12/8/25 Prices

Interesting to see a 23c/bu jump in Chicago January 2026 soybean futures last night. It has lent a hand to both canola and rapeseed futures this morning. Corn appeared to have been dragged along for the ride, closing a smidge higher while wheat at Chicago and Minneapolis closed either side of unchanged.

A USDA World Ag Supply and Demand Estimates report is due out tonight. The punters are generally backing higher US corn stocks year on year, lower soybean stocks year on year, and higher wheat stocks year on year. Looking at wheat values at present you could probably come to the conclusion that this is already priced into the market.

Looking at corn one might argue that there is more potential downside, depending on how the USDA manipulate the stocks number tonight. There has been some talk of three dollar corn for a few weeks now. Recent field reports for US corn are starting to show a few issues though, fields that look good from the road appear to have had a pollination problem, much more common with one particular variety. Whether or not this is enough to become a major issue or it turns out to be a storm in tea cup is yet to be determined. The odds the USDA will even take note of this is also low given that much of tonight’s data is based of 30 day old information anyway.

The key to sustaining or improving US wheat futures values will probably lie with their spring wheat estimates. There’s room for reductions in yield across the western parts of the US spring wheat belt. From an international perspective we may also see some reductions in the Canadian number. Late rain across the Canadian Prairies appeared to have stopped the collapse of yields in many locations but the chance of an average crop across much of southern Saskatchewan is unlikely at best. The elephant in the room could be the Russian spring wheat crop. Its had a dream run and may counter any reductions in Canadian or US yields. Rainfall across Argentina has also been very good this winter, we may see some slight increases for wheat there too.

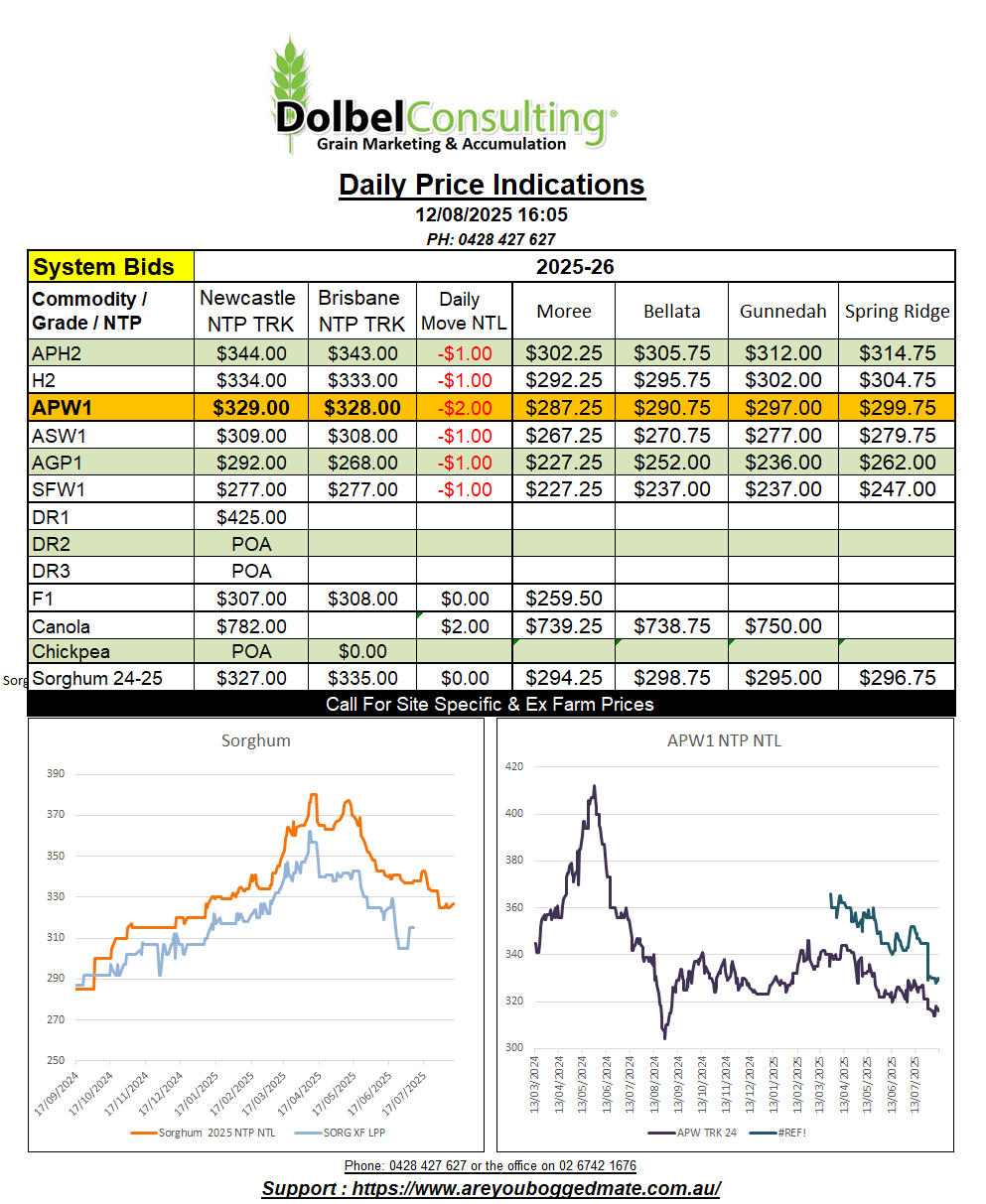

More of the same this week, the packers appear to be in control of the old crop sorghum market for the time being. The system market appears steady at $300 delivered LPP depot. Comparable to $325 Free On Truck (FOT) depot. Remember this number if you are cleaning up any ex farm grain.

The Carrington port was bid at $358 late last week for 1k. Cargill have 15kt loading at Carrington on September 1st, in and out in one day. Accumulation for this slot appears to be covered. There was a little “selling the track, buying delivered” occurring as the usual up country executions issues compounded but this appears to have sorted itself out as grower stocks become depleted.

The national sorghum program this year appears to be indicating a carry over of roughly 139kt, not a lot and mainly across far northern NSW and QLD with a deficit on the LPP. I’ll put together a final S&D in September out lining box and bulk exports.

The new crop market remains incredibly flat for both wheat and barley while canola is up and down like a brides nightie.

New crop canola on the track fell $10 on Monday, after gaining $6.00 on Friday. Overnight both French and Canadian markets were higher. Paris up €3.75/t in the Feb slot and Winnipeg up CAD$11.20 / tonne in the Jan 26 slot. These moves appear to be against the flow in palm oil but followed the Chicago soybean market more closely. The combination of a slightly weaker AUD here this morning and the better oilseed futures should help canola take back some of yesterdays losses.