21/11/25 Prices

US weekly sales data is reported online as of Oct 2nd. Looking at sorghum firstly we see net sales of 170.2kt and outstanding sales of 578kt, which is actually up from the 424.8kt outstanding sales volume for the same date last year. The big difference is the accumulated sales number though, 70.1kt this year vs 244kt last year. Drilling down into the data shows China has bought zero, vs 324.5kt a year ago.

US outstanding sales is looking healthy compared to last year to date, even without China on the books, which is surprising. Pakistan and Mexico are helping but the absence of both China and a little from Africa, will hurt US export volume longer term.

A sale of 110kt US white wheat to Bangladesh was reported. Current values out of the Pacific Northwest for white wheat indicates a value C&F Asia of roughly US$271 per tonne. This compares well to current values for Australian white wheat. Close to H2 value to the grower, but would allow APW to move into that market with some trade margin. The US use of tariffs may have more to do with US activity in “traditional” Aussie markets than physical grain price at this stage.

Arrr yes, remember the level playing field we were all told we would be competing on when the single desk was abandoned… have I mentioned ISCC lately.

US HRWW export volume continues to crush last years numbers, 4.54mt of exports vs 1.788mt this time last year. All US wheat exports is 10.008mt vs 8.243mt last year. Corn is the impressive one though. Outstanding sales of US corn were 22.564mt vs 13.184mt last year.

Back to wheat, with US weekly export sales reported at 888kt, 288kt above the highest trade estimate, I find it interesting that the market actually slipped away. The rapid export pace of US wheat, and corn, if sustained is threatening to make current USDA projections look a little low.

From a global perspective we also see Russian wheat exports increasing, October / November possibly close to record volume. This possibly isn’t a bad thing for those happy to sit out these low prices. The major issue will be how good the northern hemisphere spring is, will it counter a possible lower ending stocks.

As is often the case when a market slips a little, liquidity evaporates. Grower interest in selling was low as storms rolled across the plains. Trade interest in buying was also low, purchases over the last week or two from the north keeping their book full.

With Manildra looking for some stock management solutions and the trade filling up with new crop, we may start to see the protein end of the market soften or trade sideways from here through to the new year. This too, is not uncommon for this time of year.

With little volatility in the international market since Q2 this year the trade haven’t really had massive opportunities to short local or international markets. No trader is going to get rich on basis trading Chicago or back to back trading, but that is where we’re at.

