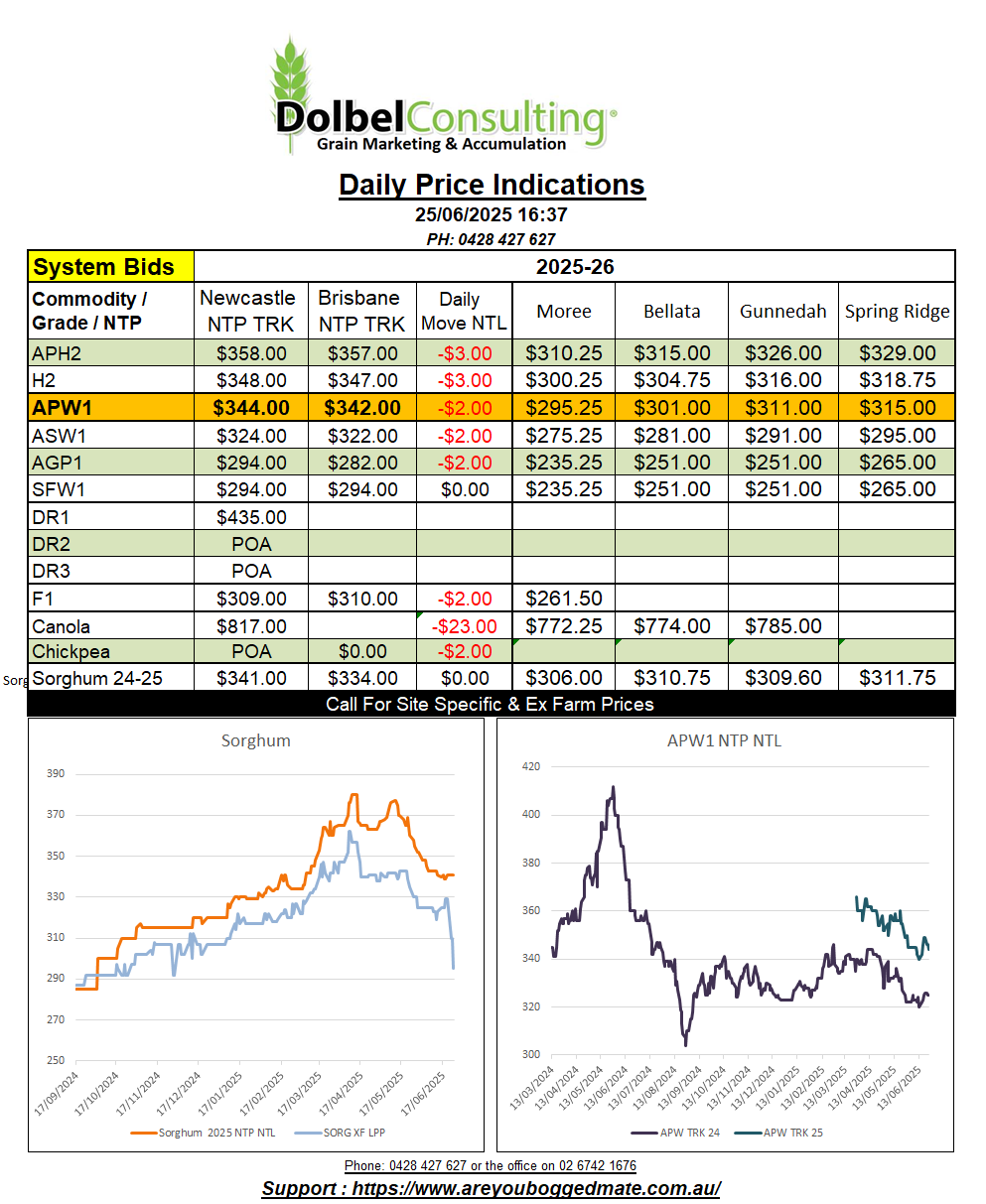

25/6/25 Prices

International wheat cash and futures values all trended lower yesterday. Risk off ?, who knows. The US weekly crop condition report wasn’t exactly bearish wheat that’s for sure. Falling quality ratings in both US spring and winter wheat, delays to harvest, all pointed to a stronger open but it was not to be. Pesky fundamentals getting in the way of technical trade, how dare reality be considered.

The reality is probably more downward pressure from an international perspective unfortunately. Black Sea values have started to slip lower as we move closer to harvest there. Regardless of the dry finish in both the black soil country of Russia and the Ukraine, the world continues to expect to see both as competitive exports of wheat in Q3 – 4. Overnight Russian FOB offers were back roughly AUD$7.69/t compared to yesterdays conversion into an Asian consumer. This mornings conversion for Ukraine wheat values are back even further, down just over AUD$10.00 / tonne.

US values out of the Pacific Northwest were also lower, not as bad as the futures market, but still lower. White wheat did buck the trend, remaining steady, while spring wheat from the US slipped just AUD$3.53/t compared to yesterdays conversion. HRWW was the big loser though, PNW values back AUD$10.06/t day to day to an Asian market. The fall does bring US values back more in line with H2 values CiF same end user. HRWW now just a couple of bucks under a white wheat of the same protein level.

The elephant in the room will be canola and rapeseed, both shedding a bunch of value overnight. Look for sharply lower new crop values for local canola this morning. Some of this downside is probably spill over selling from oil, WTI crude falling USS$4.14/b overnight. Soybeans at Chicago didn’t help, shedding 12c/bu nearby and 9.75c/bu in the Nov slot. Palm oil was up a smidge though, stopping the slide of the last couple of days. Looking at comparable values for Aussie and Canadian canola CiF Europe, we see that Aussie canola is now just US$20.00 over Canadian values. Further erosion in price here is predictable but we could potentially start to see some basis improvement too.