20/8/25 Prices

International futures markets for grains were generally lower. MGEX spring wheat was one of the few grains that bucked the trend, closing higher by a very small margin.

Hard red winter wheat was the weakest of the wheat contracts. This rolled across to slightly lower values out of the Pacific Northwest. Using the north Asian consumer market as a benchmark consumer we can compare the CiF value for US HRWW and Australian H2 wheat. At current values the US product is roughly AUD$7.38/t cheaper than the Aussie product. That’s not a lot given that it’s not unusual for white wheat to pull a $25 premium to red wheat given its milling characteristics.

Spring wheat (13%+) values out of the US / Canadian Pacific Northwest were higher. Combining the improvement in both cash and futures for spring wheat in the US and Canada with the drop in the AUD we see a net change in the conversion value from FOB US to XF LPP of just under +AUD$3.00/t.

Paris milling wheat (12%) futures were off €1.75/tonne in the December slot. Cash values FOB France using a similar conversion from a CiF end user point to an XF LPP price shows that French cash values actually improved a little, just under a dollar a tonne. Black Sea values using a similar conversion were up over AUD$4.00 / tonne. Using a generic Asian home to compare the competitiveness of USA HRWW to Russian milling wheat of a similar protein we see that the US product is as much as US$25.00 cheaper than Russian wheat and more than $35.00 cheaper than Ukraine milling wheat.

The weekly ND Wheat crop progress report shows 77% of the North Dakota durum crop rated good to excellent, with just 2% rated poor. Further west in Montana the durum crop is rated just 1% good and 57% Poor / Very Poor. Around 40% of the Montana durum crop is now in the bin. N.Dakota has harvested around 24% of their durum, just 1pt under the 5 year average. Saskatchewan durum harvest is underway but we’ll see more data late next week.

Local values remained under pressure yesterday. The trade continue to actively seek old crop grains and pulses but the bids are less than enticing. With most old crop product now placed the hunt for old crop grain is much harder, even if the trade could handle better bids.

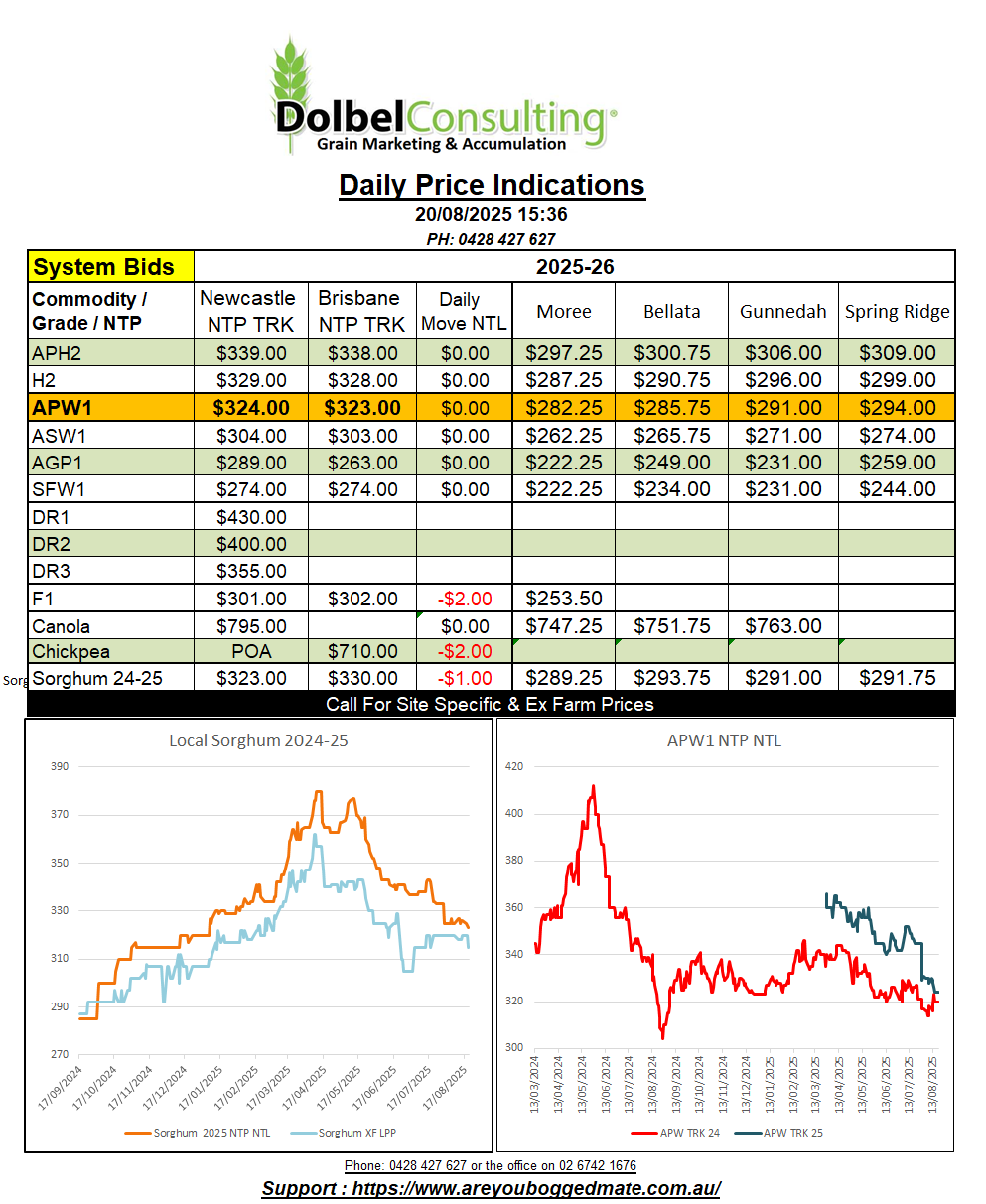

Sorghum by road to Carrington was bid at $365 delivered prompt. After this slot is covered, 15kt in September for Cargill, the odds of seeing more through Carrington will be remote. Graincorp covered their 60kt for August a while ago and have been happy to bid under the box trade in the mid term. The local box market continues to be the best bid out of the track. Agracom bidding just a dollar above a poor Graincorp bid in the system. Give me a call if you are cleaning up some system sorghum, I’ve been able to bid a couple of bucks above the crop connect number for sorghum to be packed elsewhere.

New crop sorghum saw a bid of $325 delivered Downs packer which is roughly $25.00 under the current old crop bid. Using US corn futures as a benchmark for feed grain values, like sorghum, one notices that there is a carry in the corn market. Currently corn is valued at 379.5c/bu nearby at Chicago versus 431.25c/bu in May 2026 slot, roughly +AUD$32.00. This does raise the question, why are we seeing a discount between new and old crop sorghum bids at present. A similar pricing strategy was implemented last year, the new crop bid pushed $30 higher between the introduction of new crop bids in September and the end of October, which wasn’t due to stronger corn values.

New crop wheat was flat yesterday. We saw a slight improvement in basis and the lower AUD also helped. With the AUD down 0.62% this morning is will go a long way to countering any downside pressure from US futures. The move in the AUD equivalent to roughly 3c/bu, basis could pickup the difference.