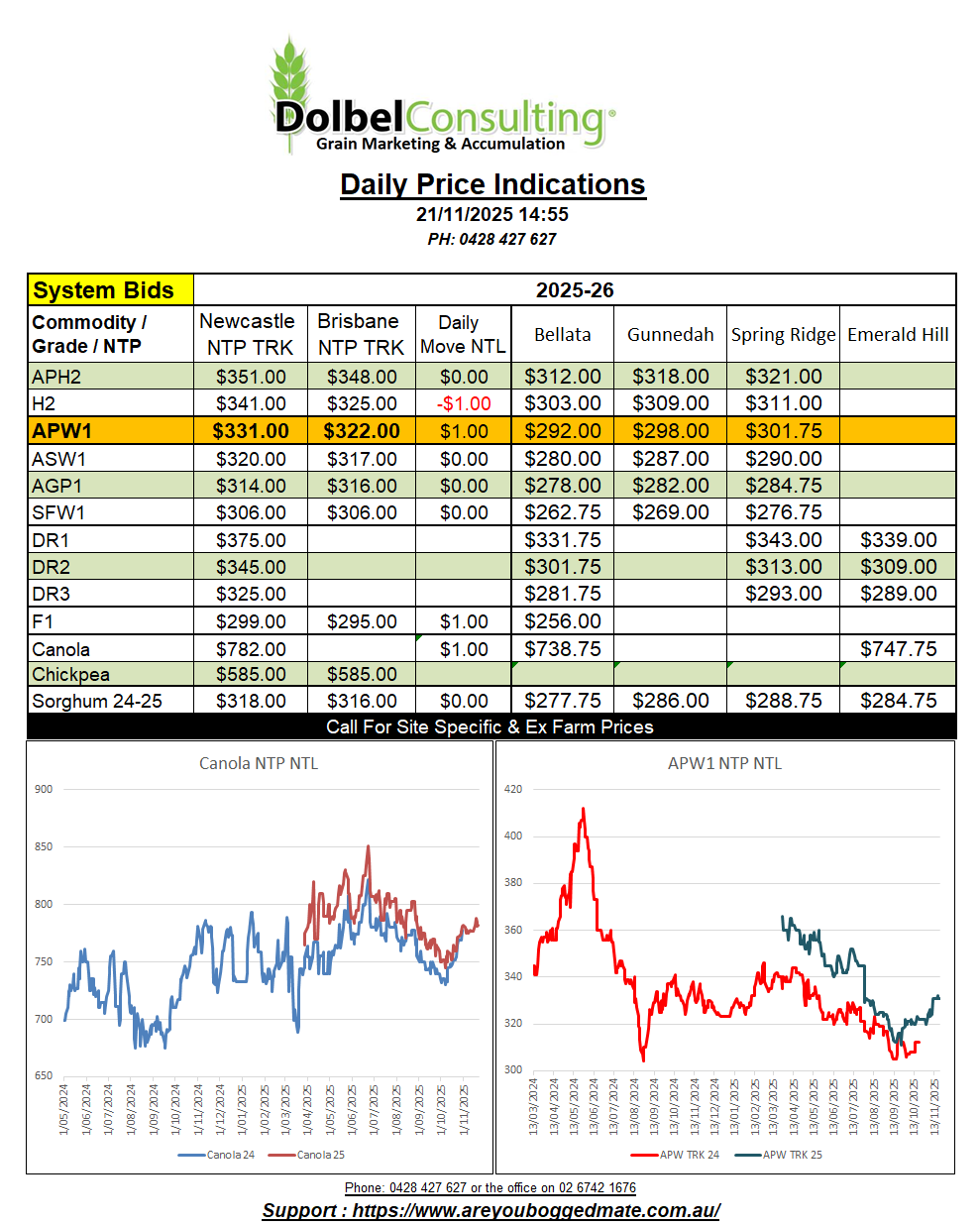

The APW price range on the track this season is $55.00/t. The highest price of $366 NTP NTL was when the contract first became available back in March. By June, the end of sowing, prices were already back to $325, just $5.00 better than what we saw bid yesterday.

As for the SFW1 market, it’s probably been even harder to work with now that Tangaratta are buying ASW as their “feed wheat”, not SFW1. Looking at ASW ex farm LPP we see it topped out at $305….yesterday, for a Dec / Jan slot, after hovering around $285 +/- $15 for most of the lead up to harvest. SFW1 has bounced of the low of $247 set back in September, not that anyone was going to sell at that level, and has come to trade at roughly $5.00 under ASW, $300 XF LPP this week.

These price ranges do highlight the lack of opportunity the trade has seen to position in the local market, and may be hinting that this market could well continue to trade sideways through to mid to late Q1 or early Q2 next year, when the northern hemisphere thaw period and potential volatility.

Showers associated with a low cell along the WA / SA border are pushing across SA this morning. The area of low pressure over western South Australia is expected to stall and move slowly east across SA today and tomorrow. Showers are expected across the SA cropping country, with falls of 3mm to 5mm doing nothing more than delaying harvest activity for some.

A trough line associated with the area of low pressure over S.Aust will move east and into western NSW overnight, combining with another trough line that is persisting along the Newell today. Storms are expected to become active again this afternoon. The ECMWF model predicts storms across the southern parts of the plains from about 3-4pm, pushing east and becoming heavier along the southern half of the plains towards the ranges.

Storms may persist on and off throughout tomorrow morning before developing into more severe storms again tomorrow afternoon.

Storms this afternoon are expected to be more severe towards Coolah and further north towards Narrabri and Wee Waa. Storms west of Narrabri yesterday produced damaging winds and large hail.

Saturday storms are expected to be worse west of the Newell, possibly severe between Warren and Coonamble and north towards Burren Jct.

A surface low is likely to develop over north, western NSW on Sunday night. Models suggests that storms from this development on Monday will be mostly to our east. I’m not convinced that the LPP won’t see some serious storms on Monday if this low does develop, keep an eye on this.