8/8/25 Prices

There’s a USDA World Ag Supply and Demand Estimates (WASDE) report due out next Tuesday US time. There are a few trade estimates around prior to the release. Currently the trend seems to be expecting increased corn and soybean yields and production over last months estimates. US corn production is expected to see a significant increase year on year, possibly by as much as 28mt higher. US soybean production should be similar to last year.

US weekly wheat export sales continue to the very good, once again exceeding pre-report estimates of 350 – 600kt. At 738kt, sales are up 25% week on week. Appearing on the list is Nigeria 185.9kt, Bangladesh 165kt, Mexico 105.9kt, S.Korea 89.1kt and Philippines 68.4kt. These sales were off set against some adjustments and cancellations to net back to the 737.8kt total.

US corn sales were poor at 170.4kt, down 50% week on week and down 71% from the 4 week average volume. There were no reported sorghum sales for old crop sorghum and just 34kt of new crop US sorghum sales to Mexico. Total weekly sorghum export volume was back 95%, all to Mexico.

The good sales data for wheat rolled across to form support in both futures and physical pricing. Hard red winter wheat values out of the US Pacific Northwest improved. A day to day comparison of HRWW values into the Asian market and then converted back to an Aussie port equivalent price shows a move of +AUD$4.45 / tonne after taking currency fluctuations into account. The US white wheat conversion comparison out of the PNW was also higher, up AUD$1.56/tonne. While both US and Canadian spring wheat values out of the PNW were relatively flat.

Both Paris milling wheat futures and cash values FOB Rouen were higher, futures faring a little better than cash. The day to day conversion comparison for 12% wheat FOB Rouen was firmer by roughly AUD$3.82 / tonne, Paris milling wheat futures firmer by €3.25/tonne in the Dec slot.

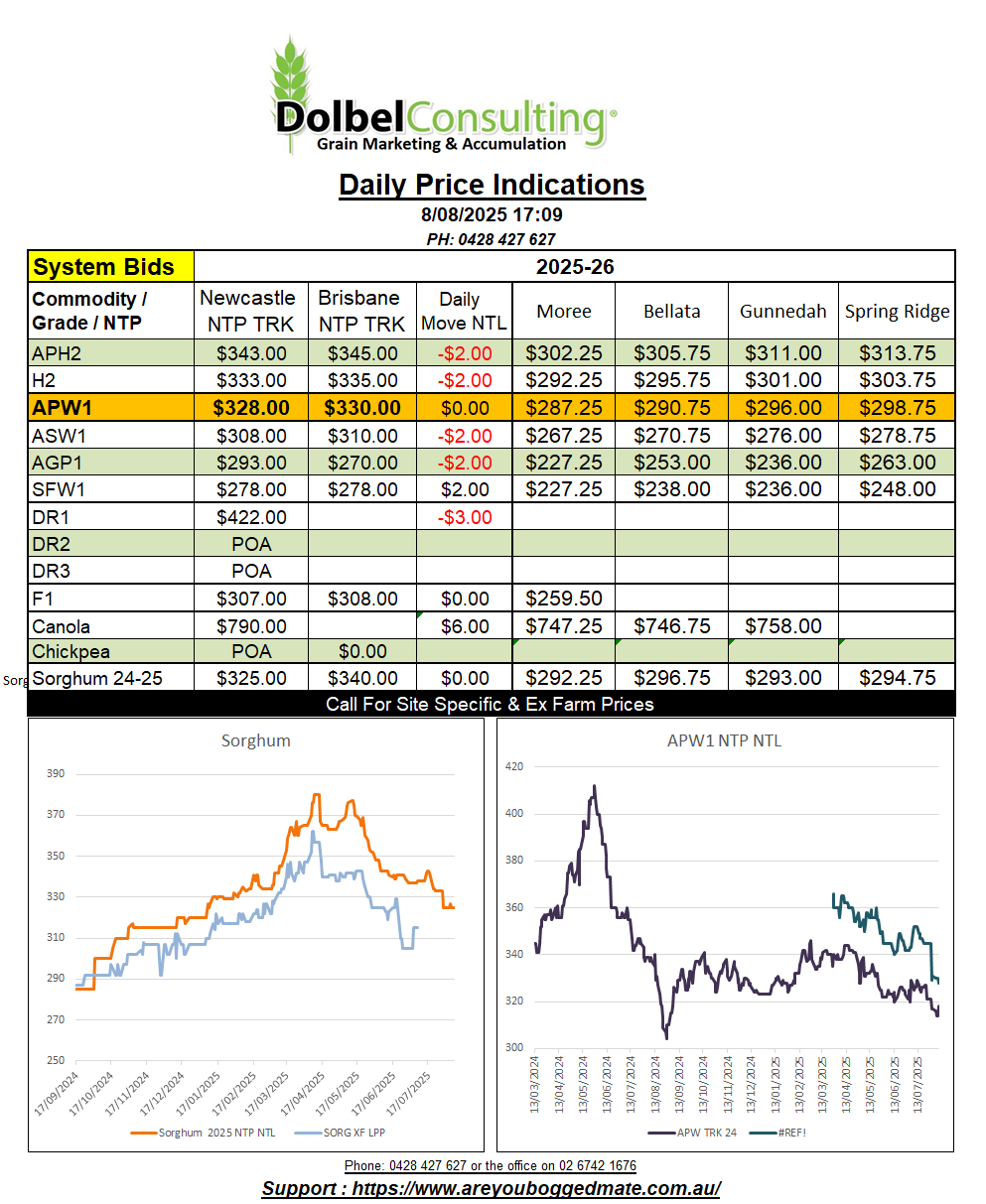

The local market remains dead. Old crop demand is minimal on paper as stocks tighten but the consumer and trade appear to have ample coverage. Old crop sorghum is sideways, bid at $357 Downs packer, $340 LPP packer or $330 +/- NTP Newcastle for track sorghum, net up country around $300 delivered site. New crop wheat is sideways with basis continuing to buffer moves in both US futures and currency at present.

This is producing a flat, boring market with little opportunity for local producers or traders to get set in the new crop wheat market. International markets continue to be influenced by both the Russian conflict and the US trade wars, but do tend to be less volatile than one might expect. Northern hemisphere exporters of wheat appear to be happy to watch the US sell at the bottom. Overnight Russian milling wheat did slip a little lower though. Shedding roughly AUD$1.94/t compared to yesterday, Ukraine not to be out done also slipped lower by AUD$3.71/t compared to yesterday, but is still well above the Russian FOB value for milling wheat. If you convert Russian wheat into the Asian end user market and then back to an Aussie price equivalent port we come up with a number something close to AUD$280-$290 XF LPP. Very close to current new crop bids. This does tend to indicate that we shouldn’t see a lot more downside in local prices unless international values fall away. The general consensus is that with the US able to exceed projected weekly export sales volume at current values, then the next major influence in our local prices will probably be the AUD. This is a little concerning after the US job adjustments earlier this week had the punters talking US interest rates lower rather than higher. A lowering there may push the AUD higher, but it may also hint of continued weakness in the global economy. The Yuan is pegged to the USD and the AUD continues to be traded as a Yuan proxy, hopefully countering any adjustment in US rates.