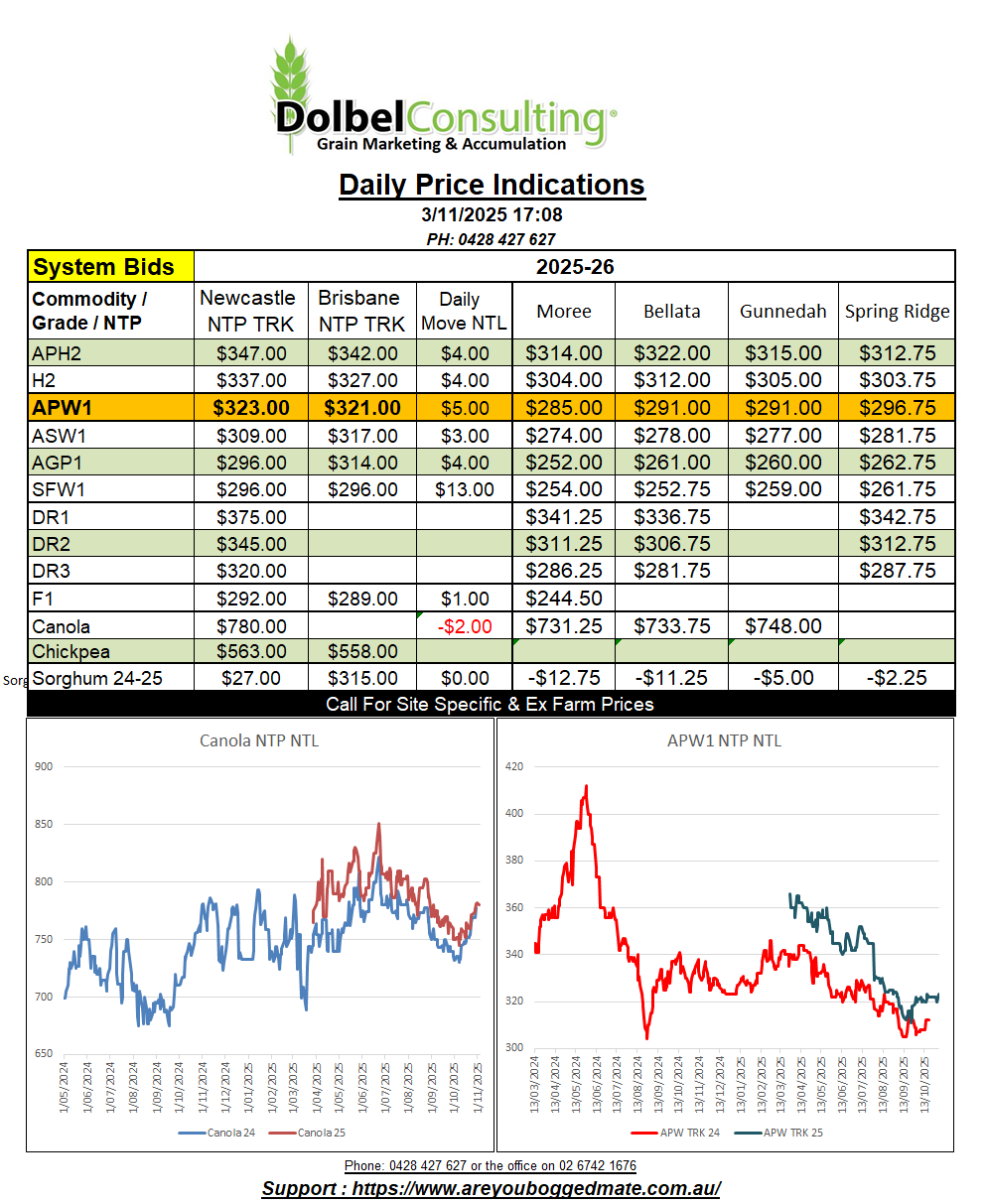

3/11/25 Prices

International wheat values are generally higher this morning. Cash values out of the US Pacific Northwest saw good gains in HRWW, the day to day conversion comparison increasing by roughly AUD$6.44/t. Spring wheat values were also firmer, not by as much as HRWW though. Canadian spring wheat out of the PNW was up AUD$2.43/t compared to yesterdays conversion. This puts Canadian and US spring wheat within a couple of dollars of each other into the Asian market, and Aussie APH wheat right between US and Canadian spring wheat values at a C&F Asian consumer basis.

