5/8/25 Prices

Canada had the day off, so no data from Winnipeg this morning. Cash bids across SE Saskatchewan were generally flat to lower for wheat and durum while a smidge higher for canola. US values out of the Pacific Northwest were generally less than a dollar lower for wheat, including white wheat. Canadian spring wheat out of the PNW was flat.

The USDA weekly crop progress report shows corn unchanged at 73% G/E, 42% dough stage. Soybeans at 69% G/E, back 1pt on last week and 58% setting pods. Cotton at 55% G/E and 5% opening bolls. Spring wheat at 47% G/E, back 1pt on last week and 5% harvested. Winter wheat was estimated at 86% harvested a 6pt jump week on week.

Last week saw weekly US export inspections for wheat at 600kt, this was the higher end of trade estimates. Net weekly US wheat sales were pegged at 592kt, although high this number was down 17% from the previous week, it’s still a relatively robust result. No new US sorghum sales were reported.

US wheat continues to be priced well into the Asian market. At current values HRWW is roughly US$7.00 less than new crop H2 into the Asian consumer. Russian wheat of a similar protein would land into the same consumer market for roughly US$11.00 under Aussie H2.

The US continues to use tariffs to push trade deals. This may see some Asian consumers switch to US product that may have otherwise bought Russian or Australian wheat if the price dictates. This is not great news for Australian demand and may see exports into some Asian market shrink a little in 2026. For some the next US election, Nov 2028, may not come soon enough. The Trump administration continues to create volatility across most international markets. Good for some in the US, but dare I say it, more likely better for his closest friends, than many of his international allies.

Localised flooding around Gunnedah continues this morning. The river had sustained a 8.5m +/- peak for over 12 hours, and is currently (7.00am) sitting at 8.75m, oddly a 24cm rise over the last 30min, this is the maximum reading it has registered over the last 24 hours.

The flow rate is still strong at 145kML/d, as of 4.30am. The Peel R and downstream of Keepit has fallen away, the flow rate is also reduced significantly. The Namoi R downstream of Keepit is falling but the flow rate is still at 49.9kML/d, which will sustain a very high flow within the banks. The Namoi R at Boggabri continues to rise and is currently sitting at 8.12m, minor flooding occurs at 7.0m there. Lake Keepit sits at 104% of capacity.

That’s the long way to saying it’s bloody wet. It’s not often you see a flood on the back of 70mm of rain over a week. A few things that I noticed while watching river stations over the weekend was the sharp spike in flow rate in the Peel R at the Appleby lane station. It jumped significantly at one stage by over 20kML/d in a short time frame and kept climbing. Someone said it was snow melt, others suggesting a storm in the hills, probably a combination of both. Moore Crk & Attunga Crk all catch off the Moonbi and to the SW of Bendemeer, they flow into the Peel R near Appleby lane. Creeks to the north flow into the Namoi R east of Manilla. The flow rates for the Namoi above Keepit were also very high, 60kML/d+, Manilla township seeing 71mm over the 2nd and 3rd of August.

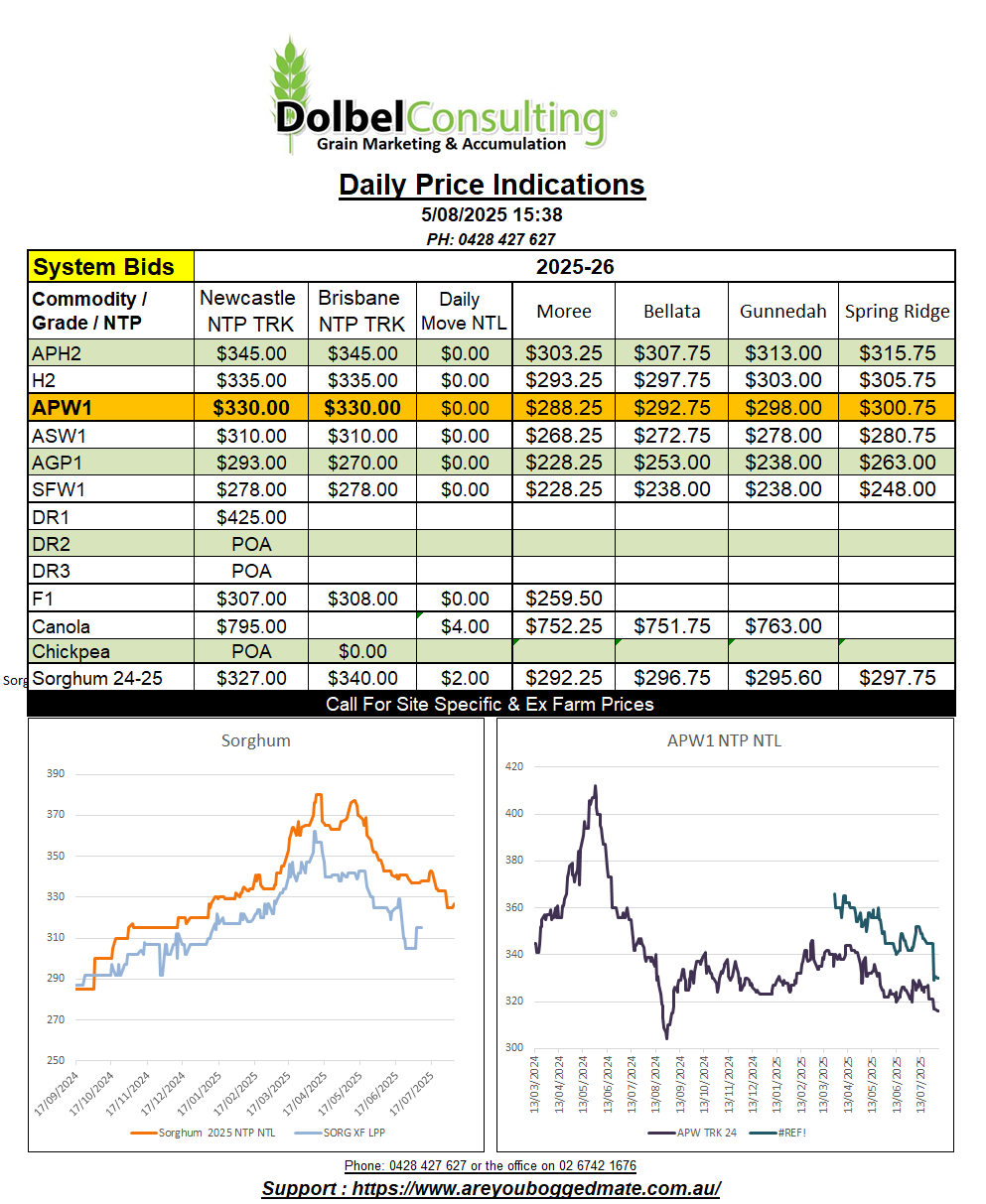

Not seeing a lot of demand for grain at present. Some interest in sorghum ex farm LPP for Sept / October / November packing, bid at $315 to $325 ex farm LPP depending on pickup window and location. New crop wheat remains range bound and soft. Canola values appear sustainable.