20/5/25 Prices

There are a couple of things at play here, poor weather in Europe and good weather in the US. You may not think that looking at US futures versus Paris futures though. Chicago wheat, corn and soybeans all closed in the green last night. Paris milling wheat was back €2.00/t in the September slot and -€1.75/t in the December slot. Paris corn was flat to softer, and London feed wheat shed £0.80/t nearby and £0.85/t in the Jan 26 slot.

The only product at Paris that had some upside was rapeseed futures, closing €1.25 higher nearby and €0.75 higher in the Feb 26 slot. Cash bids for canola ex farm SE Saskatchewan were also higher, closing on average C$1.35/t higher for a June lift and C$1.23/t higher for a Sept 25 lift.

All in all nothing moved significantly higher when compared to wheat futures. The reality for us when taking the AUD into account may be a little different though. HRWW out of the US Pacific Northwest was on average about +AUD$0.65 /tonne compared to yesterday’s conversion. US Spring wheat out of the PNW was a little better, the comparison there up AUD$4.25 / tonne. Canadian spring wheat out of the PNW was not as keen to push higher, up just AUD$2.83 / tonne compared to yesterday. These moves do keep US HRWW at a very competitive price into the Asian consumer.

The USDA weekly US crop progress report was out after the close. Corn sowing is progressing well at 78% in, just above the 73% average. Soybeans are 66% sown (53% avg) and sorghum is at 33% sown, 2pts above the average pace. The winter wheat crop condition rating was back 2pts in the good to excellent range, now pegged at 44/8 G/E. Last weeks HRWW crop tour did note a little disease creeping into some fields, but this weeks condition rating for Kansas has improved 1pt to 43/6 – 49% G/E. Around 71% of the Kansas wheat crop is now in head. Kansas, Nebraska and much of the central corn belt remains drier than average, hence the good sowing pace for corn and beans. The spring wheat region is wet though, western N.Dakota seeing 50-70mm last week.

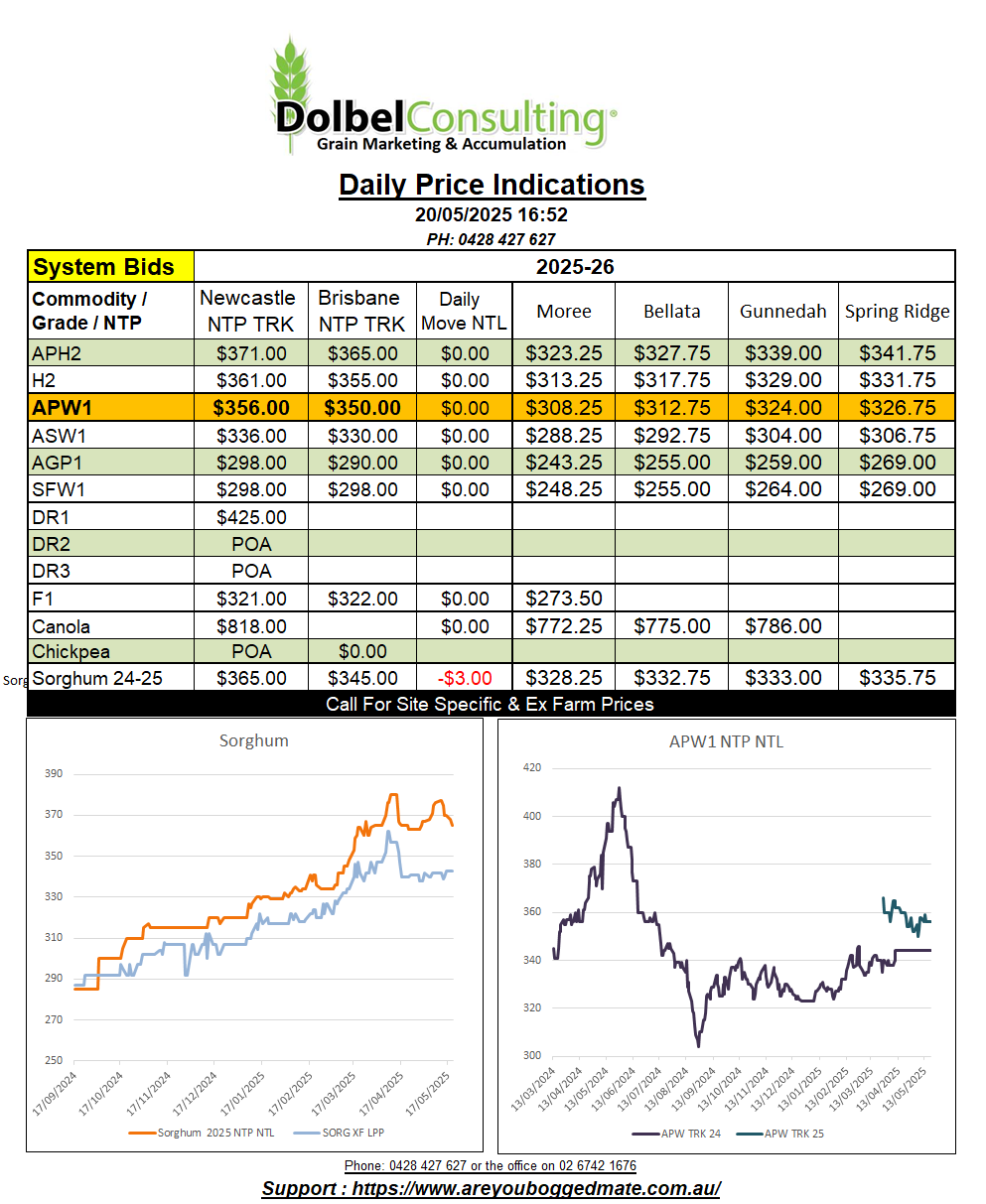

We are starting to see a little more weakness in track sorghum vs delivered Newcastle port by road, which is hanging on to last weeks value. This may be reflecting the current trade position for bulk shipments through NAT vs Carrington, and / or the demand period for further export requirements through Carrington. Without a stem report that reflects future port demand, not current nominations, it’s hard to tell.

The track market saw little volume on the offer side to test the resolve of the bid. Werris Creek found generic buying interest “at the bid” which topped out at $341.50 / tonne delivered site, roughly $368.50 NTP NTL equivalent. Buyers are site specific with their track bids though, some showing little interest in ownership at some sites west of the main track.

Delivered Carrington by road was bid at $388 June / 1st week July. The buyer, as always, is yet to appear on the current stem report as a nomination for shipment in July. The buyer is also telling me that they are nearing their accumulation requirements for this vessel.

This does raise a valid question, with nominations for Newcastle port at 214kt, and a projected bulk demand of 394kt, that leaves a balance of 180kt to appear on the Newcastle stem over the next couple of months. Let’s say that August is the last month of nominations, so three months left, that’s only 60kt per month. There has been more 30kt +/- boats than 55kt+/- this year. Maybe the trade are taking it easier on ship size after last years quality issues. But this does indicate just 1 or 2 boats to appear per month to complete the sorghum program between June and August …. if the 394kt is the correct assumption.

Overnight international sorghum values were AUD$3.00 to AUD$10.00 lower, Argie values hit the hardest. Now US$2.00 cheaper Cif China than Aussie.