5/12/25 Prices

Negativity in wheat came from the StatsCanada report. Although this data was generally already factored into the market, the confirmation of data is never seen as bullish, unless you are a fund manager with a sell the rumour / buy the fact mentality. Which is becoming more common than one would like to think.

Canadian wheat production was estimated at 39.95mt breaking a 12 year old production record. Not a bad feat given their season of too dry / too wet.

Reuters reports that China is expected to load 6 boats of US soybeans in December. The latest USDA US grain sales report for Oct 30th, yes now more than a month ago. Shows China on the buyers list. We also have US officials claiming that China is on track to buy their usual volume of US soybeans between Nov and February. That’s a big call, 12mt of bean sales in a few months. Just keep in mind sales do not equal shipments. Sales contracts can be cancelled and often are.

There was also talk of two more US sorghum boats being sold to China. US FOB sorghum values slipped away by AUD$2.00 to AUD$3.00 per tonne compared to yesterdays conversions, last night. C&F China values were also lower thanks mainly to the AUD. On the back of an envelope, and including the 10% tariff China has on US sorghum, the US product would be worth roughly US$291 C&F China. The freight rate from China to Australia is roughly US$27 / tonne. Giving the US product and equivalent FOB Aussie price of about US$264, / AUD0.6614 and this is about AUD$399. Without knowing the exact FOBing and insurance costs, and trade margin, it’s hard to get an exact estimate of the equivalent XF value here, but one might assume it’d be somewhere around AUD$334 before trade margin is deducted.

Algeria picked up 810kt to 870kt of milling wheat this week, unofficial reports claim at a value of US$256 C&F Feb. We can assume not Aussie at that value.

