24/9/25 Prices

Chicago wheat futures improved overnight, taking back much of the previous sessions decline. There’s not a lot of fundamental news that has changed to support the recovery. Technically wheat is cheap, not only from a futures punters perspective but from a physical buyers perspective. US weekly export inspection data, and weekly sales volume, should continue to indicate this. US wheat loadings were very good for the last reporting period and sales data for the period September 5th-11th were not to shabby at 377.5kt but lower than some weeks.

The punters are expecting to see these numbers continue to be strong and shouldn’t be disappointed with the 854kt US wheat export inspection number reported for the week ending Sept 18th either. Weekly US wheat sales are 21% higher year on year.

US corn inspections were also good at 1.329mt, although a little under last weeks 1.512mt, but still very acceptable. Soybeans export inspections were 484kt, back well on last week, but volume is still running a touch higher when compared to the same time last year.

Weekly US sorghum export inspections were reported at 30.6kt, a little under last week, taking marketing year volume to about half of what it was this time last year. Not the end of the world for US sorghum though, as the marketing year only just rolled over on Sept 1st.

US wheat is the impressive grain at present though, export inspections are at 8.711mt versus 7.732mt for the same time last year, almost 1mt higher.

Chicago soybeans done well to finish in the green after news that Argentina has dropped export taxes on beans temporarily. Reuters reported that China had booked at least 10 boats, possibly 15, of Argie beans on the back of the news. A further slap in the face to American exporters is the price, said to be at a premium to US beans. China continues to shun US soybeans at a time when they would normally be booking 10mt to 12mt of Q4 supplies. So far the winners of the trade war between the US and China has been Brazilian and Argentine soybean growers.

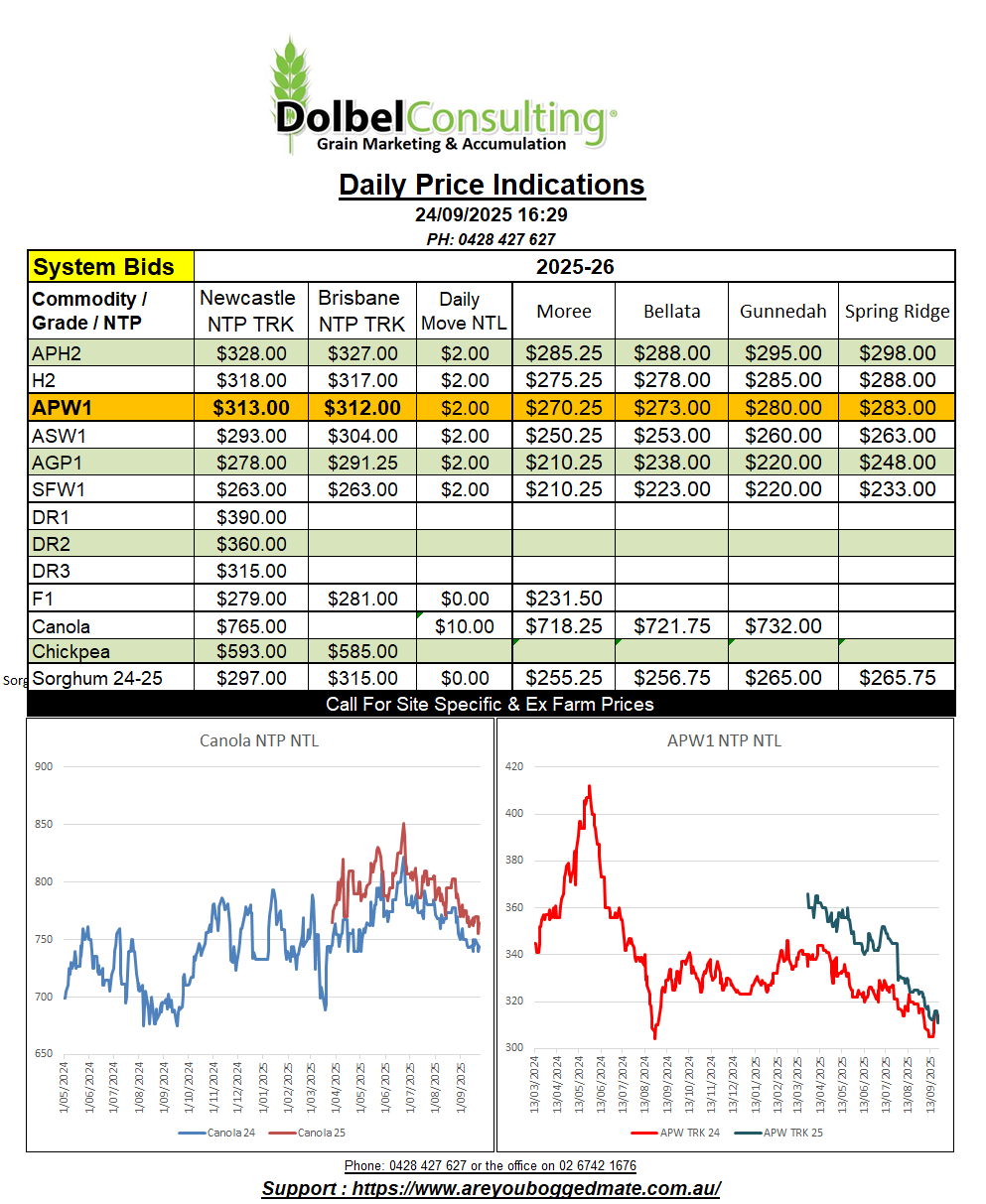

Grain markets remain exceptionally quiet. The downward pressure on the market coming from weaker US futures and ample world ending stocks for most grains. Domestic wheat stocks are set to increase, if not farmer owned, trade and consumer owned. Two good seasons in a row will do that.

Winter crop survey data continues to come in, thanks to everyone that has replied. I’d still like to see some more acre reports come in before I’m comfortable with the analysis, but at present the data is telling me a 47% decrease in barley acres, a 16% increase in wheat acres. I’m a little sceptical on the wheat data, but the percentage is a variation compared to last year, so it could still be close. Durum has basically been abandoned, there’s a 13% increase in year on year acres, but the number of growers planting durum has declined. Canola and chickpea area appears to be up around 20% for each.

If you have not sent me your sown area data please do so as soon as possible.

ASX wheat futures were pushed lower yesterday, following the lead from trade cash bids. Old crop SFW1 was unchanged, actually higher at some spots. ASX futures convert to a delivered Gunnedah silo price of $264.90 for APW1, I don’t need to tell you how terrible that is. New crop APW1 cash bids were closer to $279. Old crop H2 was bid at $352 delivered Newcastle port. One would assume at this stage of the game new crop will probably come in pretty close to this number, but we are not seeing new crop milling wheat bids away from the track market at present.

There is little difference between new crop and old crop SFW1 into the Downs market, both bid around $320 delivered.