Over the last 12 months US HRWW had drifted below SRWW values, that’s a little like seeing H2 wheat here being cheaper than APW / ASW wheat.

At the moment we are seeing ASW bid at $320-25 delivered LPP end user, and H2 being bid at $300.75 delivered Spring Ridge silo. Indicating the track is no place to take your LPP wheat at present. H2 isn’t seeing too many bids at the port by road level, but one might expect to see numbers similar to the Brisbane bid of $355 delivered for H2 in time, but still only equivalent to $315 XF LPP.

I’ve attached a chart of the US HRWW / SRWW values over the last twelve months. One might expect this inversion in quality to price to swap back around to see HRWW at a premium to SRWW again by the US harvest next year. If this is the case, would it signal an improvement in HRWW values or a decline in SRWW values. If I was a punting man I’d back the former.

Canadian XF canola values out of SE Saskatchewan and French FOB rapeseed values were sharply lower overnight. Paris rapeseed futures fell €2.75 in the Feb26 slot. The average ex farm SE Sask canola price came in at CAD$572.51/t, down CAD$11.50/t for a December lift. This puts Canadian canola into the EU market at roughly US$70 under the Aussie product off the east coast. If Canada was exporting to China their product would be roughly US$63 under the Aussie product. Interesting to note both canola and rapeseed values falling as Chicago soybeans closed 7.5c/bu higher in the Jan slot.

Why I’m not bearish wheat. In saying this I need to emphasise I could be wrong and there’s a myriad of outside influences that could prove me wrong, but as things stand at the moment I’m not bearish wheat.

There are a few reasons, ranging from how much lower could it go before we see a big reduction in local and global production, and at what value does the international trader simply stop selling in a flat price market. We also have the weather to contend with. At the moment the northern hemisphere is sowing or getting close to finishing sowing their 2026 winter wheat crop, and some places have had a difficult sowing period.

Take China for instance. There’s been a lot of rain in China, and a lot of that has been across the major winter wheat regions. It’s always hard to confirm what is going on in China, but until sown area is confirmed by satellite images in the spring I’m going to assume that there will be less acres in China than usual.

Dry weather is also causing a few issues in Europe, the USA and Canada, and Turkey has been dry for a while now.

Russia, Ukraine, Romania and Bulgaria are all seeing above average rainfall. Some parts of Romania and Bulgaria as much as 150mm over the last few weeks. Granted, it is long time between today and the northern hemisphere harvest, and sowing into wetter soil versus drier soil is preferable, but I’d still like to see if the less than ideal weather, especially in China, has an impact on global sown area before making a sales decision on 2025 wheat. It may just be a good year to dribble wheat onto the market, weighting volume more towards Q2 in 2026.

The trade continue to seek ASW+ for delivery into the Liverpool Plains consumer market. Grades further north appear to be mainly H2 or better, and there has also been a few rain delays dragging the expected volume on the market down. ASW delivered Tamworth was bid at $325 prompt yesterday.

The radar and satellite images tend to indicate that the weather is mainly to our east as of 7.00am this morning. Overnight rainfall was minimal away from storms and even limited for those that got under a storm. Gunnedah 0.4mm. Storms were generally more across the northern parts of the Inner Downs towards, some storms producing cricket ball sized hail around Jondaryan and east of Warwick.

Further south Mudgee and across to the Upper Hunter saw 5-10mm, and Cowra picked up 6mm, further west saw lesser falls, West Wyalong 4mm.

The BOM synoptic charts shows the area of low pressure over the western Downs that is producing the storms to our north dissipating as it drifts further north over CQ this afternoon. The trough line will remain intact though, stretching from about Hebel to Mt Isa and then west across the tropical north. There’s a good chance storms will develop along this trough line again this afternoon, but should be more active across the Downs, CQ and the SE corner of QLD.

The maps start to get interesting again on Monday. A low cell will be located off the west coast of Tasmania. A deep trough line is expected to extend north away from the low, stretching all the way to the Gulf. As the trough passes across the NSW wheat belt on Monday night and Tuesday morning storms are expected to develop. The ECMWF model predicts the most severe storms will be across the Downs on Monday night. Weaker storms developing across the NSW CW will track east, intensifying as they do and arriving across the LPP around 11.00pm to 1.00am Tuesday. Falls of 10-20mm are possible on the LPP.