23/9/25 Prices

The USDA weekly crop progress report was out overnight. With the US wheat harvest all but complete this report should have a minimal impact on wheat values. There is still plenty of speculation on US corn yields though. Around 56% of the US corn crop is now mature, with 11% of the crop in the bin. The southern states are leading the charge, Texas 76% done, a little ahead of their average pace. Progress in the ” I ” states is slower, but ahead of average, with between 8% and 12% of harvest done in the central corn belt. This is where the big variations on yields appear to be. The US corn condition rating fell back 1pt on the G/E rating, now pegged at 49/17=66% G/E. A rating one might not associate with the type of yields the USDA are currently predicting.

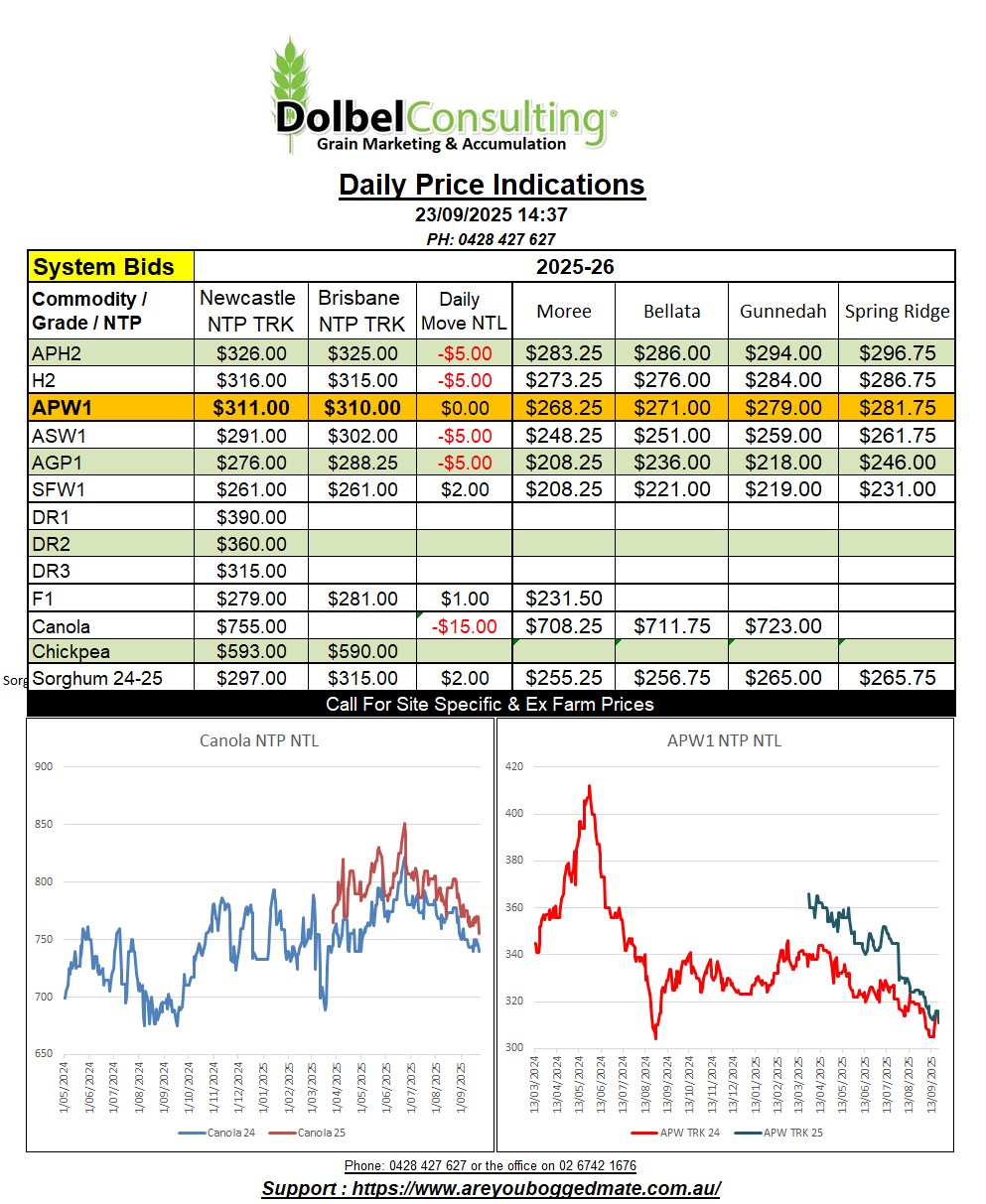

Chicago soybean futures were lower by 14.25c/bu in the Jan26 slot, leading the oilseed complex lower with losses noted at Winnipeg and Paris for canola and rapeseed. Australian canola values continue to draw a premium compared to Canadian canola which is trying to buy market share into the EU market. If the Chinese do start to buy Aussie canola in volume, I imagine the Canadians will be welcome into the EU market. It does raise an interesting point though. If Aussie canola does end up going mainly to China would that still see the enforcement of the ISCC non compliance discount ?

Paris futures were back €3.75/t in the Feb 26 slot. Compared to yesterdays conversion that’s a decline of about AUD$3.56/t when taking currency fluctuations into account. Winnipeg was worse, that day to day conversion comparison falling around AUD$11.43/t. Canola XF SE Saskatchewan fell CAD$9.15/t for a December lift, just over AUD$12.00 compared to yesterdays conversion.

Considering the possible failure of the Ukraine sunflower crop, the implementation of export duties on Ukraine canola and the tightening supplies of EU canola. One may find the move lower in canola values a little perplexing. Is it simply a matter of Canada competing against itself, possibly.

The anchor to the complex remains the lack of US soybean sales to China. Talks are ongoing but are making little progress.

While the northern hemisphere market moves into a post harvest short term glut of grain, local markets begin to gear up for the new crop harvest due to start around the border in mid to late October. The prospect of 30C +/- over the weekend should hurry the process along, as should the lack of any reasonable falls of rain over the next fortnight.

I’ll try and get away for my annual crop drive and video round up of the NWSP over the first couple of weeks of October. If you have a cracking crop let me know, more than happy to do a nice drone video of it for you.

Old crop feed barley on the track, yes there’s still feed barley coming out of the system, was offered for sale yesterday but failed to attract a bid. The consumer appears covered through to harvest, and there doesn’t appear to be trade shorts, or buyers willing to take the risk of getting filled out of the Graincorp system.

The biggest problem for the buyer would be executing the removal of the system barley in a timely manner, at a reasonable location, and without any insect issues. The trade could be allocated system product at any location that Graincorp currently have feed barley stored. Not necessarily the site the barley was delivered to. The GTA location differential that might cover some of the freight difference, but depending on location it may have a huge bearing on the timeliness of execution. The last lot of barley I moved out of the system here on the plains went through at $246 delivered site, roughly equivalent to $290 delivered end user LPP.

Barley, or “poverty grass” as some know it, may again live up to this name in 2025-26. Overnight international feed barley values continued to slip away, falling on average AUD$1.23/t