19/8/25 Prices

The USDA US weekly crop progress report was out after the close last night. 3% of the US corn crop is rated as mature now, with 72% of the corn crop in the dough stage. The crop condition rating for corn slipped from 52/20 – 72% G/E last week to 50/21 – 71% this week, still a very handy crop.

82% of the US soybean crop is setting pods, the condition rating for beans remained unchanged at 53/15 – 68% G/E, but there was a 1pt move from Fair to Poor.

US sorghum was pegged at 78% in head of which 34% is now colouring and 18% is mature. The G/E condition rating for US sorghum slipped from 47/19 – 68% last week to 46/17- 63% this week. Prices for US sorghum were mixed overnight, FOB Texas values generally weaker.

US spring wheat harvest has moved to 36% complete. N.Dakota remains slow at just 24% harvested. The spring wheat G/E rating improved 1pt to 50%. The overall harvest progress is a little better than what the trade had predicted prior to the release. Possibly triggering more technical selling tonight.

US wheat futures continue to push lower, surprising many as the US sales pace is already higher than it was for the same time for the marketing year this time last year. US wheat out of the Pacific Northwest continues to move into the Asian consumer, enjoying the lack of competition from the major southern hemisphere producers and better freight rates than Black Sea suppliers. The US has also bullied some Asian consumers into supply agreements with tariffs.

HRWW values out of the PNW were a little firmer in AUD/t terms compared to yesterdays conversion, up roughly AUD$2.50/t, as was club white wheat. Cash spring wheat values, both Canadian and US, out of the PNW were lower by less than a dollar a tonne.

Canadian canola values were lower, cash bids ex farm reflecting the lower futures market. Paris rapeseed was firmer across all months.

The WA crop just keeps getting bigger and bigger. The rain expected there over the next couple of days will only help the crop at the most crucial stage of development in September.

The latest Grains Industry of Western Australia data shows an increase from their last production estimates. The latest projection has wheat production there at 11.5mt, barley at 5.97mt, and canola at 3.105mt, total winter crop production, including oats and pulses, is now estimated at 21.928mt.

The WA winter crop is unlikely to beat the 26.1mt record set in the west in 2022-23, but may well land a place in the top three production years.

Meanwhile east coast production is only being held back by fewer than expected acres that were sown, in many cases due to fields being too wet.

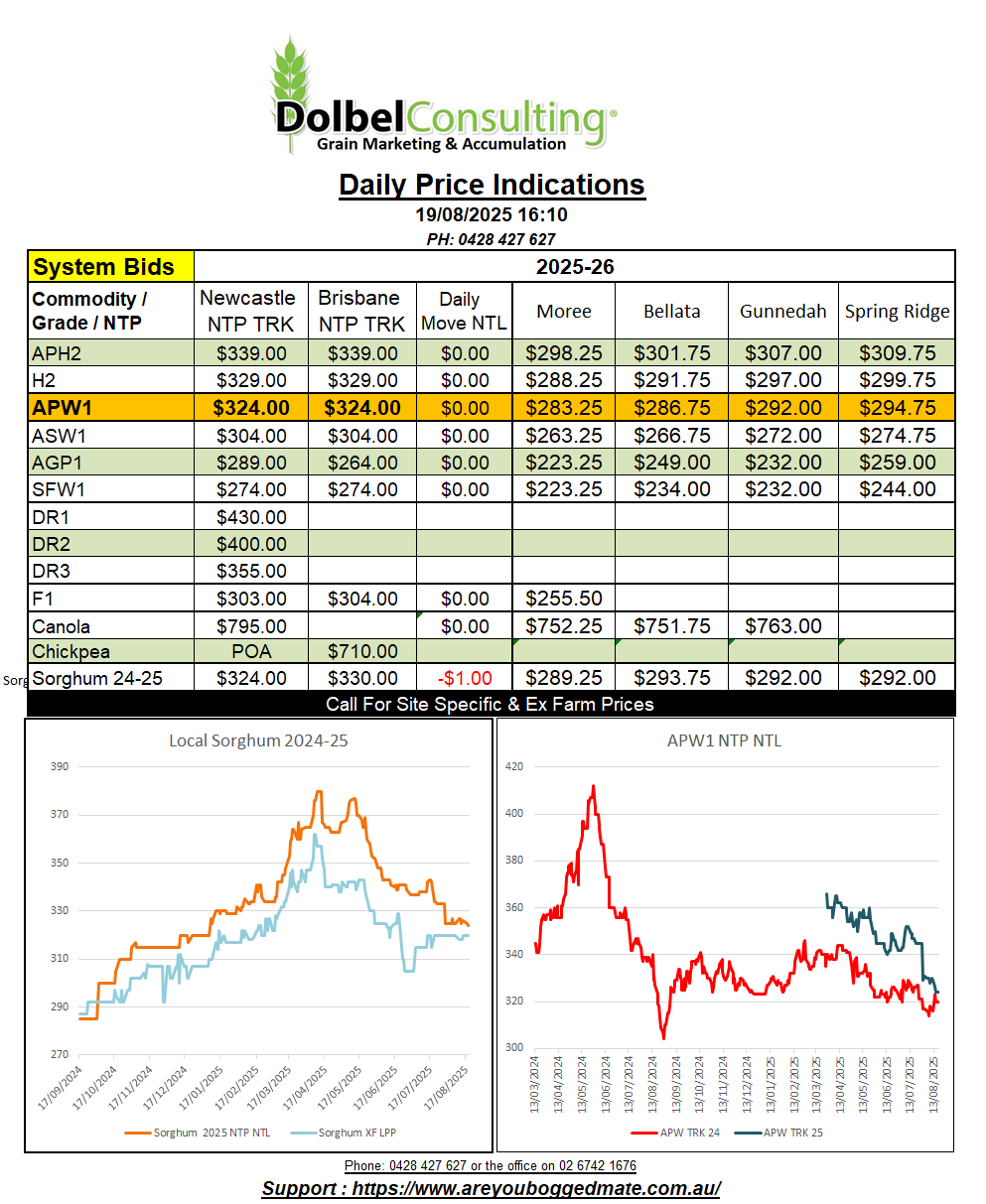

Marketing opportunities for the new crop have been very limited this year. The new crop APW1 NTP Newcastle bid trading a range of just $42.00 since its introduction at $366 NTP Newcastle back in late March. Yesterday saw the new crop APW1 multi grade contract bid at just $324 NTP Newcastle, the lowest bid for APW1 we’ve seen leading up to a harvest since August / September last year, when values slipped as low as $310 NTP NTL. When this happened last year Chicago wheat futures were roughly 30c/bu higher than they are at present and the AUD was 67c +/-.

Interestingly HRWW cash values out of the US Pacific Northwest were just a couple of dollars higher than they are now when converted to a AUD/T XF LPP equivalent price using Asia as a consumer last year. The softer AUD is helping a lot.