03/03/25 Prices

US grain and oilseed futures followed the path of least resistance again last night, shedding value across corn, wheat and soybean futures. Corn has been hit hard this week. A combination of the funds clearing long positions accumulated since October last year as a hedge against inflation, and the talk of higher corn acres to be sown in the US come spring as a loose fundamental reason.

There is a degree of switching between corn and soybeans sowing in the USA. Currently corn has the upper hand with price / gross margin in most fields. During the US winter corn futures for the December 2025 slot have rallied from 445c/bu on the 11/9/24 to 477.5c/bu on the 18/2/25, a move higher of just 32.5c/bu. Compare this to the move in nearby futures from 380c/bu to 502c/bu, 122c/bu and you may start to realise the rally may of had little to do with 2025 corn area and more to do with nearby US exports and the assumed inflation hedge.

2024 US corn production was about 377.6mt, back 12mt on 2023 but 30.8mt larger than 2022. US corn exports have been solid, projected at 62.23mt for 2024-25 compared to 58.21mt last year. US consumption has hardly changed. This nets out at roughly 39.11mt of ending stocks, versus 44.78mt last year but stocks were as low as 34.54mt in 2022-23. In Feb 2023 nearby corn futures averaged 671c/bu, this year the Feb average is 488c/bu, 2024 Feb 423c/bu. This would mean that the market has been about half as volatile between 2023-24 and 2024-25 as it was during the 2022-23 – 2023-24 seasons.

With a US stocks to use ratio for 2024-25 at 10.19%, compared to 9.92% in 2022-23 one may have expected to see more volatility, throw in the additional exports and one might even become skeptical that this current sell off isn’t just a bear trap (famous last words).

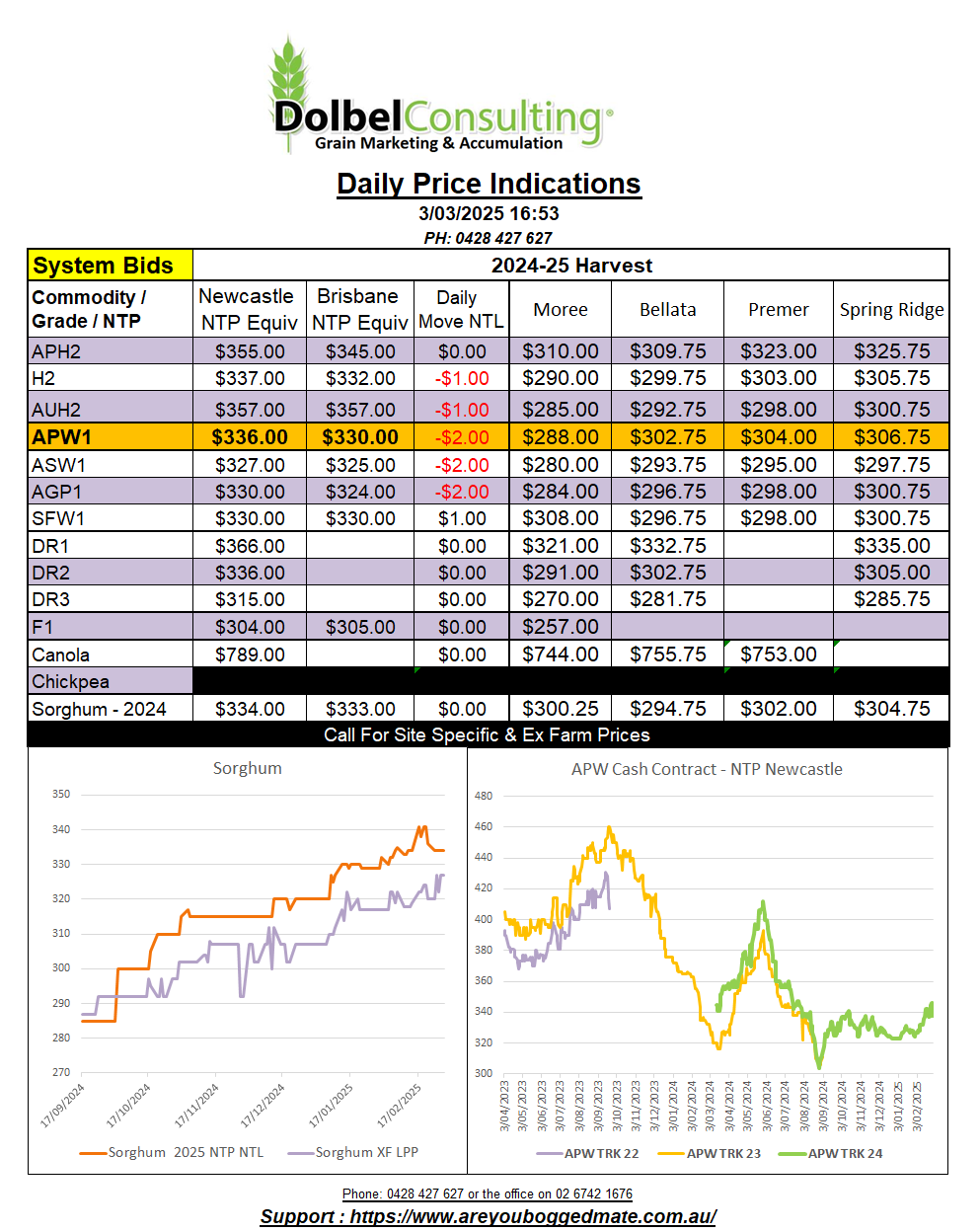

Corn values do have a bearing on sorghum price, not to the extent it used to 20 years ago, but it still does. Volatility in corn will often feed through to the sorghum price. The USDA announce the US sowing intentions report on March 31st. The punters are all about a large corn sowing this year. A variation from that assumption may lead to additional volatility in April / May.