1/8/25 Prices

Russia continues to be a major wheat exporter for the year ahead. SovEkon raised their export estimate by 400kt to 43.3mt the current crop being harvested. The Russian harvest is producing a mixed bag of results after a slow start. There has been areas in the south affected by drought, seeing reduced yields but good quality, while some regions in the north have seen average yields and quality. Further east along the border regions with Kazakhstan spring wheat production should be very good this year, possibly countering the impact of dry weather around the Black Sea.

Total Russian wheat production is estimated at 83.6mt according to SovEkon. Russian domestic values to the farmer are low, bid between US$190 and US$182 per tonne for 12.5% protein wheat. The lower prices coming more recently. This has not been received well by the producer, which appear to be standing back out of the market in hope of better prices going forward. This may be wishful thinking if the total production estimate is correct though. World wheat production is good again this year. Although not exceeding demand the draw down on world stocks is not a lot and we continue to see a global stocks to use ratio about 30%, that’s never a good sign and generally predicts a tough marketing year ahead for wheat.

With the EU limiting Ukraine imports this year, marketing wheat out of the Black Sea will be a tough gig. Competition from Romania, Bulgaria and Ukraine into the Middle East and North African markets will be fierce. Currently we see Ukraine wheat still priced above Russian wheat, this may allow Russian exports to pick up quickly in the short term. With Russian monthly exports expected to pickup from last month 2.1mt to the more traditional average of 3.1mt (or more) in August. Ukraine will need to do more than send envoys to Egypt, they will need to convert these meetings to physical sales.

Overnight cash values out of the US Pacific Northwest were generally a smidge higher in AUD/t. Hard red winter wheat lead spring wheat higher, gaining roughly AUD$2.39/t over yesterday’s conversion. Values XF SE Saskatchewan were up CAD$1.90 tonne for 1CWRS13.5% wheat.

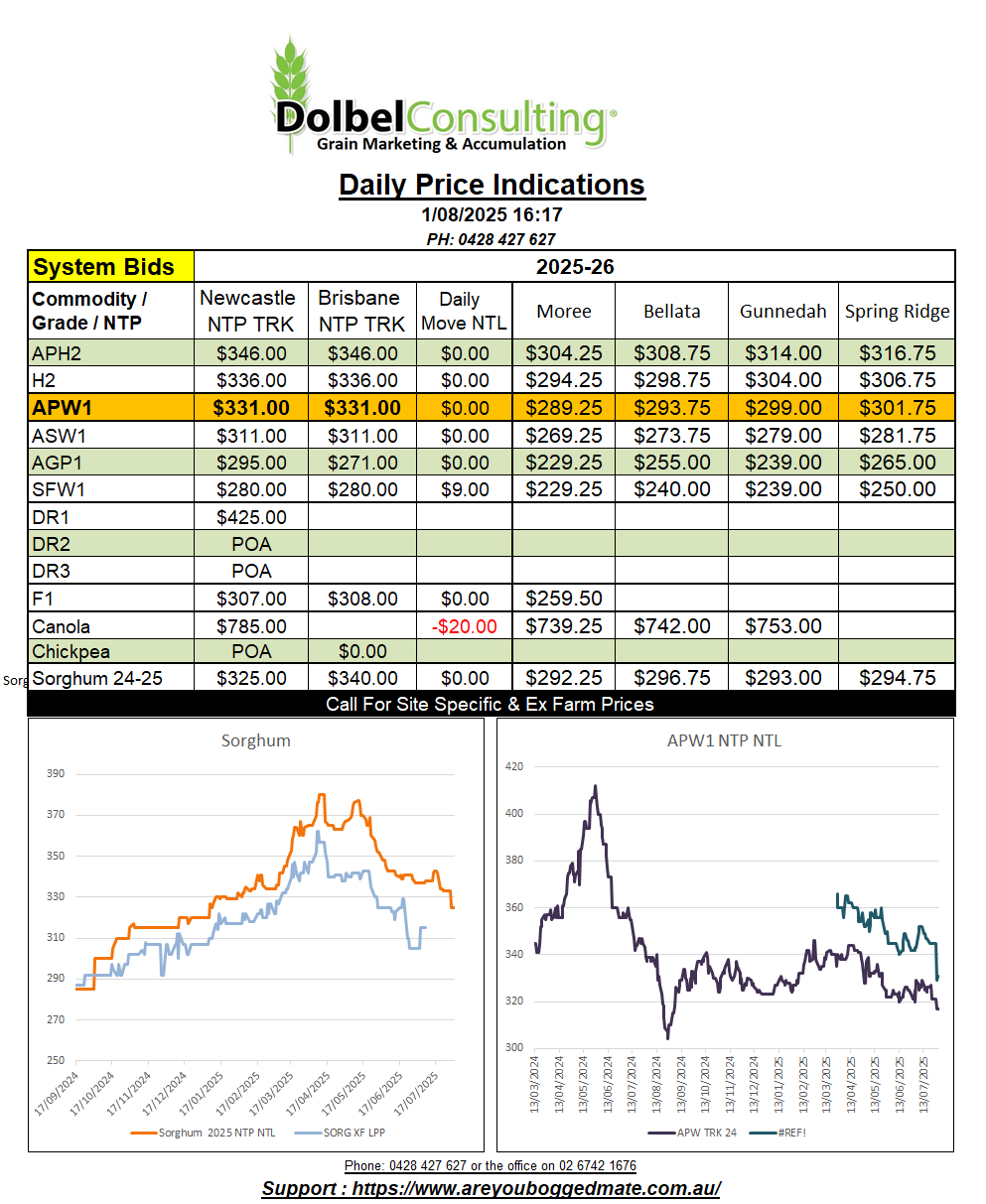

Looking at the ASX wheat futures numbers this morning I see the traditional new crop slot, Jan 26, was back $3.00, but the March 26 slot was up $6.00. This reflects a terrible basis number for cash bids here versus ASX, just +$5.69 / tonne. The new crop wheat market hasn’t really offered us any local physical marketing opportunities this year. To be fair even bank swaps now take opportunity away with varying basis to Chicago futures. It really is making new crop marketing hard for not only the producer but also the smaller traders.

The difference in price at a delivered Gunnedah silo level for ASX futures for January vs March is +$7.95/t. January ASX $283.76, March $291.71 using last seasons Graincorp storage and handling costs. The cost of carry from 1st January to 1st March is two months storage + money charges if accounting that way, roughly $4.40/tonne.

The Aussie dollar has remained flat to a smidge lower against most of the majors overnight. A slight gain against the yen but generally softer against the US dollar, Euro and Indian Rs. In the case of chickpeas the reduction has been enough to turn a slight fall in Delhi market values into a slight increase in AUD per tonne. Currently we see Delhi chickpeas trading at more that AUD$133 / tonne above their minimum support price, those sneaky government “grain traders”.

Local new crop durum values were unchanged yesterday, not a bad feat considering the sudden weakness in French values. Overnight port La Nouvelle values were again lower, shedding roughly AUD$1.83/t compared to yesterdays conversion. Canadian 1CWAD13 bids were unchanged.