26/9/25 Prices

Chicago wheat futures pushed higher as good US export demand triggered some short covering. US sales and export pace for wheat and corn remains very strong. Weekly wheat exports sales ending the week Sept 18th were reported at 540kt. That wasn’t the highest trade estimate leading up to the report, but it was definitely towards the high end of all estimates.

Corn had another blinder, actual sales beating the highest trade estimate, coming in at 1.923mt. Current 2025-26 accumulated US corn sales stand at 25.76mt, this is the largest volume recorded for this time of year…ever, and does not include China on the buyers list.

Reuters reports that China has suggested they would look at US soybean imports if tariffs are removed. With the current counter tariff China has placed on US soybeans it is making US beans more expensive than S.American beans. Some solid reporting their Reuters…..

Trump has announced that the US will distribute aid to US farmers who are suffering due to the impact of tariffs. Trump states that the administration of tariff revenue may include a portion distributed to farmers as aid, before going on the state that farmers stand to make a fortune in the longer term, once the benefit from these tariffs kicks in. This is almost as entertaining as midget mud wrestling.

IKAR, a Russian ag consultancy firm, has raised it’s current estimate for Russian wheat production to 87.5mt, if realised it would be Russia’s second largest wheat crop in recent history. I guess they have a little extra black soil to sow these days. The Russian spring wheat crop saw a perfect season.

International wheat values, including Russian, have been on the move higher this week. This is leading some analyst to call the low for the season in. Things can change quickly but with the recent improvement in EU, Black Sea and US FOB wheat cash values, you can see where they are coming from.

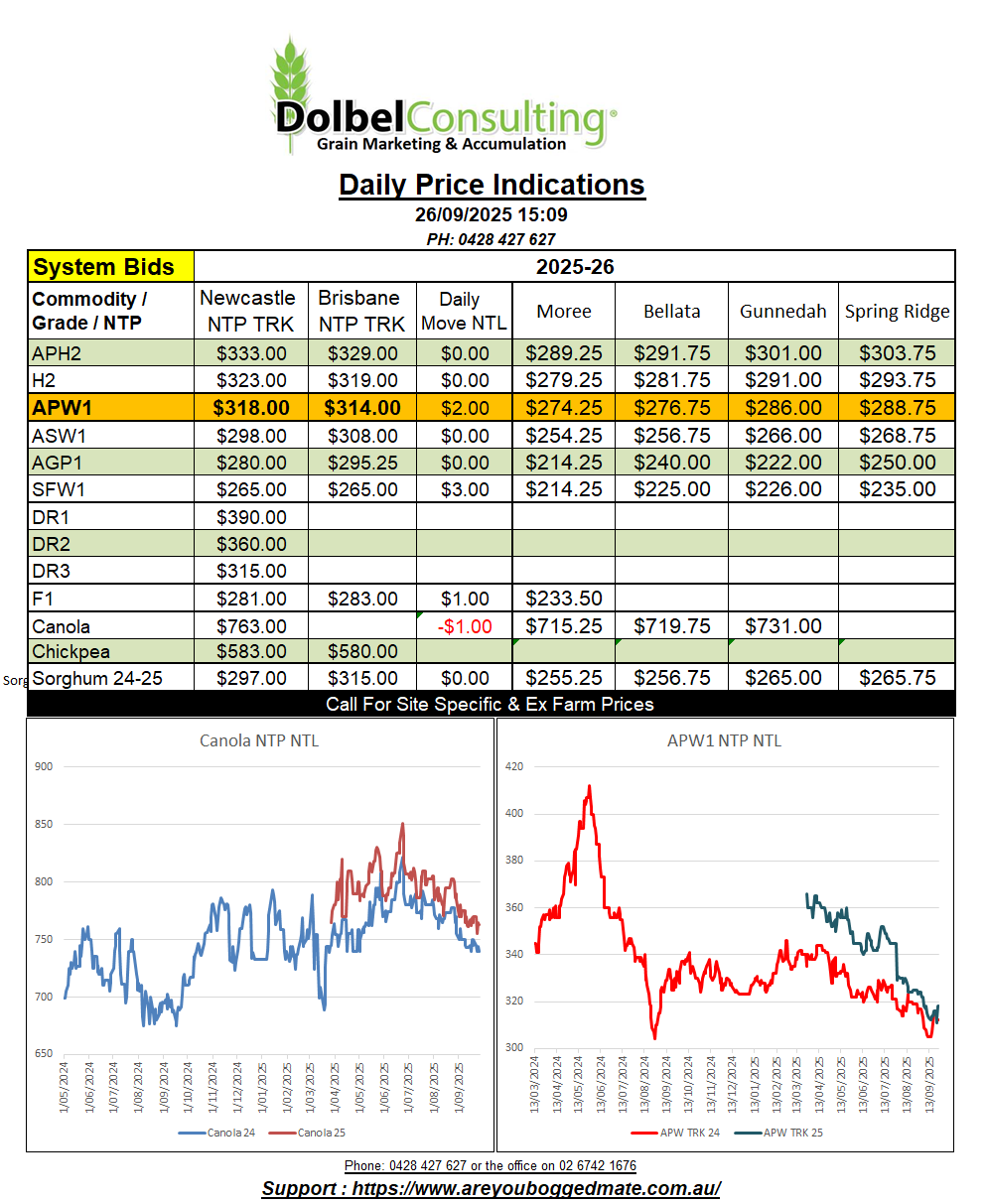

A weaker AUD overnight will help most conversions here this morning.

The Commonwealth Bank has been reported as stating that the AUD will reach highs against the USD not seen since June 2022. Looking back at June 2022 I see it had an average of 70c, a high of 72.65c and a low of 68.68c. Keep in mind the longer term average of the AUD and a number often promoted as the RBA preferred value is 72c. The CBA expect the hangover from US tariffs to hit hard and weaker oil prices to weigh on the US dollar, pushing the AUD towards a “fair value” of 72c. The US FED have stated they are surprised by the minimal impact US tariffs are currently having. Old data I’m assuming.

Gold values continue to push higher. I keep hearing the words of Warren Buffet when I see the lofty value of gold, “gold is generally not a good investment, in a years time a piece of gold is still a piece of gold, it will always be a piece of gold, gold is only good for a hedge against fear”. I remember a wheat analyst once presenting a slide showing a connection between higher gold values and better wheat prices, that’s not exactly playing out at present either.

ANZ, CBA and Morgan Stanley all agree that the AUD will continue to rise as the US FED continue to cut rates at a quicker pace than the RBA will.

As a retailer, I for the life of me, can not see an improvement in the retail sector that would cause the RBA to hold rates, and not try and stimulate the Australian economy with something other than imported house purchases. I guess when the only tool you have is a hammer (interest rates) than everything looks like a nail. I have no faith in the government (red / blue / green or orange) in implementing anything that will have a long term benefit to Australia.

If there was a change in policy in the US, and their import tariffs were dropped, the impact this would have on Australian agriculture could be…. interesting. I hazard to guess in many cases we might even see some ag values fall. Sorghum is a good case study for that move.

Keep an eye on new crop chickpea values today, further small losses at the Delhi market are being countered by the weaker AUD for now.