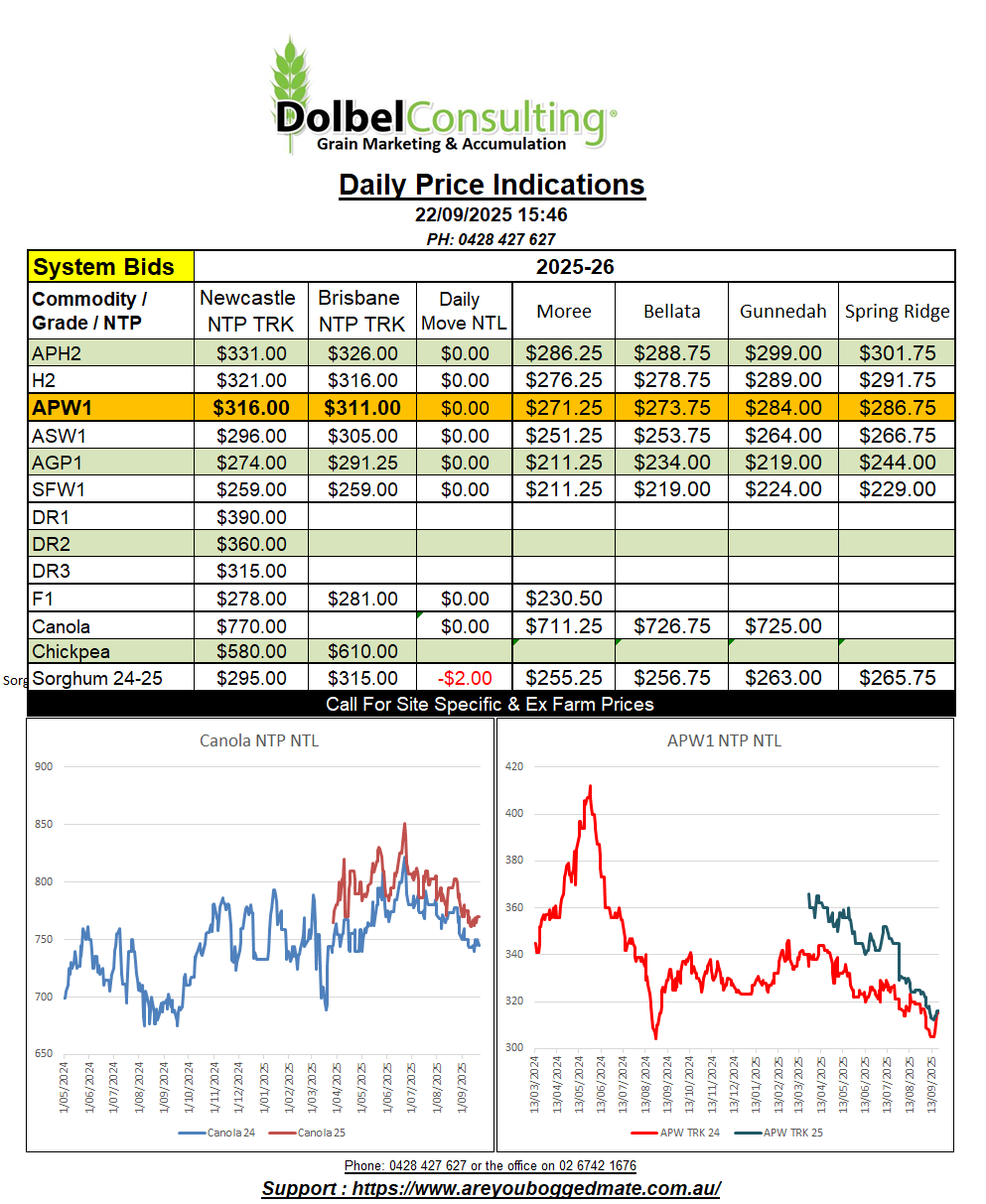

22/9/25 Prices

International grain futures are a sea of red this morning. The stronger USD hurting markets there and triggering further selling. Soybeans were pushed lower on reports that conversations between the US and China are going no where, and will probably continue to go no where ahead of next months OPEC summit in South Korea. Weakness in Chicago soybean futures spilled across the oilseed complex resulting in losses not only to US soybeans and soybean products, but also for Paris rapeseed and Winnipeg canola futures. Malaysian palm oil futures were also softer by roughly AUD$3.60/t.

Chicago corn futures found little support, the prospects of a 420mt+ US corn crop and the stronger USD the main bearish factors. The trade overlooked reports of another 200kt flash sale of US corn.

US corn yields are expected to be high according to the USDA. Even after the USDA reduced their August estimate of 188.8bu/ac (11.85t/ah) to 186.7bu/ac (11.71t/ha) in the September report, that is still a significant increase from last years average of 179.3bu/ac (11.25t/ah) and the 2023-24 average of 177.3bu/ac (11.12t/ha). Some analyst tend to think the current estimate is grossly overstated, and to be fair in some areas where harvest is occurring those estimates do appear to be very high. There was a number of pollination issues in some varieties this year and some rust problems in the south, both of which may have been overlooked by the USDA, time will tell.

When comparing international cash market conversion this morning with yesterdays conversions we see the weaker AUD has helped a lot. Many export values were lower in origin currency but the AUD has in many cases halved potential losses. Many comparisons showed declines of less than a dollar. In simplistic terms the move in the AUD was worth roughly 2c/bu, SRWW futures fell just 1.75c/bu.

The AUD has also buffered some of the decline in canola and rapeseed conversions. Canola bids XF SE Saskatchewan were down CAD$4.66/t for a Dec 25 lift. When factoring in the AUD the move is roughly closer to -AUD$2.66/t. World fundamentals are unchanged as N.Hemisphere summer crop yields unfold.

There are scatted reports of last weeks frost tipping crops across southern NSW. Conditions are OK in these regions and agronomist generally expect to see the crops that have been affected out grow the tipping and compensate with what grains are now filling.

The BOM expected to see frosts across the NSW wheat belt stretching from about Baan Baa south to the eastern Riverina on Wednesday next week. The season has been excellent, if not too wet for some fields, so we may see a similar scenario play out here on the plains where any crops that do experience a little frosting should be able to compensate across the unaffected part of the head or with late tillers. Still it does have the potential to take the cream away.

After building a spreadsheet that basically converts all world wheat values from point of origin to delivered consumer +/- tariffs (not local taxes) it has enabled me to better refine my world cash wheat price comparisons. To better compare apples with apples. Further refinement will take place but it is still very evident that US wheat into the Asian markets is very competitive, but so is Australian wheat at current values.

US sales have been strong and the US have been using import tariffs into the US as a means to negotiate around importer restrictions. Making US wheat very competitive to some Asian buyers. I’m half of the thought, let the US sell now and get out of the way through their winter and our harvest period. The only problem with that is the level of coverage some buyers may get during the next few months. This may make Q1-2 sales of Aussie wheat a little harder, keeping prices lower for longer. Anyone remember one of the main reasons why the pool was set up yet ?

The AUD is back under 66c this morning and should go a long way to countering any negative price pressure on Monday.