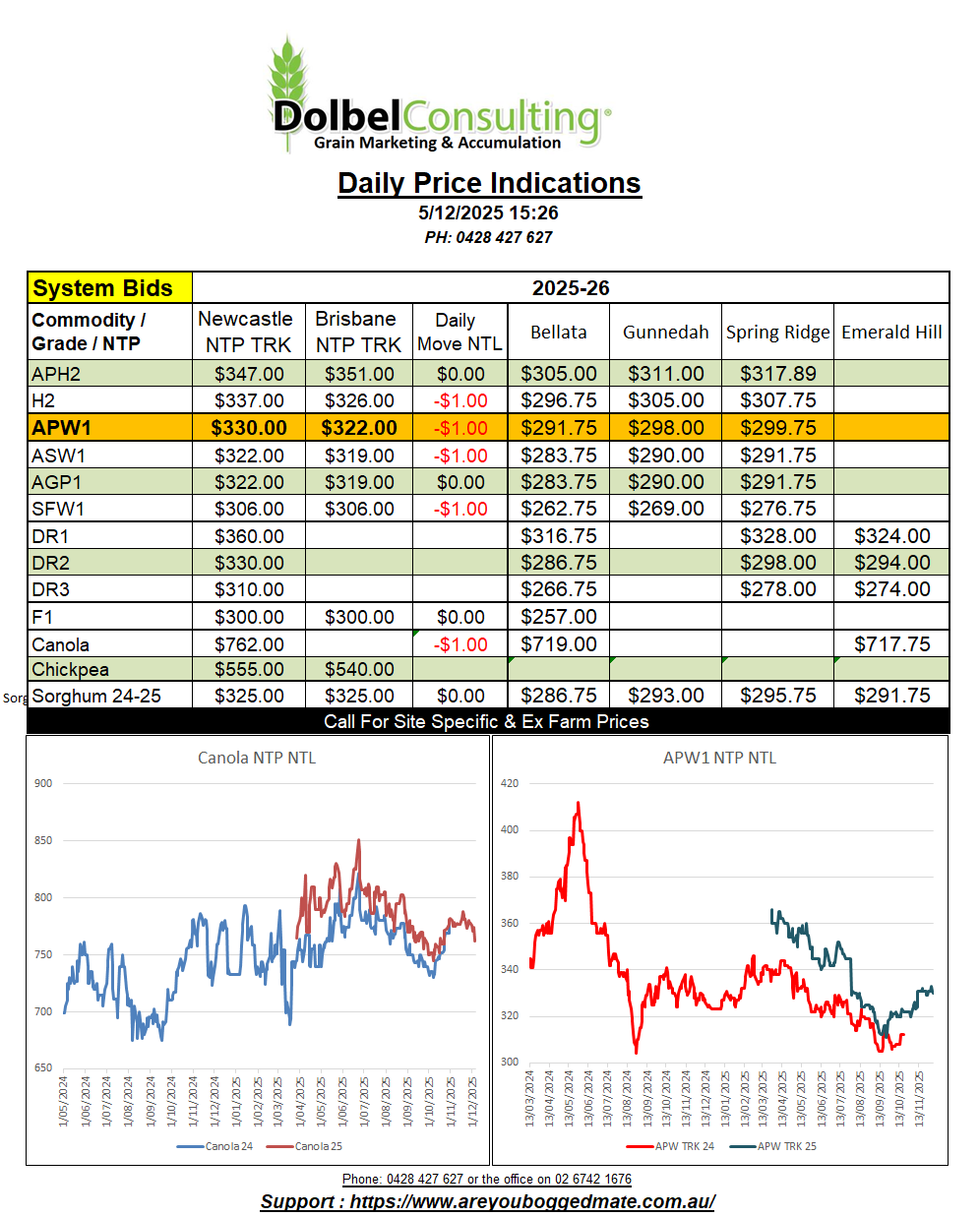

Yesterday was a write off, the stronger AUD appeared to take the high volume / low margin export brokers out of play pretty quickly. H2 milling wheat into the Newcastle port fell away. Offered from the grower at $365 delivered Jan / Feb, bid $355 from the trade. APH2 Newcastle port by road was mixed, generally following H2 lower, but with little on offer by road the bid wasn’t tested. APH did feel stronger than the H2 market, possibly not falling by $10.00 like H2, but more like $5.00.

Milling wheat on the track held on a little better, the basis traders buffering the cash bid a little by increasing basis a smidge. To see basis remaining at +50c/bu through the middle of harvest is not common. Possibly indicating that the producer is not selling this market lower in the volume as high as one might expect to see in December.

If this is the case, that doesn’t automatically mean the price is going to get much better. Come March / April, when there’s traditionally a little volatility in the northern hemisphere crops, we may well see what is now a higher than normal basis turn into more of a harvest type basis, lower. The trade may not pass on volatility in futures as an improvement in cash bids here. I’m not saying this will happen, but it’s plausible given the lack of opportunity in this market over the last several months and the way the trade have buffered out volatility in futures influence in cash bids here.

Feed barley changed hands at $262 ex farm Goolhi yesterday for prompt pickup. There’s not a huge amount of December demand for feed barley at present. Being the logistical nightmare that December often is due to public holidays, most consumers and traders get well prepared early to mid December. Those looking to sell into a Dec home quickly turn into price takers. SFW1 wheat was well bid at $300 XF SE LPP for a January pickup.

Airflow will tend to be from the NW across inland NSW and QLD today, pushing the mercury into the mid to high 30’s. Gunnedah 37C today and 39C tomorrow.

Late Saturday or early Sunday a shallow trough line will move across the NSW wheat belt, reducing temperatures as it passes. We should wake up to a much more pleasant Sunday with a top of 34C. Cloud cover may keep Saturday night / Sunday morning mild to warm.

As the change moves NE across the wheat belt showers are likely to develop ahead of the trough. There’s a chance the CW of NSW will see light showers or storms around sunset Saturday. These showers and storms are also expected to develop across the Hunter late in the afternoon, stretching NW towards Bourke. As we move towards 8-9pm showers should move NE onto the SW edge of the LPP, pushing over the ranges and into the Premer valley.

The system will continue to move slowly NE across the plains producing light showers of 2-5mm around Spring Ridge before midnight.

Showers are likely to persist through to sunrise on Sunday. By then showers will generally be trying to clear to the east, but potentially persisting along the bottom of the plain and towards the ranges. As some heat comes into the day storms are likely to develop across the LPP and along the ranges and coastal fringe. Possibly producing some heavier falls between Newcastle and Taree about lunchtime Sunday. Storms will become more active across the Hunter in the afternoon, tracking NE and becoming severe around Mt Seaview. LPP weekend rainfall is not expected to be more than about 5mm to 10mm.